Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Whether you’re an experienced investor or just starting out it’s likely you’ll make some mistakes along the way. These are the 10 common errors you should try to avoid in order to boost your chances of success.

Not having an investment goal

Before you start investing it’s important to think about what you want to achieve and over what timeframe. For example, your goal might be paying off your mortgage in 15 years or going on a world cruise when you reach age 60.

Andy Bell, chief executive of AJ Bell and author of The DIY Investor, says starting to invest without a set of objectives is like going for a drive without a destination in mind.

When you have an objective it’s easier to figure out how much risk you can take and which assets might be suitable.

Not diversifying

You might favour a particular sector or stock, but if you invest all your money in it and the stock or sector plummets it will have a hugely adverse impact on your portfolio.

You can spread your risk by investing in a range of asset classes which don’t all rise and fall together, such as equities, fixed interest, property and cash.

You can also diversify across geographies, sectors and company sizes.

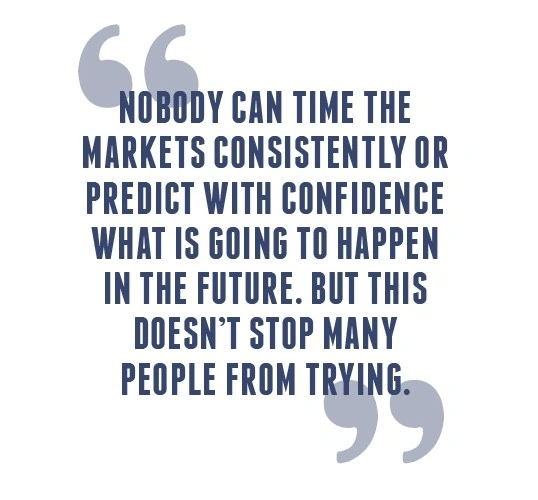

Trying to time the market

Nobody can time the markets consistently or predict with confidence what is going to happen in the future. But this doesn’t stop many people from trying.

‘Unfortunately many individuals get swayed by short-term noise, performance or market sentiment, moving money out of areas they think are destined to fail and jumping into those they believe are primed for success,’ says Patrick Connolly, head of communications at Chase de Vere, a financial planning firm.

Connolly says the best approach is to have a long-term investment strategy and stick with it through good times and bad.

It’s worth realising that when the market dips you only lose money if you sell your investments.

Refusing to accept mistakes

This doesn’t mean sticking with terrible investments. Robert Ward, chartered wealth manager at Walker Crips, says one of the most damaging trends is the reluctance to accept a mistake.

Investors are often loathe to sell a poor performing investment in the hope it will bounce back at some point.

‘The reality of investing is that you will not get every single investment decision right – it’s simply not possible. Being able to accept a mistake and sell an investment when it is losing money is difficult but can save a lot of pain over the long term,’ says Ward.

Putting too much emphasis on cash

Cash isn’t the safe haven it appears to be. Inflation can reduce the value of cash over time and reduce the value of your savings.

‘The level of cash held should be viewed as part of a diverse portfolio which is in line with investment objectives,’ advises Gareth Evans, investment manager at Hargreave Hale.

Failing to review

It’s not sufficient to set up a portfolio and then leave it because investments might not perform as expected.

‘Regular and detailed reviews are essential to ensure a portfolio is in line with current goals and objectives,’ says Evans.

If some of your investments have performed well and others have performed badly, this can change the overall shape of your portfolio meaning you could end up taking too much, or too little, risk.

You can rebalance your portfolio by selling some of your investments which have performed well and reinvesting into those which have performed poorly. This will help to get you back to your starting position.

Chasing last year’s winners

Investors often jump into funds or asset classes which have a strong short-term performance, believing the outperformance will continue.

You end up investing at the top of the market after gains have already been made, and then selling out near the bottom just as the performance is about to turn.

‘This approach can lead to people making sizeable losses and having a thoroughly miserable experience along the way,’ says Connolly.

Believing the hype

A lot of the investment industry is based around trying to sell products or promote ‘star’ fund managers. As a result, different funds or asset classes are constantly hyped up.

An obvious example is the technology boom and bust in the late 1990s.

Connolly says many people select funds that are promoted by discount brokers or the media.

The result is they end up with a portfolio of individual ‘flavour of the month’ funds with no real overall strategy and little idea of the overall asset allocation and risk profile of their portfolio.

Connolly says investors should look at the bigger picture and buy funds that enhance their overall portfolio, rather than buying a random fund which is predicted to perform well over the next six months.

Missing out on tax breaks

You and your spouse or partner can each pay £20,000 into an ISA and £40,000 into pension each year to shelter your money from income tax and capital gains tax.

Andy Bell says investors should make the most of their £11,300 capital gains tax allowance by cashing in sufficient gains each tax year. You can move investments between spouses to make the most of your allowances and income tax bands.

Ignoring charges

Costs eat into your investment returns, so it’s important to compare the fees levied by platforms and funds. They can often vary hugely.

The ongoing charges figure is the best number to look at when comparing funds, as it’s made up of the annual management charge plus administrative expenses.

It’s important to compare like-with-like when deciding whether a fund is over-priced or not.

![]()

This article is provided by Shares Magazine. Shares publishes information and ideas which are of interest to investors. It does not provide advice in relation to investments or any other financial matters and does not guarantee the accuracy or completeness of the information in this article.

Investors acting on the information in this article do so at their own risk and AJ Bell Media Limited and its staff do not accept liability for losses suffered by investors as a result of their investment decisions. Shares is published by AJ Bell Media Limited part of AJ Bell.