Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

A 30% rise in the copper price over the past month has put a rocket under the shares of copper miners. There are many reasons behind the unprecedented commodity price movement and most of them suggest you should stay bullish on the metal, even after the big price surge.

I believe all investors should have some exposure to the metal in their portfolio. It is an economic bellwether. If you believe the world economy is going to grow, you need a slice of copper. It is used in wiring, power grids, construction, transport, and much more.

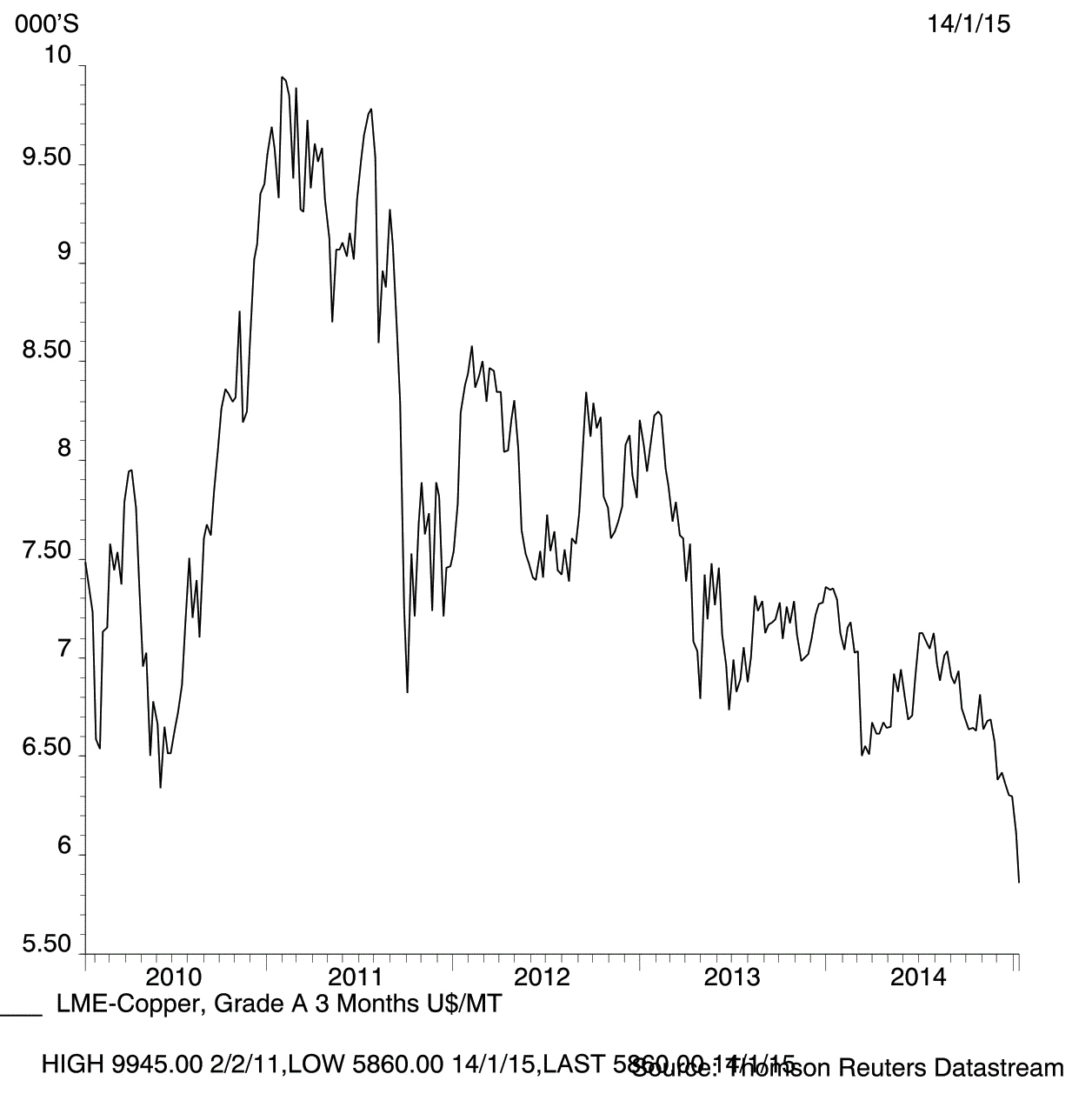

The price of copper for delivery three months in the future traded at $4,635 per tonne on 21 October. It had jumped to $6,025 per tonne by 11 November. The metal had eased back to $5,422 per tonne as of 15 November, but still very attractive.

We flagged a brighter outlook for copper in our article on miner Savannah Resources (SAV:AIM) on 3 November. The shares have since risen by 27% in value. Key to that stock pick was UBS’ forecast that the copper market would switch from surplus to deficit in 2017 which implies a rising copper price.

Market dynamics

The copper industry has a tendency to experience supply disruptions as it is prone to labour strikes and production disappointments, often due to ageing mines where grades are falling.

Donald Trump’s victory in the US presidential election is also supportive for the copper price. He wants to spend heavily on infrastructure which will require a lot of copper.

Macquarie earlier this week increased its copper price forecasts by 11% to 17% over the next four years to reflect the current market situation and the Trump effect.

It doesn’t believe the US infrastructure push would manifest until 2018, given the lag between policy formulation and implementation. However, it acknowledges that copper could benefit in the interim as the market starts to allocate a bigger portion of assets to the metal in anticipation of an eventual infrastructure push.

I expect to see a strong flow of money into exchange-traded funds that track the copper price. Good copper miners to buy, in my opinion, are Kaz Minerals (KAZ) and the aforementioned Savannah.

Rio Tinto (RIO) also looks interesting amid extra exposure to iron ore and coal – two more commodities racing ahead in price this year.

![]()

This article is provided by Shares Magazine. Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters and does not guarantee the accuracy or completeness of the information in this article.

Investors acting on the information in this article do so at their own risk and AJ Bell Media Limited and its staff do not accept liability for losses suffered by investors as a result of their investment decisions. Shares is published by AJ Bell Media Limited part of AJ Bell.