Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

With its leading market share in major domestic appliances, AO World’s problem has never been delivering the goods, but doing so in a profitable way, and as a result the latest set of full-year results represents a major step forward.

The shares are still miles below 2014’s flotation price of 285p, let alone 2021’s pandemic peak north of 400p but improved profits and cash flow could help to persuade the company’s £650 million stock market price tag is justified, or even too low.

Source: LSEG Datastream

AO has a 15% market share in the major domestic appliance market and has a share of almost a third in the online arena. It has pushed through a major restructuring as part of its ‘Pivot to Profit’ strategy, following prior withdrawals from the Netherlands (2019) and Germany (2022) and the profit and loss account has started to show the benefit.

Earnings improved in the year to March 2024 despite a 9% drop in sales down to £1 billion – the third straight decrease in annual sales since the go-go days of the pandemic and lockdowns, when consumers were stuck at home and many of those whose incomes were unaffected (or even boosted as commuting and other expenses fell) spent freely on their houses and home improvement.

Source: Company accounts, Marketscreener, consensus analysts’ forecasts

Times have got tougher for many consumers since the pandemic ended (not necessarily what anyone would have expected), thanks to the oil and energy price shock, galloping inflation and a sharp upward move in interest rates and borrowing costs from generational lows.

The share prices of electricals and consumer electronics retailers such as Currys and Marks Electrical reflect this situation just as clearly as the stock market valuation of AO.

However, the GfK survey on UK consumer confidence, and the sub-index that looks at sentiment toward making major purchases such as white goods, is on the rise, helped by cooler inflation, robust wage growth, lower energy price caps and the prospect of lower interest rates from the Bank of England at some stage, perhaps in the not-too-distant future.

Source: LSEG Datastream, GfK

These factors, as well as the company’s own initiatives to make customers stickier and drive repeat purchases, when appropriate, such as AO Five-Star Membership, AO Finance and the partnership with Frasers, presumably underpin founder and chief executive John Roberts’ goal for double-digit percentage revenue growth in the year to March 2025.

Add that planned improvement in the top line, also boosted by the introduction of delivery fees, and ongoing cost control as part of the ‘Pivot to Profit’ plan and AO World could serve up another increase in earnings in the coming year.

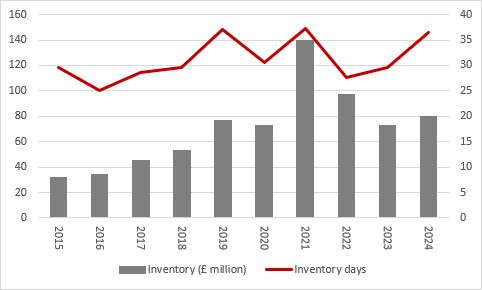

Having closed its Dutch and German businesses, AO World continues to focus on tight control of inventory and marketing costs, as well as increased automation and efficiencies at the firm’s five distribution centres.

Stock turn is already pretty speedy at 36 days and keeping that high will reduce the need for discounting to shift unsold product and boost margins in the process.

Source: Company accounts

Online delivery of such keenly priced, largely commoditised products such as white goods, is never going to be a fat-margin enterprise, as the company’s ultimate goal of a 5% adjusted pre-tax return on sales attests, but analysts believe that underlying pre-tax profit will rise again in the coming year to £39 million, compared to £34 million in the year just ended.

Source: Company accounts, Marketscreener, analysts’ consensus forecasts

“That equates to net profit of around £25 million, so AO World’s current stock market valuation of some £650 million still comes in at 26 times that figure – and a 26-times earnings multiple is more than twice the rating afforded the entire UK equity market by investors.

“That is punchy, given the relatively thin margins on offer, and the highly competitive nature of the business. A strong balance sheet is one point in the company’s favour, as it has net borrowings of just £31 million including leases, and another is growth, at least if AO World can meet Mr Roberts’ long-term ambitions of sales growth of 10% to 20% a year, 5% adjusted pre-tax profit margin and strong cash conversion.”

These articles are for information purposes only and are not a personal recommendation or advice.

Written by:

Russ Mould

Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

Ways to help you invest your money

Put your money to work with our range of investment accounts. Choose from ISAs, pensions, and more.

Let us give you a hand choosing investments. From managed funds to favourite picks, we’re here to help.

Our investment experts share their knowledge on how to keep your money working hard.

Related content

- Fri, 13/06/2025 - 11:30

- Mon, 09/06/2025 - 10:43

- Fri, 06/06/2025 - 11:25

- Fri, 30/05/2025 - 13:55