Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineThree in a row for Experian?

Credit bureau Experian (EXPN) has featured as a Shares top pick for two years consecutively and we’re returning the stock to our Great Ideas list of stocks for another 12 months.

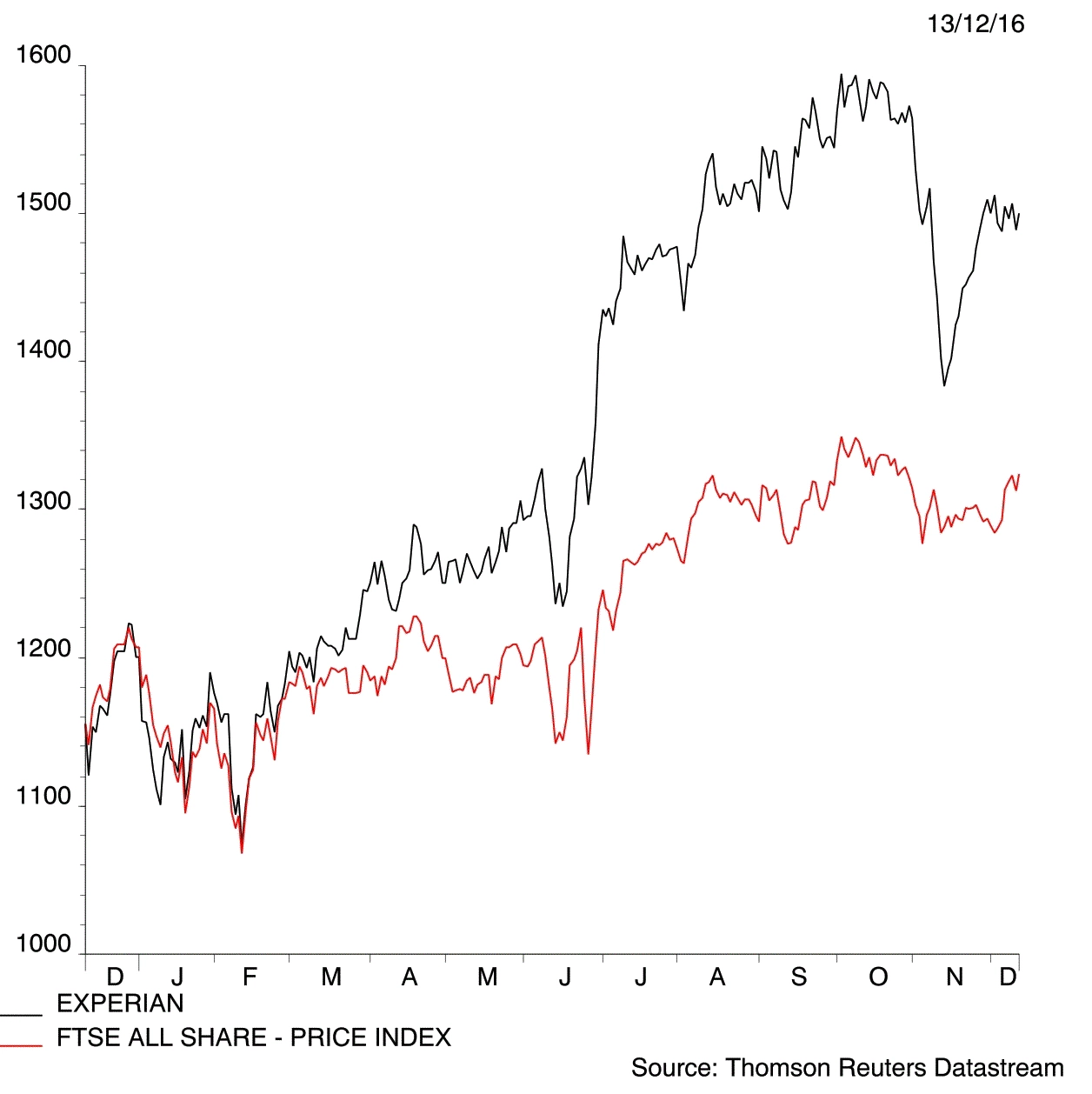

Experian is in our view one of the UK’s finest businesses. Its progress over the past two years, delivering returns of 70% including dividends, provides a good example of how investors can make money by owning good quality stocks.

Stronger than average earnings growth is a key reason for Experian’s stock market performance during this period.

Earnings and multiples

Earnings per share were forecast in 2014 at 56.6p for the year to 31 December 2015. This year, analysts estimate Experian will earn 91 US cents per share, or 71.7p, an increase of 26.7% from 2015.

Another key reason for Experian’s stock price performance is an expansion in its earnings multiple.

Dividing Experian’s estimated earnings for the 2016 financial year by its current share price of £15.00 gives a 2016 price-to-earnings ratio (PE ratio) of 20.9. Back in 2014, doing the same calculation, Experian had a PE ratio 16.2.

Over the last two years, Experian’s PE ratio has expanded by around 29.0%.

Another way of describing this is to say that Experian’s earnings have increased by 1.267 times (26.7%) over the last two years and its valuation multiple has expanded 1.29 times (29.0%).

Multiply these two numbers together and you have the exact return shareholders have enjoyed from owning shares in Experian over the last two years, excluding dividends: 1.64 (64%).

Dividends added a further 6% over the two years for a total return of 70%.

Can Experian do it again?

Earnings growth of nearly 30% in two years is a good result and would be difficult to repeat indefinitely into the future. Also, now that Experian trades at a higher PE ratio of 20.9, future expansion of this multiple may be less likely. But we still remain bullish on the stock.

Analyst Robin Speakman at Shore Capital says shares in Experian look expensive.

‘On a cash flow valuation basis, using a discounted cash flow model, Experian is trading above our fair value level of £14.50, suggesting a market perception of a discount rate some way below ours,’ wrote Speakman in a 2 November research note.

‘Clearly, the share price reflects the recent strength of the US dollar to sterling; we continue to appreciate the strength of the strategic market position that Experian enjoys.

‘Given what we considered to be a full valuation we retain a hold stance for the present.’

Key risks for shareholders include potential cyber attacks on customer data, increasing regulation and Experian’s £3bn debt load. (WC)

Experian (EXPN) £15.00

Stop loss: None

Market value: £15.1bn

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.