Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineXP Power has potential to beat earnings forecasts

We believe XP Power (XPP) is an under-appreciated growth story. It has a super income track record with plenty of scope for capital returns.

The £464m power switching components supplier has paid out 444p per share in dividends over the past 10 years, including 2016’s 71p payout, up from 66p in 2015.

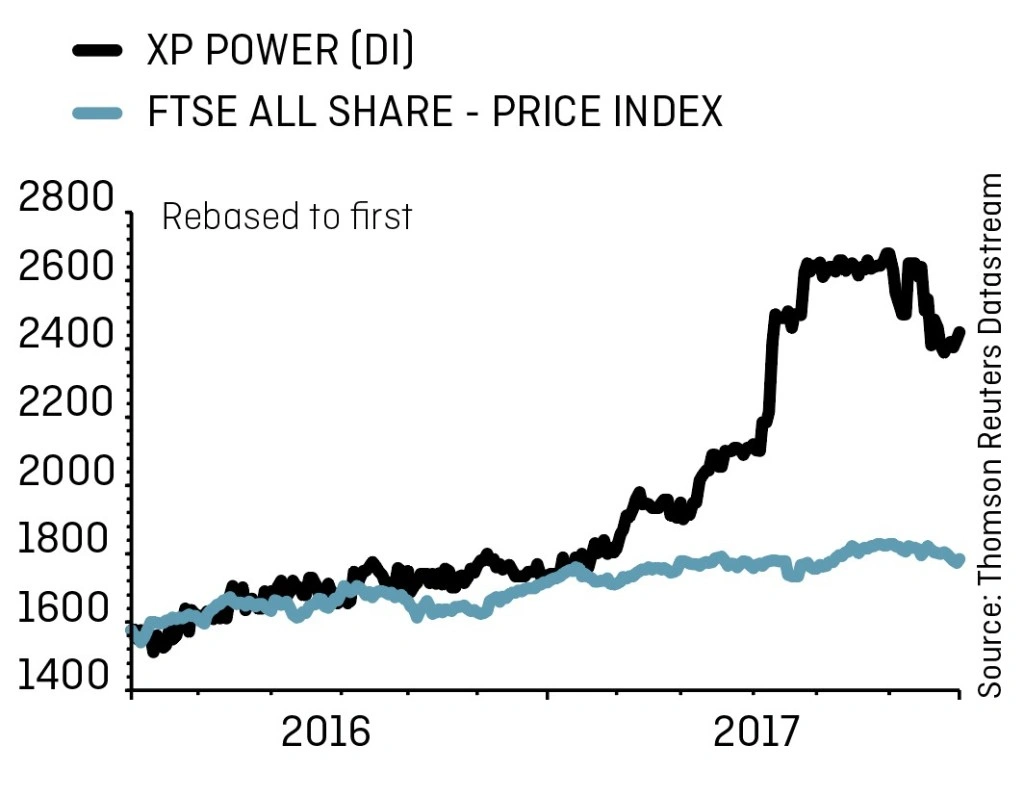

Over that decade, the share price has soared from 411p at the start of 2007 to now trade at £24.11.

WHAT DOES IT DO?

XP has clawed its way up the value chain over the years by developing its own in-house intellectual property (IP). This is complex, science-based kit designed for when off-the-shelf solutions can’t do the job.

Many power systems require custom output voltage combinations, unique control or status signals and specific mechanical packaging for optimal performance and systems integration.

This is where XP’s engineering tries to stand out. The company has a stated aim to have the most comprehensive and up-to-date product range in its target markets, particularly in defence/aerospace, healthcare, rail and a few other custom power niches. XP estimates these add up to a combined £1.5bn target market.

It has developed a stringent five-step sales cycle process designed to leverage its engineering expertise into operating and financial performance.

IMPROVING MARKETS

Pre-tax profit has progress from £20.2m in 2012 to £27.8m in 2016. If this looks a little pedestrian, consider that this has been achieved in a fairly plodding trading environment.

That looks to be changing. There have been accelerating trends in the last quarter of 2016 and first quarter of 2017. In particular, we note that XP said on 11 April that trading so far this year had been strong.

Recent director share sales worth £14.5m may have shaken some investors. However, those directors still own substantial stakes in the business, worth more than £43.5m between them.

Investment bank Investec forecasts mid-single digit growth in pre-tax profit this year to £30.4m and £32.1m in 2018. Yet its analysts admit they are being ‘cautious.’

This implies scope to not just meet, but beat expectations, creating further positive market sentiment around the stock.

XP Power (XPP) £24.11

Stop loss: £19.29

Market cap: £464m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- 21 investment trusts now considered ‘dividend heroes’

- Fire safety expert Marlowe reports surge in interest

- FTSE 100 stocks with superior dividend growth

- AA refinances debt to cut annual charges

- Takeover bid for FTSE 100 stock Worldpay

- Significant development in US sports betting market

- Inmarsat sweats on satellites battle

- Three UK stocks grab place on ‘high quality dividend’ list