Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

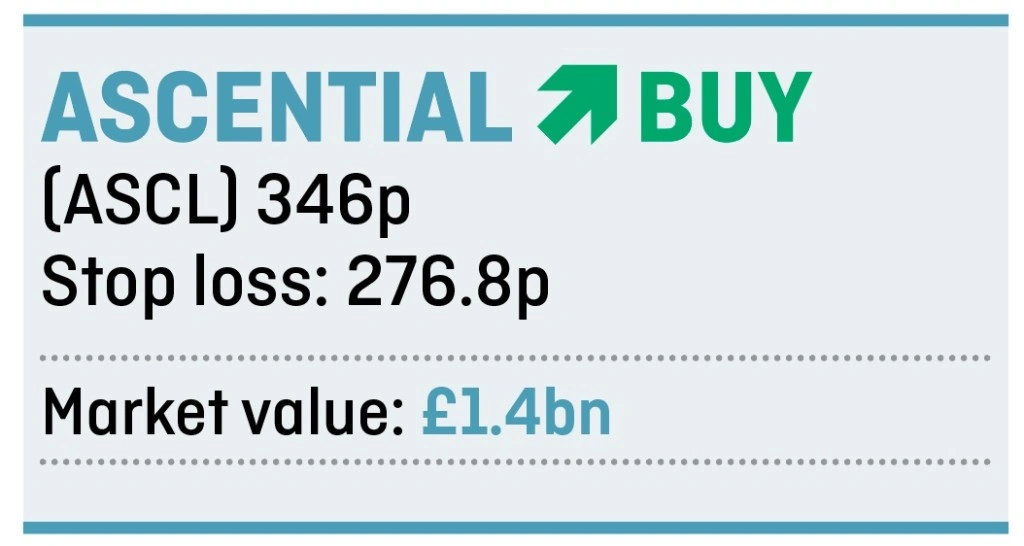

magazineAscential’s China Money boost

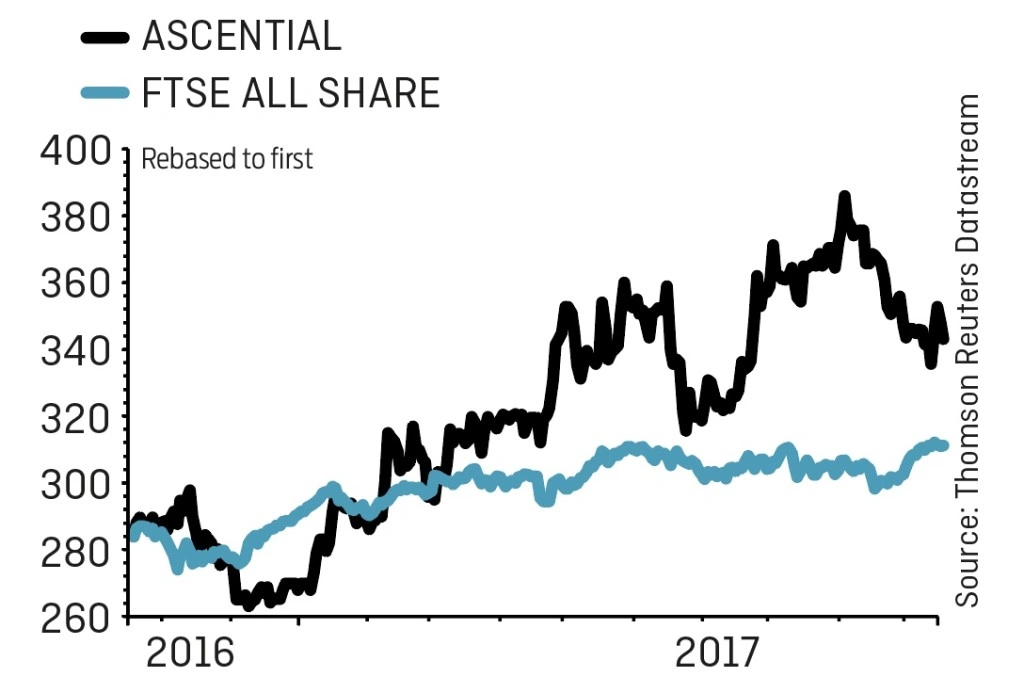

Now is the perfect time to invest in media group Ascential (ASCL) as there are several potential share price catalysts on the horizon. We’re particularly excited about the launch next year of its Money 20/20 event in China which could have a significant boost

to earnings.

Nearer term, the company is set to hold a capital markets day on 14 November where it will provide more detailed information on its business, potentially resulting in more interest from analysts and investors.

Ascential is best known for running the prestigious Cannes Lions advertising festival. It joined the stock market in February 2016, having previously been owned by private equity firm Apax and Guardian Media and operated under the name of Emap.

The business has two divisions: Exhibitions & Festivals which accounted for 60% of its revenue and 70% of earnings in the first half of 2017; and the mainly subscription-based Information Services which made up the remainder.

Why we like events companies

Events businesses tend to be cash generative and enjoy predictable revenues with plenty of recurring business.

Investment bank Berenberg says Ascential differs from its competitors in that it has a smaller, more focused portfolio of brands. It notes the group has disposed of nearly one third of

its brands and integrated two ‘high-growth acquisitions’.

On this basis, it reckons the company can deliver double-digit earnings per share growth out to 2019.

On 12 October the company announced an agreement to launch a new version of its successful financial services-focused Money 20/20 event in China, to be held in November 2018.

Because of inherent differences between markets in this space there is limited risk of cannibalising existing business by launching in

different geographies.

Berenberg estimates that if the Chinese event grew to the level of its Las Vegas iteration it could boost its 2019 earnings estimates by nearly 30%.

Although the new exhibition won’t contribute to the bottom line for some time we expect the market to begin pricing in its potential over the coming 12 months.

Valuation not too demanding

On this basis we don’t see a 2018 price-to-earnings ratio of 17.4, based on Berenberg’s forecasts, as too much of a stretch.

With strong cash generation enabling the company to steadily pay down debt, there is also the scope for further M&A activity which could augment growth prospects.

The free cash flow yield, a metric often used by private equity firms to identify targets which can deliver returns ahead of the cost of borrowing, at 7.3% suggests Ascential could itself be a takeover target. (TS)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.