Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLloyds leads the way on banking recovery

The days of banks having tarnished reputations is far from over but there are encouraging signs that some of the old retail investor favourites are getting back on form.

Lloyds Banking (LLOY) leads the pack as its first quarter earnings beat market expectations. Analysts suggested they might upgrade full year profit forecasts by as much as 7% following the statement.

Could Lloyds deliver consistent dividend growth once again?

The bank posted a £2.08bn underlying profit, and this is leading to increased confidence it can return to consistent dividend growth.

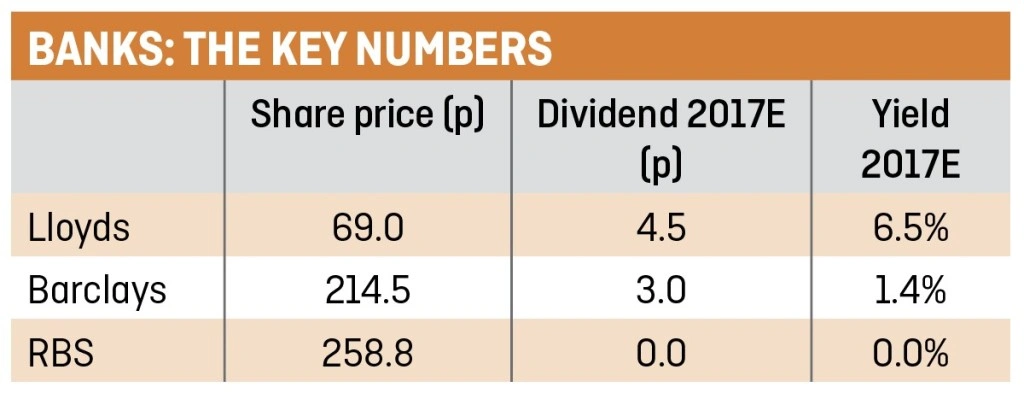

Investec forecasts a 4.5p per share dividend for the 2017 financial year, equating to a healthy 6.5% prospective yield.

Investment bank Jefferies says that Lloyds’ net interest income has surpassed expectations for the first time ‘in ages’.

The bank’s net interest margin (NIM), the difference between income from lending and the cost of funding and a key indicator of a bank’s profitability, is up to 2.8% from 2.68% in the final quarter of 2016.

RBS returns to profit

Another benefactor of state aid, the Royal Bank of Scotland (RBS) is not faring as well. The bank is still 72% owned by the Government, while Lloyds could be fully privatised soon.

RBS’ recent results show it is finally back in the black, having turned a £938m loss this time last year to a £259m profit in the first quarter of 2017.

The bank’s NIM improved to 2.24% from 2.19% and the bank further reduced its cost to income ratio to 76.1%.

However, the management also warn profit will be down for the next quarter due to a slow start in its investment banking arm.

RBS is in no position to start paying dividends any time soon so while the bank is finally moving in the right direction it has a lot of ground to make up on Lloyds.

At a headline level Barclays (BARC) exceeded analyst expectations in the first three months of 2017 with profit doubling compared to the first quarter of last year. However this excludes a big hit for selling its Africa unit. The bank incurred a £658m post-tax cost on the sale of the business.

Unfortunately for Barclays, investors seem more concerned about its chief Jes Staley’s reputation as he is being investigated for his attempts to identify a whistleblower.

The bank slashed its dividend by more than half to 3p a share earlier this year and it does not look likely to raise it in the near future. (DS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.