Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

Financial markets had assumed that Trump would talk tough on tariffs and back off when he got a deal, so the US president’s plan to act first and then (perhaps) talk has come as a nasty surprise to share prices around the world, especially as Canada and Mexico have already threatened retaliation. Trump’s launch of tariffs in 2018 did raise revenues for America but US corporate profits took a hit that year and America’s S&P 500 index fell by a fifth, so markets have understandably taken fright this time around.

Weirdly, stock markets have begun Trump’s second term in boisterous form, in marked contrast to 2016’s election result when they approached the Republican candidate’s win with caution. Ultimately, the S&P 500 gained 56% during Trump’s first term, but that came with a big wobble in 2018, when the index lost 5% overall and endured a mini bear market in the autumn, as threats of tariffs on China became reality.

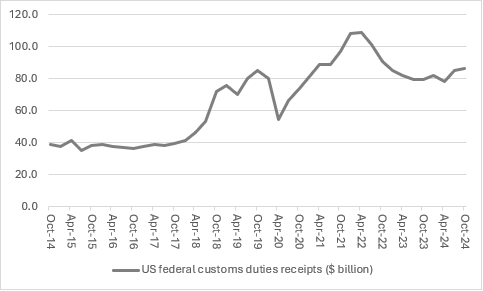

America’s tax take did benefit, as customs duties doubled in short order. The tattered state of US federal finances, where the debt is far higher now and the interest bill is surging, means this offers some good news, from an American perspective.

Source: FRED – St. Louis Federal Reserve database

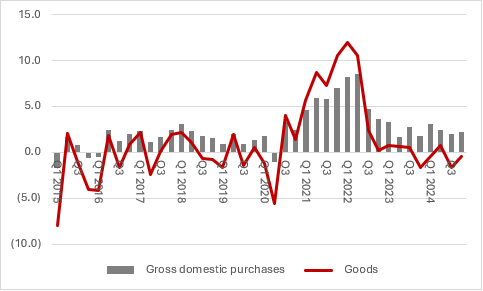

Nor did inflation spike, to perhaps assuage current financial market fears that higher tariffs will mean higher prices and higher prices will mean higher interest rates. Data from the US Bureau of Economic Analysis shows the price increases for gross domestic purchases across the American economy generally and for personal consumption of goods eased in 2018 and 2019, despite the Trump tariffs.

Source: US Bureau of Economic Analysis

This may have been because the best cure for high prices is just that – high prices – with the result that consumers and companies refused to pay them and sought out cheaper options (which is precisely the Trump plan this time around). But it may have also been because American importers and foreign sellers into the US elected to take the hit on margin and did not pass on the cost impact of the tariffs.

US corporate profits stalled in 2018 and actually shrank as a percentage of GDP, with the latter again suggesting that companies just took the margin hit and did not run the risk of losing revenue if they jacked up prices.

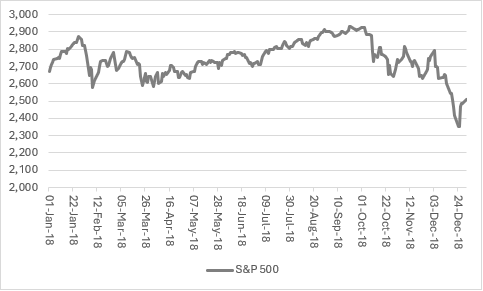

US stock markets did not like that at all. The S&P 500 started 2018 well but finished it badly, as a one-fifth fall in the autumn wiped all of the year’s gains – and more.

Source: LSEG Refinitiv data

This is a worry. According to data from Standard & Poor’s, the US equity market started 2018 on 23 times forward earnings and ended it closer to 19 times, thanks to the autumnal slump.

This time around, markets are welcoming, not worrying, about Trump. Analysts expect 17% corporate profits growth in 2025, and the S&P currently trades on 24 times earnings (based on that 17% growth assumption). Any disappointment could have the same impact, if not greater, than it did seven years ago.

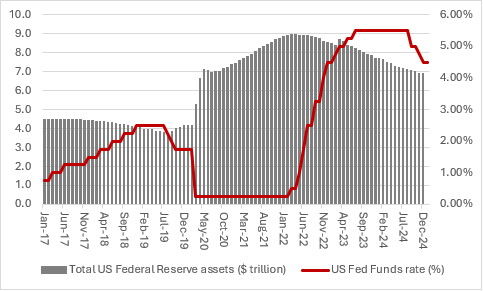

One big hope is that the tariffs do not last, while another is that the US Federal Reserve helps out with some interest rate cuts, something for which Trump is already calling. Rate cuts in 2019 did help get the S&P 500 on track (and then more QE and more reductions in the headline cost of borrowing in response to Covid-19 provided a torrent of cheap liquidity which markets thoroughly welcomed).

But back in 2018, the Fed was raising rates and had stopped growing its balance sheet. In 2025, thus far, it has paused rate cuts and continued to shrink its balance sheet as part of its Quantitative Tightening programme.

Source: FRED – St. Louis Federal Reserve database

This could help to keep demand and inflation in check, but it might not do much for the 17% forecast of profits growth and maybe the biggest challenge of all for US equities (and perhaps global equities) is that expectations and valuations are simply higher than they were seven years ago – even the precedent of the impact of tariffs offered little encouragement.

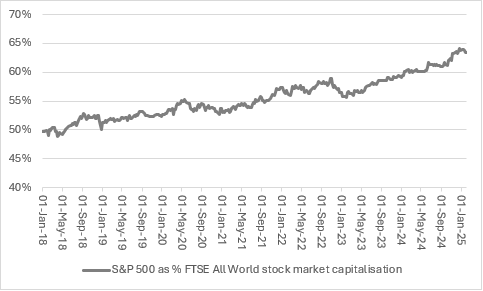

Any monetary policy response – or the lack of it – and the duration of the tariffs and retaliatory responses are now key variables that investors need to assess. A brief skirmish that leads to a deal may ease stock market concerns. However, Trump is already warning of the need for short-term pain in exchange for the long-term gains of higher tax income from duties and then higher domestic output and employment as buyers shun imported options made more expensive by tariffs, so it could be a bumpy ride, especially given how US equities are more expensive than they were seven years ago and how they now represent 65% of global market cap, compared to 50% in 2018.

Source: LSEG Refinitiv data

Ways to help you invest your money

Put your money to work with our range of investment accounts. Choose from ISAs, pensions, and more.

Let us give you a hand choosing investments. From managed funds to favourite picks, we’re here to help.

Our investment experts share their knowledge on how to keep your money working hard.

Related content

- Fri, 13/06/2025 - 11:30

- Mon, 09/06/2025 - 10:43

- Fri, 06/06/2025 - 11:25

- Fri, 30/05/2025 - 13:55