Policy statements on trade, the tariffs and the dollar from Washington and Beijing are dominating the headlines and the attention of stock, bond, commodity and currency markets. But investors must pay heed to what is going on in Tokyo, too.

A major rally in the yen was fingered as the cause of last August’s brief stumble in share prices around the world and another surge in the Japanese currency is evident now, as financial markets endure another unexpected bout of volatility.

This may not be a coincidence. The Yen has been a source of global liquidity, as major market players have shorted it, borrowed against it and used that money to go buy risk assets around the globe.

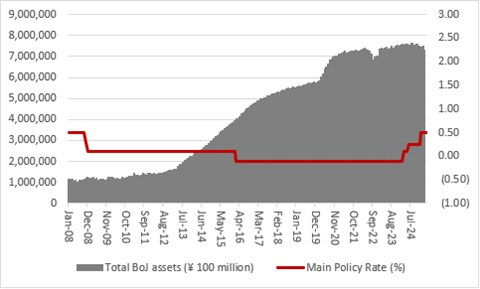

They have been able to do so because interest rates in Japan have been so low, much lower than elsewhere, and the Bank of Japan has also continued to run its Quantitative and Qualitative Easing (QQE) programme to a level way in excess of the monetary stimulus applied by central banks in the West.

Source: Bank of Japan, FRED — St. Louis Federal Reserve database, LSEG Refinitiv data

Cheap yen have therefore been one major source of the tidal wave of cash that has done much to boost share prices worldwide.

Japan’s fiscal policy

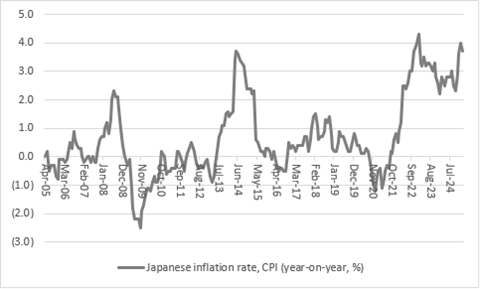

However, interest rates are now on the rise and the Bank of Japan (BoJ) is curbing growth in its balance sheet as inflation finally rears its head in the country after near forty years of disinflation and even outright deflation.

Inflation is now running at 3.7% year-on-year in Japan, based on the headline consumer price index benchmark, a figure that is almost twice the target sought by Bank of Japan governor Kazuo Ueda and his colleagues.

Source: LSEG Refinitiv data

The yields on benchmark Japanese Government Bonds (JGBs) have shot higher, to attract capital and thus buyers — not sellers, of the yen.

After three gentle increases in the Main Policy Rate to 0.5%, the highest mark since 2008, the scene is now set for the BoJ’s next policy meeting on 1 May. In theory, Mr Ueda and his team would like to sanction another hike to ensure inflation does not remain sticky and also, perhaps, to appease bond vigilantes who are starting to push policymakers around the world over.

Consequences of a rate hike

But rate hikes could attract further capital to Japan, stoking the yen’s rise and bringing three complications.

One could be the ongoing unwind of the carry trade, as losses on yen shorts by foreigners persuade them to close out their shorts and buy back more yen to fuel further gains in the Japanese currency, to perhaps create a circle every bit as vicious as it had previously been virtuous.

Another could be how yen gains inflict losses on Japanese holdings of overseas assets, notably US Treasuries, of which Japan is the single biggest foreign owner, with some $1.1 trillion in US government bonds. If Japanese holders start to sell, Treasury prices could go down and yields go up, to further complicate the growth and economic outlook in the USA, in an example of just how inter-linked global financial markets, capital flows and economies now are, whether national leaders like it or not.

And finally, for Japan itself, yen strength is potentially bad for exports and economic growth, at a time when President Trump’s tariffs are already a potential obstacle to the sale of Japanese goods.

The yen may therefore have a pivotal role in both the global economy and global financial markets as both continue to feel the reverberations of President Trump’s tariff and trade policies.

If last summer’s — brief — market squall did indeed have its roots in the yen’s rise, then investors may need to buckle up once more if the Japanese currency maintains its current upward run against the dollar.

Written by:

Russ Mould

Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

Ways to help you invest your money

Put your money to work with our range of investment accounts. Choose from ISAs, pensions, and more.

Let us give you a hand choosing investments. From managed funds to favourite picks, we’re here to help.

Our investment experts share their knowledge on how to keep your money working hard.

Related content

- Fri, 13/06/2025 - 11:30

- Mon, 09/06/2025 - 10:43

- Fri, 06/06/2025 - 11:25

- Fri, 30/05/2025 - 13:55