Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineQueen’s Speech fails to address savings issues

While Brexit is clearly sucking up huge amounts of policy time and resource, there remains a significant domestic reform agenda for the Government to undertake.

Unfortunately Theresa May’s dramatic loss of power following the general election means a number of vital retirement reforms were watered down or simply not mentioned in last week’s Queen’s Speech.

Ageing society – reforming the state pension

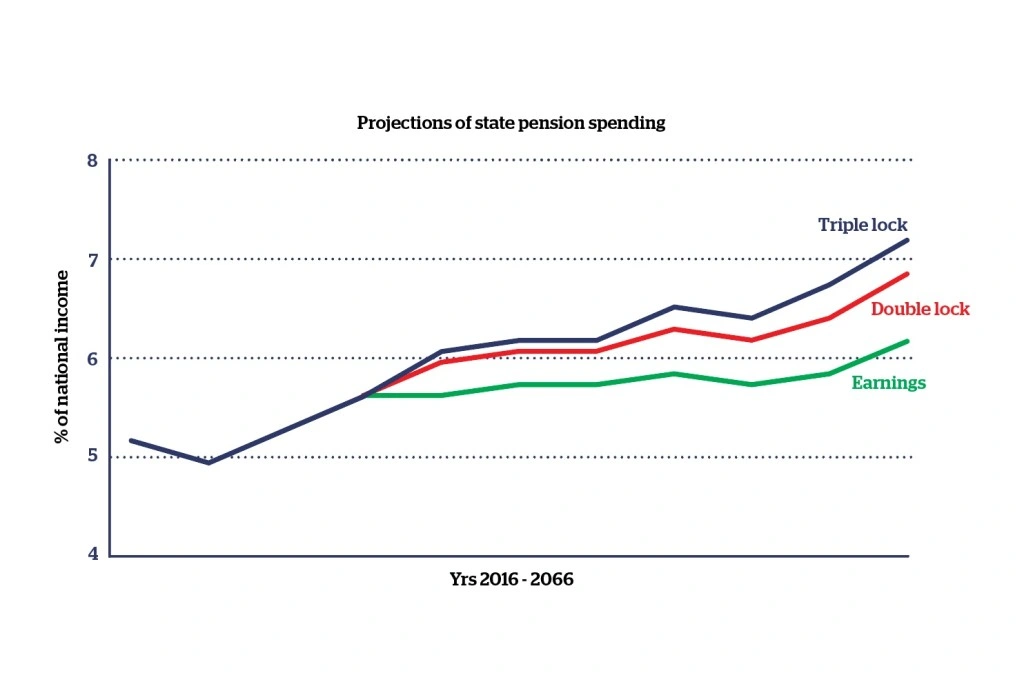

The ageing society is arguably the key challenge facing policymakers. Nowhere is this demonstrated more clearly than in the rising cost of the state pension.

The Institute of Fiscal Studies estimates the state pension will cost an extra £30bn in today’s terms in 50 years’ time.

As part of a programme to control these costs, the Conservative manifesto proposed scrapping the triple lock – which guarantees yearly increases in line with the highest of earnings, inflation or 2.5% – and replacing it with a double lock to earnings and inflation.

Furthermore, an independent report produced prior to the election backed a raise in the state pension age much faster than under current plans.

Reports suggest the triple-lock will now be retained as part of a deal with the Democratic Unionist Party, while Labour’s opposition to the proposed state pension age hike means this vital area of reform faces short-term political deadlock.

This state pension system is unsustainable over the long-term and, at some point, someone will need to either reduce the amount people receive or increase the qualifying age.

Unfortunately the Prime Minister has a wafer thin majority so bold, necessary reforms to increase the state pension age risk being kicked into the long grass.

MPAA and pension scams clampdown

With all the noise surrounding Brexit negotiations it’s easy to forget vital domestic personal finance reforms need addressing.

Savers who access their pension flexibly from age 55 are subjected to a lower annual tax-free pension saving allowance, known as the Money Purchase Annual Allowance (MPAA).

The Government announced a cut in the MPAA from £10,000 to £4,000 effective 6 April this year – but the legislation to make this happen was never enacted, meaning it is not clear which figure applies this year.

People who have used the pension freedoms need urgent clarity on this issue so they know how much they can put into

their pot tax-free in the current fiscal year.

We are also still waiting for the Government to implement a crucial clampdown on pension scammers, including a ban on cold-calling. These are incredibly important consumer protection measures that must not be further delayed.

Tom Selby,

Senior Analyst, AJ Bell

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

Editor's View

Great Ideas Update

Investment Trusts

Larger Companies

Main Feature

Money Matters

Smaller Companies

Story In Numbers

- Petropavlovsk co-founder kicked off the board after 23 years’ service

- Which FTSE 350 Shares have Lost Shareholders Money

- Which FTSE 350 Shares Rewarded Shareholders

- $390bn wiped off global drug sales forecasts

- 98.6% vote in favour of Standard Life/Aberdeen merger

- London’s shrinking bank industry

- 150M Hurricane blows Crystal Amber down