Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSage under pressure

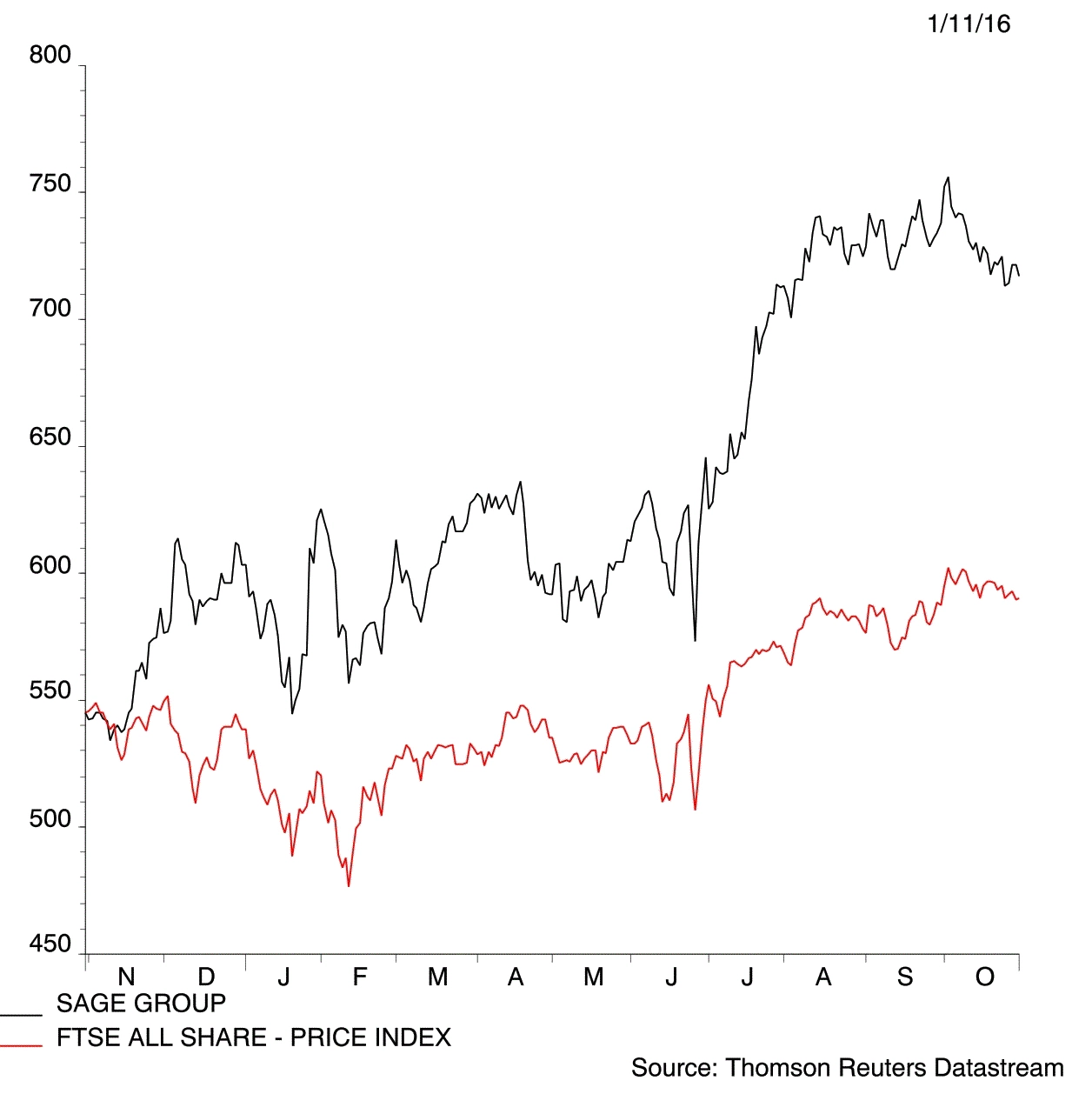

Accountancy software supplier Sage (SGE) may struggle to cling on to its current lofty share price rating. There are likely to be limited signs of accelerating growth when it reports full year 30 September results on 30 November, and there is even the risk of missing vital 6% organic revenue growth expectations.

According to calculations by analysts at Canaccord Genuity, organic revenue expansion could come in at nearer 5.3% after currency oscillations. Such a narrow miss may appear small but the market is unlikely to see it that way given that it ‘seems to have convinced itself that Sage’s growth is poised to accelerate.’

Sage has enjoyed a two-year share price run since CEO Stephen Kelly was installed, doubling to the current 716.5p. That puts the price to earnings multiple at 22.7-times, based on consensus earnings per share estimates of about 31.6p for the year ahead to 30 September 2017.

While Kelly has received almost universal praise the way he has refocused the FTSE 100 company’s sales strategy and driven cloud-based products, limited real financial gains have been made, with anticipated full year operating margin estimates of 27% unchanged since late 2014.

Analysts remains split on Sage but we side with the more cautious view, despite the group’s solid cash generating attractions.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.