Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineUK GDP figures are set to get worse

The stress on the UK economy and on public finances from the coronavirus continues to be very evident.

This has implications for the markets, inflation and sterling as we move into the third quarter. Also looming large on the horizon is an apparent end of September deadline set by the UK Government for its trade talks with the European Union.

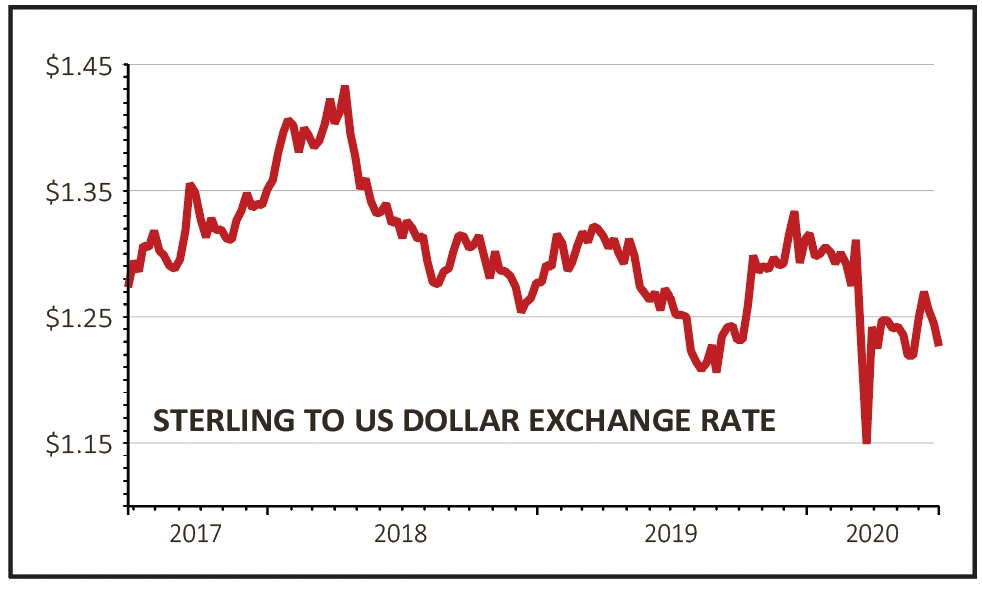

With the latest GDP update revealing downward revisions to first quarter estimates, the fall of 2.2% being the joint worst since 1979, sterling remains under pressure against other major currencies.

If an agreement isn’t reached with the EU in the coming months, then the lows of $1.159 seen in late March could be retested.

Growth figures for the second quarter look set to be worse than Q1 given April has already been revealed to have seen a record monthly contraction of 20.4%, likely outweighing any rebound in May and June.

Against this backdrop the UK’s debt management office announced plans (29 Jun) to sell a further £50 billion worth of government bonds (gilts) by the end of August taking total issuance for the first five months of the current fiscal year to a record £275 billion.

For context this compares with £136.8 billion for the whole of the 2019/20 fiscal year as the country looks to meet the cost of the current furlough schemes and increase infrastructure spending.

There are suggestions that the Bank of England may buy fewer government bonds in the future as part of its asset purchase scheme than it did in the initial stages of the coronavirus crisis.

Investment bank Morgan Stanley noted that the 18 June Monetary Policy Committee (MPC) meeting hinted that the Bank of England might even start selling government bonds with its governor Andrew Bailey indicating the size of the bank’s balance sheet could be an issue.

Morgan Stanley commented: ‘After these confusing signals, we hope to get more clarity on MPC thinking in upcoming speeches and at the August MPC meeting.

‘We expect a negative rates package in November, given diminishing effectiveness from QE (quantitative easing) and the need for additional action to get inflation back to target.

‘And we don’t think that the bank will be able to walk away from the gilt market, given the risk of ongoing high issuance driving higher yields.’

UK economy – key dates to watch

6 August – MPC meeting

12 August – First estimate of UK Q2 GDP

30 September – Apparent deadline set by UK Government on Brexit talks

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.