Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

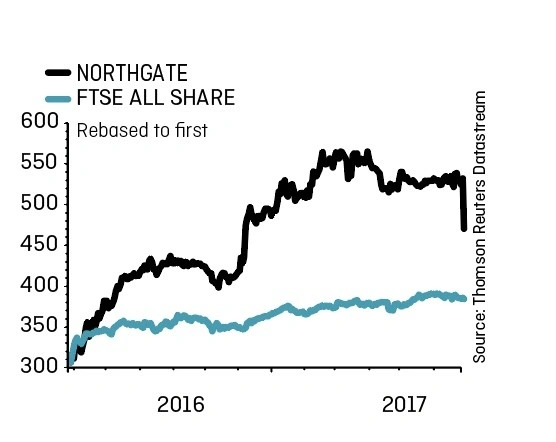

Northgate (NTG) 446p

Gain to date: 8.5%

Original entry point: Buy at 411p, 24 November 2016

Don’t panic following news of weakness in Northgate’s (NTG) UK operations (27 June). We are encouraged by the new CEO taking immediate action to identify problems in the business and come up with a plan to fix them.

Full year results for the year to 30 April 2017 were below expectations with £75m pre-tax profit versus c£80m forecast by analysts.

Fortunately, the van hire group says its Spanish business continues to trade well and it expects to grow the number of vehicles on hire over the course of the new financial year.

The share price fell 16% on the results, not helped by analysts downgrading earnings per share forecasts by 10% to 11% for the next two years.

We’re naturally disappointed by the outcome, but believe it is worth persevering with the shares.

We originally selected Northgate in the belief that activist investor Crystal Amber would put pressure on the business to either break itself up, potentially selling the Spanish arm, or do something else that could generate value for shareholders. That investment rationale still has merit today. (DC)

![]()

This article is provided by Shares Magazine. Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters and does not guarantee the accuracy or completeness of the information in this article.

Investors acting on the information in this article do so at their own risk and AJ Bell Media Limited and its staff do not accept liability for losses suffered by investors as a result of their investment decisions. Shares is published by AJ Bell Media Limited part of AJ Bell.