Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineClipper continues to ride online wave

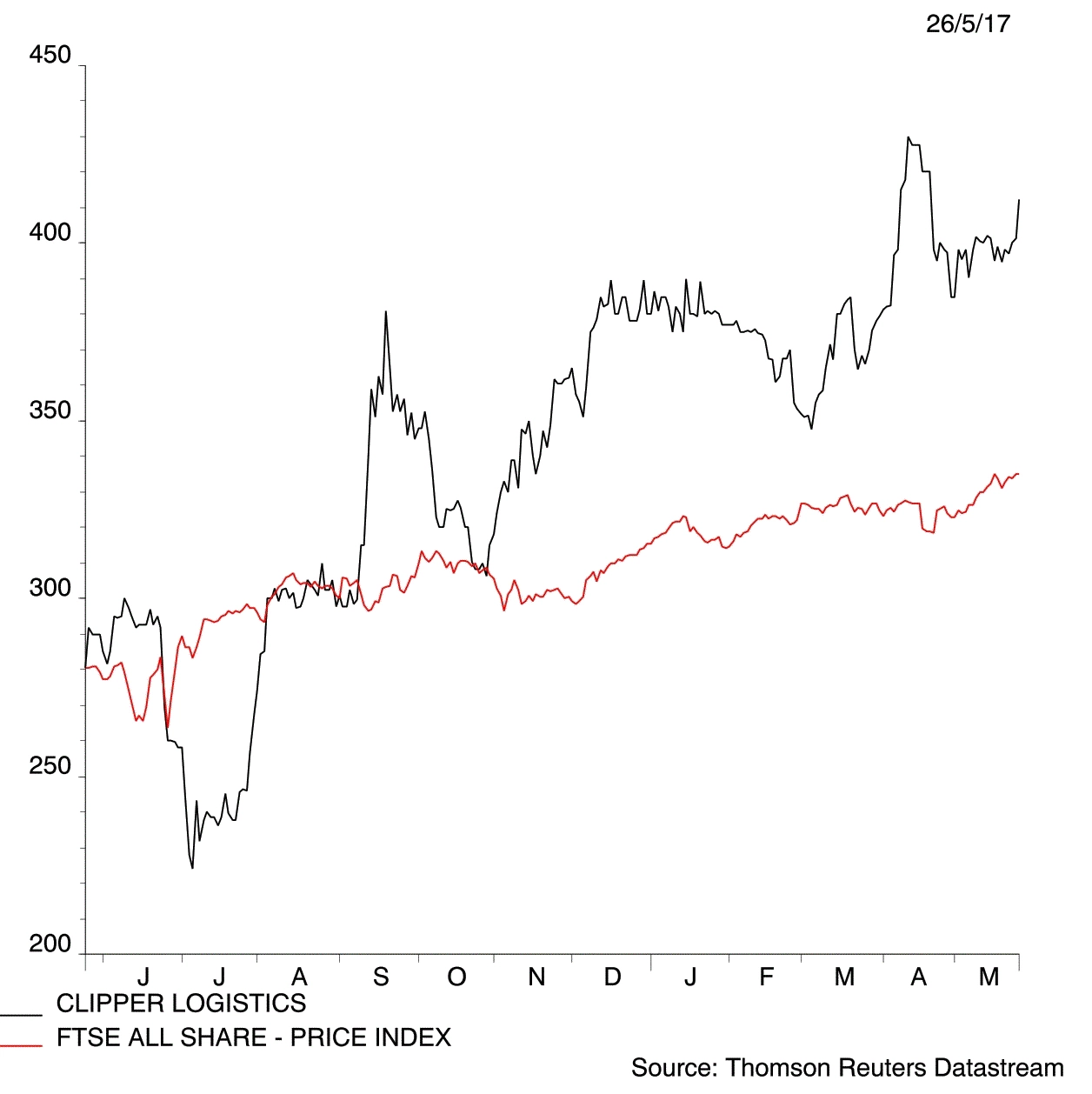

Clipper Logistics (CLG) 420.2p

Gain to date: 36.9%

Original entry point: 307p, 1 September 2016

Our bullish call on Clipper Logistics (CLG) is now a tidy 36.9% in the money. Geared into the growth of online shopping, the fashion logistics specialist runs warehouses and delivery services for retailers, sending out clothes ordered via websites and handling returns.

Its ‘sticky’ customers include ASOS (ASC:AIM), John Lewis, Sainsbury’s (SBRY), SuperGroup (SGP) and Halfords (HFD); Clipper recently signed (3 May) a new eight-year contract with the latter and also counts British American Tobacco (BATS) as a customer.

Clipper’s high-flying shares were helped higher by upgrades following the acquisition (25 May) of Tesam. Buying this smaller, Peterborough-based peer ‘provides additional capacity, at an attractive location, at an attractive price, and enhances the ability of the group to implement its strong pipeline of new business’, according to Numis Securities.

For the year to April 2018, the broker has upgraded its pre-tax profit forecast from £18.4m to £20m. Based on estimated earnings of 15.3p, Clipper isn’t cheap on a prospective PE of 27.5 times, although we think its structural growth story and strong cash generation justify a premium rating.

Keep buying high-quality Clipper at 420.2p. (JC)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.