Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineSmaller asset managers are looking attractive

Several of the market’s smaller asset managers have been having a great year on the stock market, putting the spotlight on the companies that run funds rather than individual funds themselves.

Investing in asset managers has definite risks, as investor sentiment can change quickly and the barrage of regulation can increase the costs of doing business.

However, investors are clearly finding something positive in the sector at present, so let’s take a look at three relevant stocks on the UK market.

Liontrust Asset Management (LIO)

Share price gain year to date: 17.1%

Latest share price: 453.3p

The firm’s chief, John Ions, says the key to an asset manager’s success is delivering a ‘clearly articulated strategy.’

The boss also points to the importance of his fund managers having ‘skin in the game’ (personal money in the funds they manage). ‘If there is a culture of fund managers investing in the funds they run, it shows a belief in and a commitment to their investment processes and fellow investors.

’Liontrust’s assets under management (AUM) grew by 36% to £6.5bn for the year to 31 March 2017. A further £2.5bn AUM was automatically added on 1 April when Liontrust completed a deal to buy Alliance Trust Investments.

Ions says 96% of the company’s actively-managed unit trust funds by AUM have outperformed their benchmark since launch, objective change or fund manager inception.

The company launched in 1995 and has been listed on the UK stock market since 1999. It now has 28 funds covering a broad range of themes including income, growth, special situations, ethical and smaller companies.

The company launched in 1995 and has been listed on the UK stock market since 1999. It now has 28 funds covering a broad range of themes including income, growth, special situations, ethical and smaller companies.

N+1 Singer says Liontrust’s most recent full year performance was £0.3bn better than expected, in AUM terms. It forecasts adjusted pre-tax profit moving from £14.6m in 2016 to hit £16.6m in 2017 and £24.9m in 2018. Full year results are expected to be published later in June.

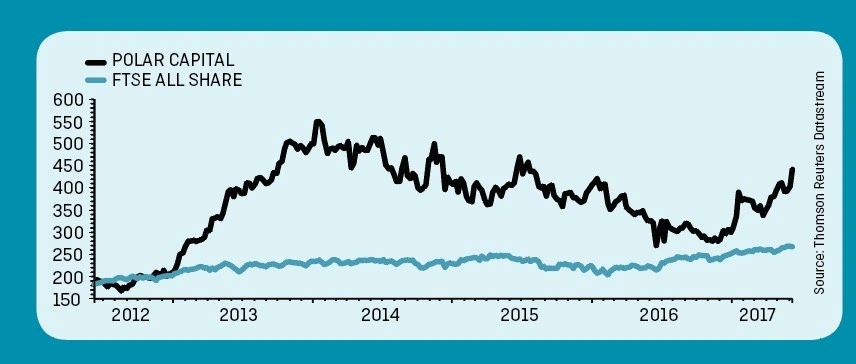

Polar Capital (POLR:AIM)

![iStock-498735438-[Converted]polarbearok](https://www.sharesmagazine.co.uk/wp-content/uploads/2017/06/iStock-498735438-Convertedpolarbearok.jpg)

Share price gain year to date: 48.6%

Latest share price: 445.75p

Polar Capital’s increased breadth of funds, combined with the positive fund performance, should provide more stability and a lower business and financial risk profile going forward, says Canaccord Genuity.

Asset manager Polar Capital in April reported its second consecutive quarter of net inflows and a 27% rise in AUM to £9.3bn for the 12 months to 31 March 2017.

‘A number of (Polar’s) funds have seen considerable levels of net inflows throughout the year, in particular Technology, Healthcare and Insurance, resulting in a marked improvement in the diversification of the group’s AUM compared to recent years,’ adds Canaccord.

We would also add in the success of its Polar Capital UK Value Opportunities Fund (IE00BD81XX91) which amassed c£170m of assets under management in just two months since launching in January 2017.

A key risk to the investment case is the dividend where Polar guides for 25p per share in 2017 and 2018. Canaccord says the payment is greater than its forecast earnings per share.

Impax Asset Management (IPX:AIM)

![]()

Share price gain year to date: 40.6%

Latest share price: 92p

Impax reported a 27% increase in assets under management to £5.7bn when it reported half year results on 11 May. The dividend was lifted by an impressive 40% to 0.7p per share, something which ‘reflects the strong performance of the business and confidence in the coming years’ according to Peel Hunt analyst Stuart Duncan.

Most of the asset managers we interviewed for this article pointed to a desire for genuine active management as a reason for the recent rise in their firms’ fortunes.

Impax’s chief executive Ian Simm says that making people aware of the stock was invaluable as well.

‘At this sort of market cap (c£117m), a bit of PR (aka publicity) brings in retail buyers. If you don’t have that communication you’re left in the hands of institutional investors,’ says Simm. His point is that retail interest makes the stock more liquid and easier to trade.

The asset manager’s focus is on environmental markets although Simm insists the firm does not wear the ethical investor badge.

Companies on Impax’s radar involved with clean energy, waste management and sustainable food are actually growth stocks which should appeal to the ‘red blooded capitalist’ according to Simm.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- 30% Shoe Zone’s sure-footed digital steps

- 72: WPP needs to plan for life after Sorrell

- Worst Performing FTSE Small Cap Stocks

- FTSE Small Cap Stocks

- Shareholders owning 18.4% of Gem Diamonds try to oust CEO

- Toople has lost three quarter of its value in a year

- 46,595 AIM stocks in demand

- Boohoo founder and family cash in £80m of stock