Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineInmarsat dividend to return to earth

Shareholders in Inmarsat (ISAT) could face a payout freeze as the company grapples with investing for long-term growth versus bumpy free cash flow.

The satellites network operator has increased its dividend payment by more than 4% in each of the past five years, with double-digit increases in two of those financial periods.

Since 2013 free cash flow (FCF) has bobbed between $81m and $298.9m. It is anticipated to deliver $96.3m for 2016. Consensus forecasts for 2017 through to 2019 show free cash flow of $24.4m, $109.6m and $111.2m respectively. Dividends will cost the company between $245m and $264m per year over the same three years.

‘We believe that the market is pricing in continued growth in the dividend near-term,’ note UBS analysts Michael Hill and Polo Tang. ‘In our base-case scenario we expect Inmarsat – possibly at full year 2016 results – to stop growing the dividend until it is covered by equity free cash flow (EFCF).’

EFCF is calculated by adding net income, depreciation and amortisation and net borrowings together, then stripping out capital expenditure and working capital.

‘We believe this change in the dividend policy will allow Inmarsat to invest in its substantial long-term opportunities and avoid pressuring the balance sheet while EFCF generation is limited and uncertain,’ comment Hill and Tang.

Growing pains

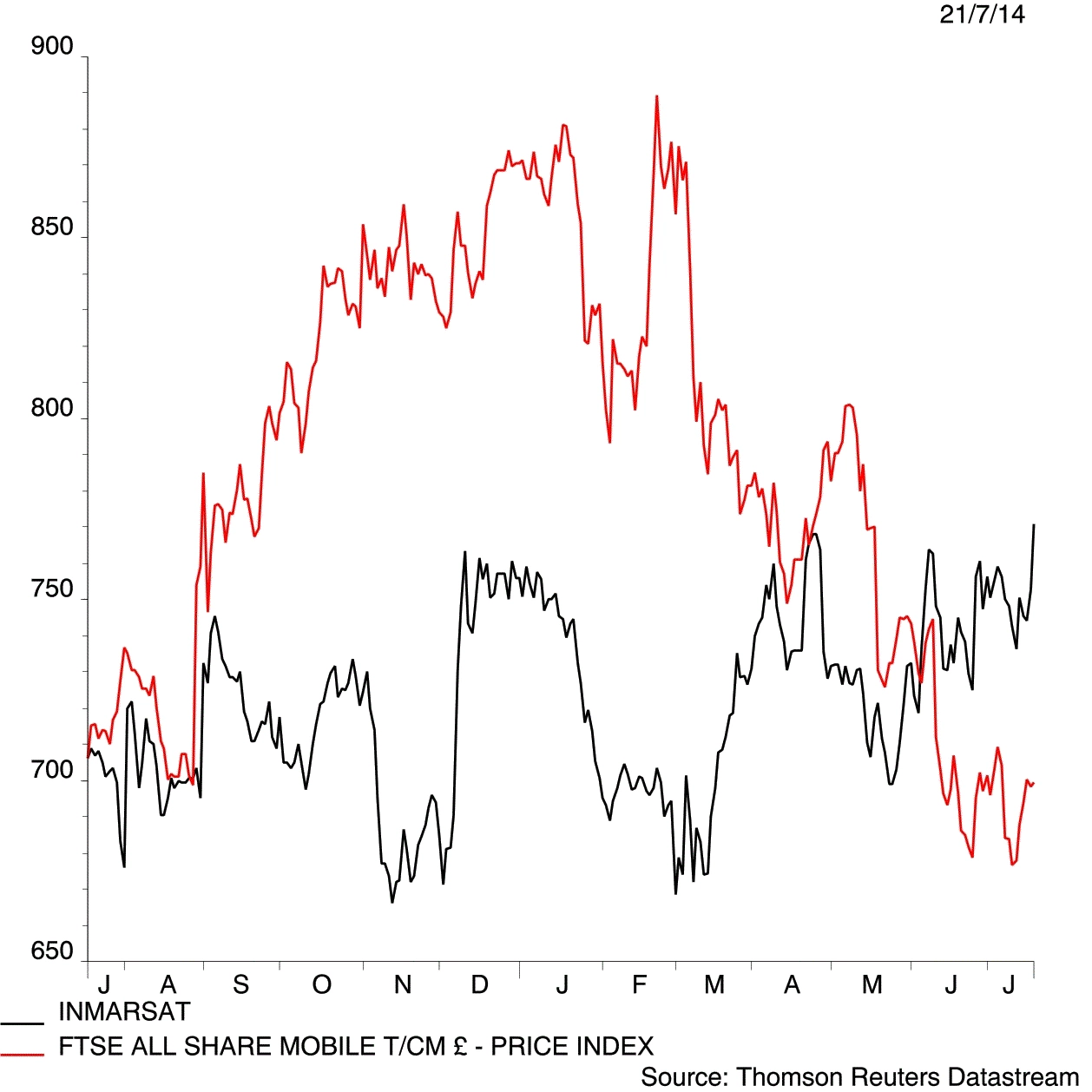

Inmarsat has endured a tough past year with a patchy operating performance sparking increasing concerns over financing costs of its near $1.8bn net debt. The share price has almost halved since the start of 2016 to 638p.

Headline trading showed some improvement during the third quarter to 30 September 2016. Revenue and EBITDA (earnings before interest, tax, depreciation and amortisation) increased 5.8% and 14% to $342m and $205m respectively, although almost all of the growth was down to its Ligado networks joint venture in the US (previously called LightSquared).

There has been some improvement. Contracts with government agencies have increased modestly while Inmarsat’s aviation side has seen a swathe of agreements over the past three or four months. It has been signing airlines to its Global Xpress fleet to supply inflight broadband internet access.

But the enterprise division continues to go backwards as does its maritime arm, worth 45% of group revenues. The latter ‘continues to be hindered by a sustained recession in the global shipping industry,’ according to analysts.

Even if the payout is frozen the forward income yield would still stand out at 6.6%. On balance that looks attractive even if sentiment may make for a bumpy share price through 2017. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- UK Banking Shares Performance

- General Retailers Shares Performance

- Story In Numbers - Fishing Republic

- 37%

- Five profit warnings in 15 months

- 1st time in 12 months: Investors give bullish signal with fund inflows

- From $17m to zero: Kenmare Resources’ earnings up in smoke

- $205.2bn: The value of failed takeover deals so far in 2017