Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy transport stocks need to get back on the rails

Regular readers of this column will be well aware that it is a bit of a trainspotter – and for that matter a ship, truck and planespotter, too.

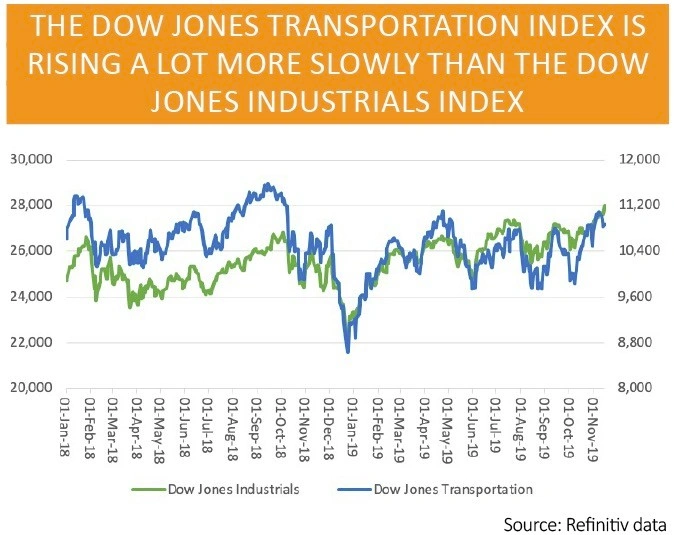

This is because it is a great adherent of Richard Russell’s Dow Theory, which argues that if the Dow Jones Transportation index is thriving then the better-known Dow Jones Industrials index should flourish too.

The logic implies it can only be good news if the share prices of the firms moving goods around the world by road, rail, sea or air are doing well. If something is sold, it has to be transported.

By default, the opposite holds true, or so the theory goes. Weak transport stocks could mean inventories are piling up on shelves and forecourts, to herald production cuts and a potential downturn in industrial activity, economic output, corporate earnings and potentially stock market valuations.

It is therefore interesting to see that the Dow Jones Transportation index still lurks 6% below its September 2018 peak, even as the Dow Jones Industrials index hits the 28,000 barrier for the first time ever.

It would not do to over-dramatise this point, as the Transportation index is still up by 19% in the year to date. But Dow theory says the index needs to lead the Industrials and when it lags attention should be paid. So pay attention we must.

COLLAPSE IN CASS INDEX

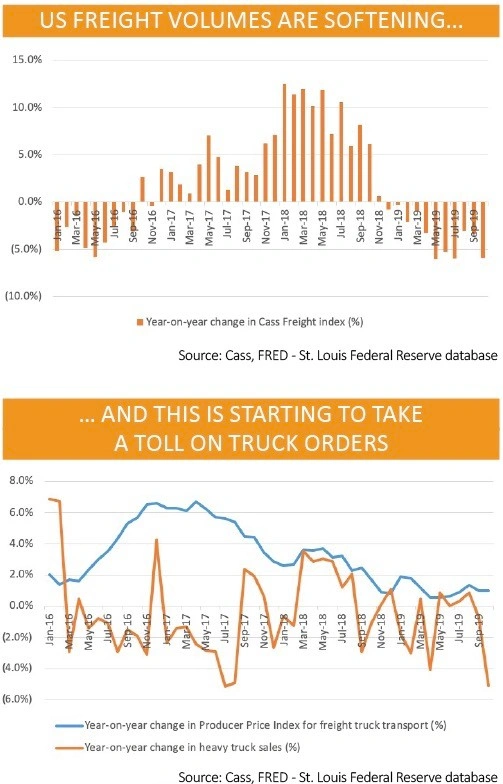

The Dow Jones Transportation index’s inability – thus far – to set new highs does unfortunately tally with quite a few economic datapoints from the US.

One is the Cass Freight index, which measures monthly freight activity in North America. October’s reading showed a 5.9% year-on-year drop in activity. That was the eleventh decline in a row and prompted Cass to make three key observations:

– The shipments index has gone from ‘warning of a potential slowdown’ to ‘signalling an economic contraction’.

– Demand is weaker across almost all modes of transportation, both domestically and internationally.

– Several key modes, and key segments of modes, are suffering material increases in the rates of decline, signalling the contraction is getting worse.

There are lots of cross-currents here, including firms building up inventory and then liquidating them again as deadlines for new US tariffs on Chinese goods come and go, and the 40-day strike by 49,000 workers at General Motors production facilities.

But the persistence of the freight trend is a worry and it is starting to filter through to other parts of the US economy – just look at how the cost of hauling by freight is sagging and how, in turn, that is weighing on orders for new trucks.

If that latter trend is not already showing up in durable goods orders, industrial production (and jobs) data, then surely it will soon, unless there is a rapid improvement. No wonder the Atlanta Fed’s GDP Now and the New York Fed’s Nowcast surveys are busily cutting their forecasts for American economic growth, to just 0.3% and 0.7% respectively, down from the third quarter’s 1.9% annualised rate.

SHIPPING FORECAST

But these freight and transport-related issues are not unique to the US, even if the White House’s ongoing trade dispute, and negotiations, with Beijing could be one major influence.

Global trade volumes are fragile, too, according to monthly World Trade Monitor published by the CPB Netherlands Bureau for Economic Policy Analysis.

Stock markets may not seem unduly fussed, buoyed as they are right now by interest rate cuts from central banks and hopes for a US-China trade deal. But corporations are taking note. Just ask Copenhagen-quoted AP Møller Maersk, the world’s largest container shipping company (a status which may make it a decent proxy for global growth).

Chief executive officer Soren Skou has just cut his outlook for growth in global container demand to 1% to 2%, from 1% to 3%, for 2019. The better news is the forecast of 1% to 3% growth for 2020 looks more optimistic, but the company’s depressed share price suggests investors remains unconvinced.

Its longstanding relationship with the FTSE All-World index broke down in 2017 and has yet to recover. It could therefore be argued there is a growing disconnect between cheap-money fuelled markets and the underlying macroeconomic and corporate profit picture.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.