Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineElectrocomponents increasingly well placed

Oxford-based Electrocomponents (ECM) is the UK’s largest international industrial distribution company. It operates across 90% of the world’s GDP so is a true global player offering a dizzying array of goods to engineers including tools, safety equipment and semiconductors.

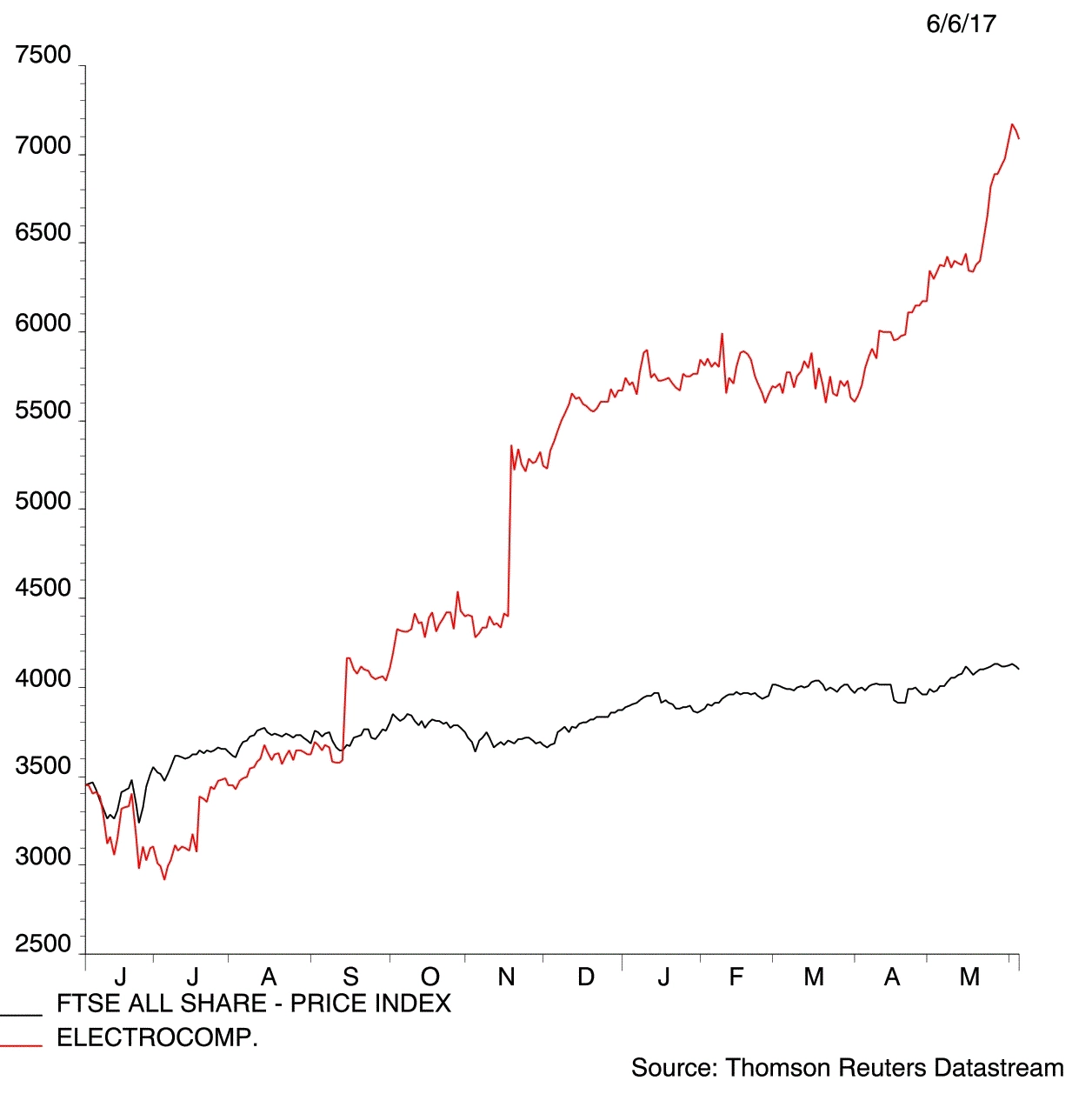

2017’s results to end of March show a company on the ascendancy with perhaps the key takeaway a hike in its dividend for the first time in five years.

Looking to 2018, broker Liberum is upgrading its earnings per share by 4%, reiterating its ‘buy’ rating and increasing its target price from 500p (which Electrocomponents has already surpassed at the current 597.5p) to 660p.

Conservative assumptions

The broker is basing this upgrade on its discounted cash flow valuation, which involves assumptions on its long term growth rate and levels of capital expenditure. As this type of valuation is extremely sensitive to assumptions made, Liberum says it has stayed within conservative estimates.

These include a long term growth rate assumption of 2.5% and a capital expenditure to depreciation ratio of one-times. This last point is highly conservative as it suggests Electrocomponents will purchase the same amount of equipment at the same rate other pieces depreciate.

Last year’s gross margin was 43.4% so LIberum’s long-term gross margin assumption of 45% doesn’t look too rich. Although its future earnings before interest and tax margin of 11.3% might seem high compared to the 8.8% delivered in 2017.

Further upside from acquisitions

The broker says further upside can be achieved if Electrocomponents engages in some acquisitions. It has also been impressed by innovations from the company such as DesignSpark, a range of software packages allowing the user to reverse engineer objects among other uses.

Chief executive Lindsley Ruth has played a big part in the turnaround of Electrocomponents since joining in 2015. The company’s share price has risen around 120% since he took the helm.

Liberum describes the management’s approach as being to ‘under promise and over deliver’ and says its success justifies its premium valuation

As Electrocomponents is a diverse company, comparing it to a peer group is difficult. While Reuters includes staffers such as Pagegroup (PAGE) as its peers, Liberum’s peer group seems closer to the mark with engineering and electronic distributers. According to Liberum’s peer group, Electrocomponents trades on the highest price to earnings ratio of 25.6-times. Is this warranted?

While Robin Speakman of Shore Capital Markets says it would be a ‘stiff challenge’ sustaining historic growth rates, the direction of the firm seems to suggest it can keep up the pace. (DS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.