Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

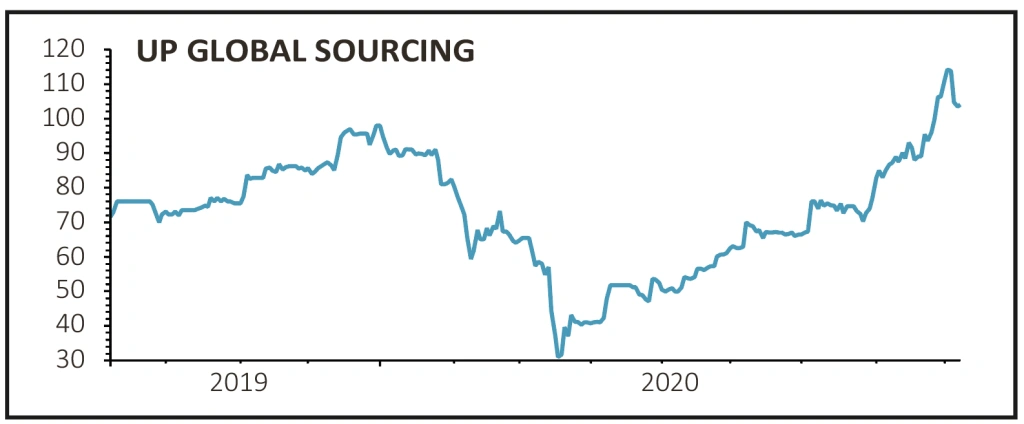

magazineUP Global Sourcing gets back on analysts' radars

UP Global Sourcing (UPGS) 102.1p

Gain to date 8.9%

Original entry point: Buy at 93.7p, 27 August 2020

Owner of value-focused consumer brands UP Global Sourcing (UPGS) delivered on its guidance for full-year earnings before interest, tax, depreciation and amortisation, reporting £10.4 million on 7 September, down 3.3% year-on-year.

The trading statement prompted Shore Capital to reintroduce medium-term forecasts with the broker looking for mid-to-high single digit growth which it believes ‘offers upside risk, reflecting the group’s broadening channel and customer mix’.

UK and international online sales were up 47.2% to £16.7 million and accounted for 14.5% of group revenues, up by more than half from the 9.2% last year. Meanwhile the concentration of customers reduced significantly with the top two names now accounting for around a fifth of group sales, down from almost 35% in 2019.

The tight management of working capital and accelerated turnover of inventory that was a feature of 2020 is expected to reverse next year as normal trading and ordering patterns emerge.

With year-end net debt down to £3.8 million from £14.4 million, the company has considerable headroom of £21.3 million according to Shore Capital.

It is forcast to pay 4.2p in dividends for the year to July 2021.

SHARES SAYS: Still a buy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.