Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineLuceco knocks lights out again

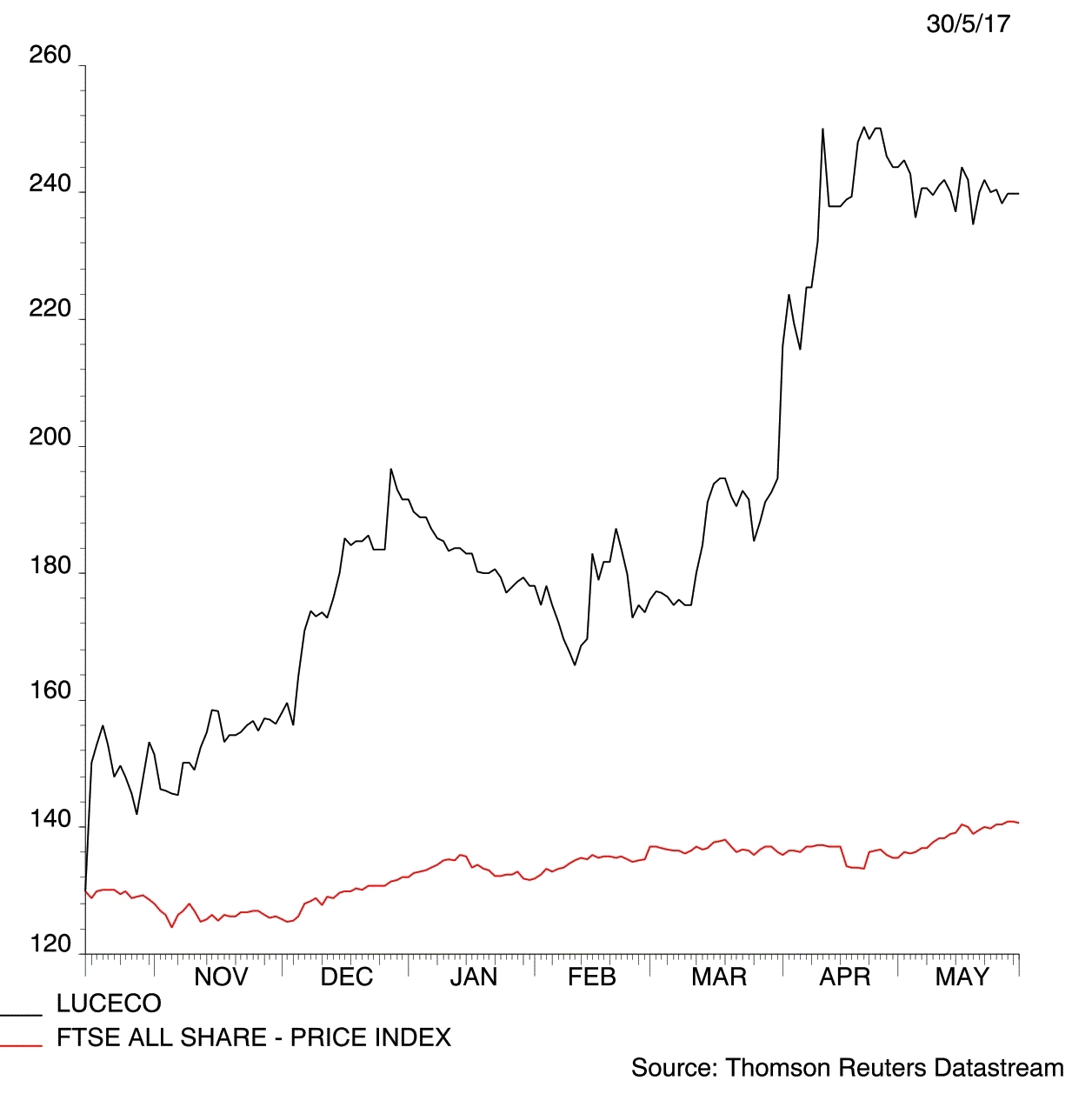

Luceco (LUCE) 239p

Gain to date: 59.3%

Original entry point: Buy at 150p, 20 October 2016

Our positive view on LED lighting specialist Luceco (LUCE) continues to be underpinned by robust operational performance. Luceco makes and distributes wiring accessories, power products and LED lights. It has a diversified customer base, selling to trade, retail and direct to businesses for specific projects.

In an AGM trading update on 25 May the company guided for results to be slightly ahead of expectations. It says the momentum flagged in full year results has continued with ‘significant year on year growth in revenue and profit’.

‘Growth has been driven by strong market share gains within the key brands in the UK and other newer markets, and the ongoing expansion of the product ranges,’ it adds.

The company has an edge on the competition thanks to its low-cost manufacturing facilities in the Far East and we remain positive for now as there is little sign of the trading weakness which we said might lead us to take profit.

The shares are up more than 80% on the 130p issue price from its October 2016 IPO. The UK LED lighting market is expected to enjoy 15.4% compound annual growth between 2015 and 2020, according to AMA Research.

Not reason to sell yet. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.