Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineKeep buying Johnson Service following upgraded earnings guidance

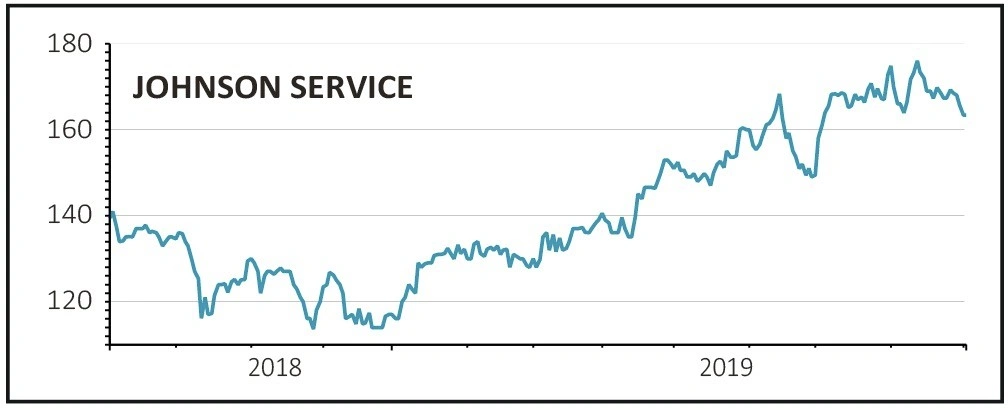

Johnson Service Group (JSG:AIM) 165p

Gain to date: 27.9%

Original entry point: Buy at 129p, 7 March 2019

Our ‘boring is beautiful’ call on catering and workwear hire and laundry firm Johnson Service continues to deliver as the half-year results show.

Revenue was up almost 10% with like-for-like growth of 7.5% thanks to strong demand and higher prices. Since the end of June demand has continued at such a pace that the firm has increased its full year sales and profit guidance.

The group prides itself on the quality of its service and delivery, and this is reflected in high customer satisfaction ratings and retention rates. Happy customers mean repeat sales, but there have been some significant new contract wins as well.

In order to manage this growing demand, especially from the hotel, restaurant and catering sectors, a new plant is opening in Leeds next spring. As well as servicing customers in the north of England the plant will take in work from existing plants, freeing up capacity to service new customers.

Given how strong organic growth was in the second half of last year we’re impressed that the firm has increased guidance for this year and would continue to buy the shares.

SHARES SAYS: This is a great long-term growth story which still isn’t widely known by retail investors.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.