Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy investors are worried about getting their money back from ETFs

Exchange-traded funds (ETFs) can be a great way for people to get started with investing.

This is mostly because of their simplicity, low cost and the ease at which they can be bought or sold, which is known as liquidity.

But that last point has some investors worried, as rising market volatility has once again got people concerned about how the multi-trillion pound ETF industry would react in a financial crisis.

While ETFs have been around since 1993 in the US, and around 2000 in the UK, they only started gaining real popularity after the global recession in 2008.

The concern is whether or not, in times of market stress, they can be sold off seamlessly and at a reasonable enough price to be able to give investors their money back quickly.

Especially in the wake of the demise of Neil Woodford, who struggled to give investors their money back, as well as other liquidity issues affecting fund management firms like GAM and H2O Asset Management, many market watchers are increasingly voicing concerns about ETFs, which have more people’s money than ever but are untested in a real market crisis.

PRICE DE-COUPLING

One of the main issues involves ‘price decoupling’, which is triggered when the liquidity of shares in the ETF – which trade every second – and the liquidity of the underlying holdings fail to match up.

The fear is that this could lead to a breakdown between the price of the fund and the price of the underlying holdings, a ‘price decoupling’, which could lead to people getting less money back when they choose to sell ETFs from their portfolios.

In a research note from August, UK regulator the Financial Conduct Authority (FCA) conceded the ‘rapid growth’ in ETF markets ‘creates potential risks to investor protection and financial stability’.

But it ultimately found no threat to financial stability as of yet as the market has coped well so far with liquidity crunches.

The FCA looked at three instances of stressed markets – the US presidential election in November 2016, a volatility spike in February 2018, and a big bond selloff last December.

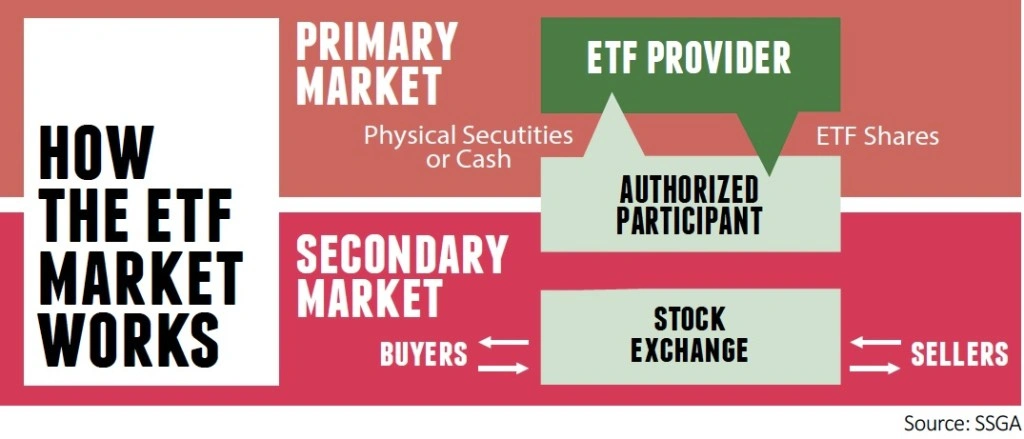

Buying and selling of ETFs in the marketplace is largely done by ‘authorised participants’ (APs), who are typically investment banks or trading firms, with the five largest APs accounting for 75% of ETF trading according to Reuters. These APs can exchange baskets of securities or cash for ETF shares and back again in the so-called ‘primary market’.

The FCA found that during the above periods of market stress, other APs who are normally less active came into the market and started buying and selling, making up for any gaps in liquidity.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.