Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazine50,000 buy a home with a Lifetime ISA and £1.1 billion tucked away for kids

It’s sad to admit, but there is a flutter of excitement that ripples through the personal finance industry when HMRC releases its ISA statistics every June. The figures reveal a host of interesting trends about what everyday savers are doing with their money, and the latest data dump was no exception.

Probably the biggest shift in consumer behaviour revealed by HMRC was a big move away from cash towards stock market ISAs. The numbers show that in the tax year ending 5 April 2021, a record £34 billion was invested in Stocks & Shares ISAs, which was £10 billion more than the previous year.

Clearly the arrival of successful Covid vaccines, combined with high levels of pandemic savings and ultra-low interest rates, gave investors both the means and motivation to put a huge wall of money to work in the stock market.

Cash ISAs didn’t enjoy such a widespread boom in popularity though. HMRC data reveals that 1.6 million fewer people opened a Cash ISA than in the previous tax year, and total contributions fell by £12 billion to £36.9 billion.

POWER OF THE PERSONAL SAVINGS ALLOWANCE

A resurgent stock market stole the limelight from the paltry rates that were on offer from Cash ISAs, but more broadly Cash ISA subscriptions have been in decline since the personal savings allowance was introduced in 2016.

This allowance allows savers to receive up to £1,000 of interest tax-free, which undermines the need for many consumers to use a Cash ISA wrapper to protect their money from tax.

That’s particularly the case when interest rates are low. At an interest rate of 1%, a basic rate taxpayer would need £100,000 in cash before they benefited from the Cash ISA wrapper, because of the personal savings allowance protecting that level of interest from tax.

But as interest rates rise, Cash ISAs will probably enjoy a bit of a popular recovery, both because the rates themselves will become more attractive, and more people will save tax by using the ISA wrapper.

At an interest rate of 3%, basic-rate taxpayers start being liable for tax once their cash savings outside of an ISA exceed £33,333. For higher-rate taxpayers it’s half this level as they only receive a £500 annual allowance, and additional-rate taxpayers don’t get any allowance at all.

SAVING FOR CHILDREN

Junior ISA subscriptions also hit a record level of £1.1 billion, the first time they have breached the £1 billion mark for the year to 5 April 2021.

But cash is still king in the land of the Junior ISA, accounting for over 57% of subscriptions in the tax year ending 2021. So, while parents seem to have shifted towards the stock market with their own ISAs, they have been more reluctant to do so with their children’s savings.

That doesn’t make a huge amount of investment sense, given that children potentially have the longest savings horizon in which to ride out the ups and downs of the stock market.

However, some parents may be saving for a specific event at age 18 which truncates the investment period, such as a university fund, while others may simply be conditioned to dealing in cash when it comes to saving for children.

But for younger children especially, some parents may well be missing a trick by tuning away from the long-term growth potential offered by investing in the stock market.

GETTING ON THE PROPERTY LADDER

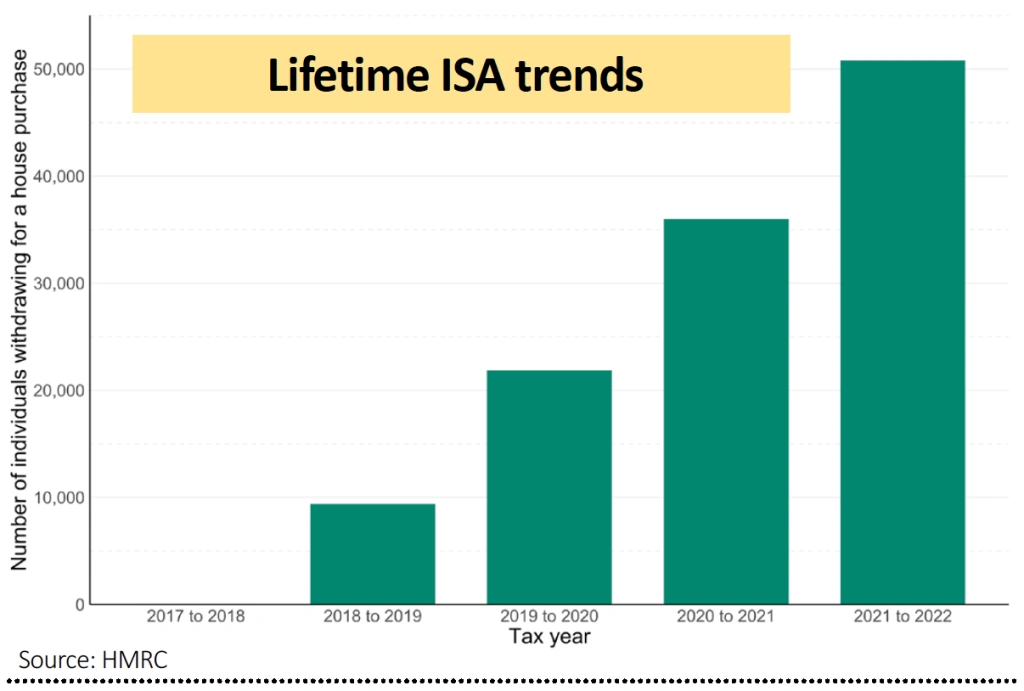

There is more up-to-date information on Lifetime ISAs. Over 50,000 people used a Lifetime ISA to buy their first house in year to 5 April 2022, which brings the total number of individuals who have used this scheme to purchase a property to 118,100.

On average withdrawals were £13,192, which means that the typical Lifetime ISA encasher benefited from around £2,600 of upfront government tax relief, including the growth on that money.

While some criticised the scheme when it was introduced in 2017, it has clearly helped lots of people to get on the housing ladder and will continue to do so as more accounts mature.

The government did temporarily reduce the early exit penalty charge during the pandemic from 25% to 20%, and they could look at this again to help with the cost-of-living crisis.

That would aid those who have done the right thing by saving for their future, but now find themselves in more difficult financial circumstances and in need of access to that money.

ISAS HAVE BEEN A SUCCESS

In total, £687 billion was held in adult ISAs as of 5 April 2021, which really is a mark of success of the ISA product in its 21st anniversary year.

There are 27 million adult ISA holders in the country, almost evenly split between genders, and the average ISA holder had an income of between £20,000 and £29,999, which all goes to show that the ISA is really a building block for pretty much anyone who wants to save money for their future.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Funds

Great Ideas

- Fulham Shore is navigating cost pressures well and continues to expand

- Buy shares in Photo-Me for its underappreciated earnings potential

- Watches of Switzerland's shares have fallen too far, buy them now

- Don't worry about slowing orders at Chemring as it looks well placed

- Cheniere Energy outperforms the global stock market

- Still plenty of reasons to want to invest in this property expert

News

- Apple’s push into advertising poses challenges for Meta, Alphabet and Snap

- Airline shares dive amid prospect of high compensation costs

- Why shares in Primark parent Associated British Foods are languishing near five-year lows

- How decades high US inflation and new ECB direction are leading to market turmoil