Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineAiming for a hat-trick with Hogg

After delivering gains of 40% and 20% over the past couple of years it has featured among our portfolio of top picks, we’re again backing dependable corporate travel specialist Hogg Robinson (HRG).

Hogg operates in a competitive market with some big hitters – slugging it out with American Express’ (AMEX:NYSE) Travel Services division in a market worth $1.5trn (£1.8trn) and growing 6% a year.

While it not might be as well known as industry heavyweight American Express, Hogg is no minnow at roughly one-third of the Amex Travel division’s size as measured by fee and commission income.

And Hogg has a solid brand of its own having started business in 1845.

On top of these attributes, the Basingstoke-headquartered business has the potential to deliver shareholder value through its fast-growing Fraedom technology unit and also has an earnings cushion from a weaker currency following the UK’s vote to leave the EU.

Digital growth

Revenue declines in recent years mask significant developments in Hogg Robinson’s business model.

Online booking and expense management represents 50% of Hogg’s business today, up from 27% in 2012. While group revenue has stalled, profit continues to grow because Hogg’s digital Fraedom travel and expense management tool enjoys higher margins than its traditional consultant-led business.

Whitman Howard analyst Andrew Smith says Fraedom’s growth gives Hogg chief executive David Radcliffe a couple of options.

Heavier marketing spend could be used to help the unit capture more market share as it grows.

‘Alternatively, Hogg could crystallise value and go for an initial public offering or trade sale especially given the multiples achieved by similar companies for on-line travel businesses.’

Currency boost

Generating around 60% of its sales abroad, Hogg is a beneficiary of sterling weakness according to Whitman analyst Smith.

Smith’s says Hogg’s foreign exchange exposures indicates a 7% boost to operating profit on top of a previously forecast 5% improvement, though these have not been added to the analyst’s forecasts.

Hogg Robinson chief executive David Radcliffe said in a 22 July trading update that revenue was 3% lower after stripping out foreign exchange movements and noted ‘an initial softening’ of demand following the EU vote.

Risks include a large pension deficit and some economic cyclicality in the corporate travel services market.

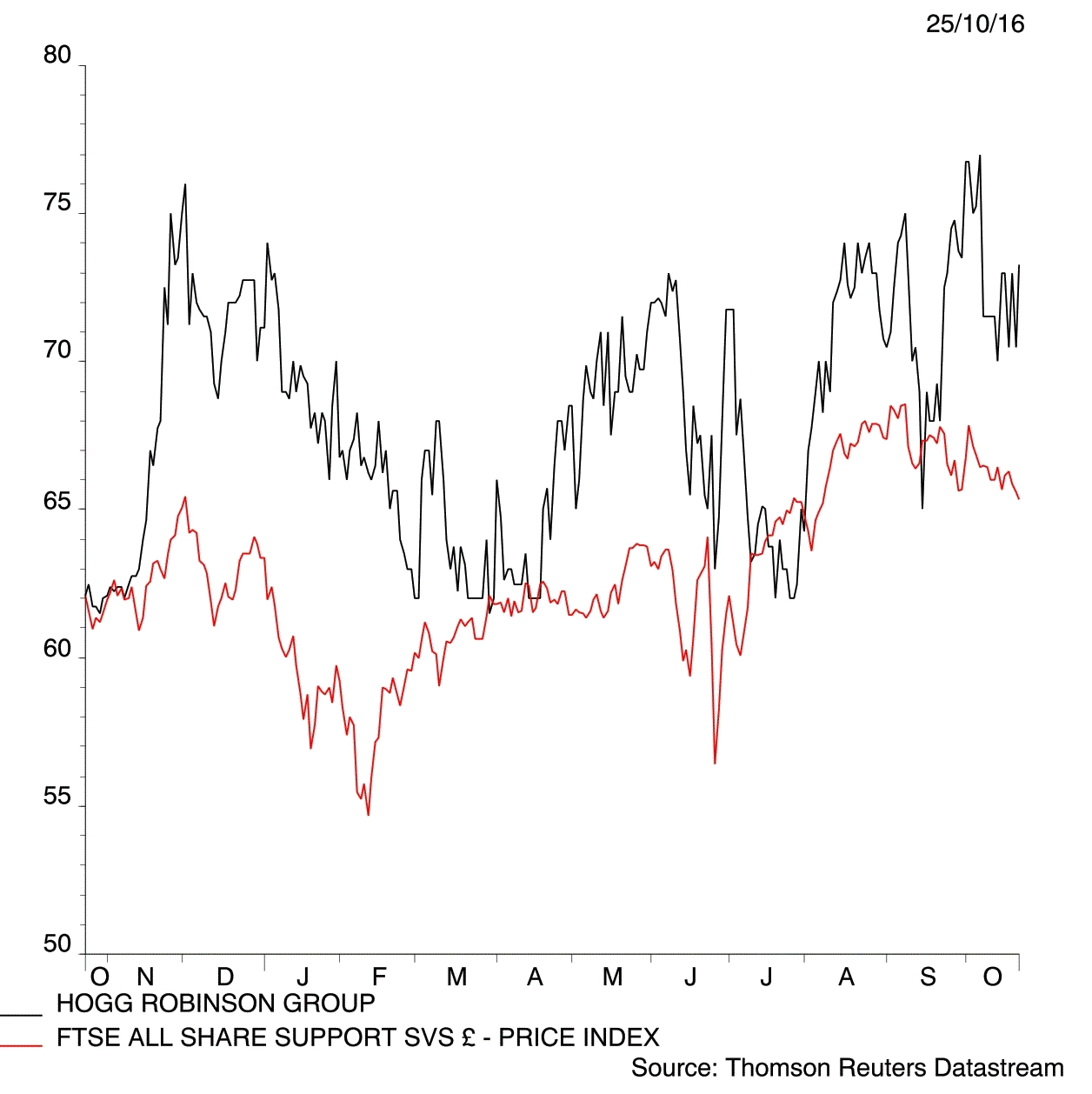

Hogg Robinson (HRG) 69p

Stop loss: None

Market value: £235m

Prospective PE Mar 2017: 9.6

Prospective PE Mar 2018: 9.2

Dividend yield: 3.7%

Analyst price target: 95p (Whitman Howard)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.