Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy the UK stock market is currently on the defensive

All of the headlines regarding to the UK stock market may well be dominated, in the short-term at least, by the result of the 11 December vote in parliament on Prime Minister Theresa May’s proposed Brexit deal.

It seems clear from price action in the UK’s stock, bond and currency markets that no-one seems to fancy ‘no deal’ as the outcome of the negotiations with the EU and the upcoming Parliamentary debate.

Whether a deal of some kind or no deal of any kind becomes the outcome is still unclear, as are the implications for the UK’s economy and its financial markets.

Throw in wider concerns over trade and tariffs and a global trend toward tighter monetary policy, in the form of higher interest rates and less quantitative easing (or even its withdrawal), and investors seem to be responding in a tried-and-tested way when it comes to their UK equity exposure – they are taking a defensive posture in a bid to weather any political (or other) storms.

CHANGE IN TONE

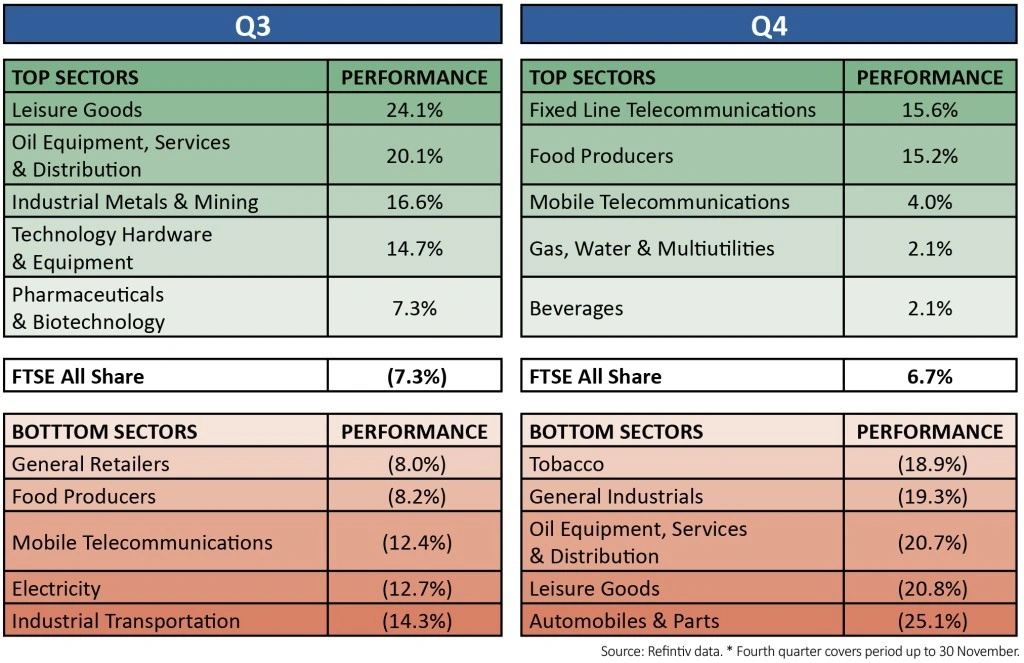

They are doing so in two ways. This can be seen very clearly by looking at which of the 39 industrial groupings have done best – and worst – on a quarterly basis since the start of 2018.

The first is a switch away from cyclical sectors like autos and parts (which also received a boost from Melrose’s (MRO) bid for GKN), industrials, forestry, media and chemicals towards more traditionally stodgy areas such as telecoms, food stocks, utilities and pharmaceuticals.

The second is a switch toward value. Technology hardware has dropped out of the quarterly list of top 10 performers.

Previously downtrodden laggards have stepped up, notably fixed-line telecoms (a sector where many a value manager has been talking up BT’s potential); utilities, which analysts argue look cheap relative to the asset bases; and even the banks, where low multiples of book value hint that a lot of bad news may be in the price (even if some would argue deservedly so).

SHIFT IN STANCE

Whether this apparent dash for safety, either in the form of defensives or stocks where lowly valuations may provide some downside protection, is the result of global fears over US Federal Reserve policy, trade wars or more domestic matters such as Brexit is hard to say.

But the fourth quarter’s stock market action differs quite markedly from what we have seen since the EU referendum on 23 June 2016.

Since then, trading has generally been dominated by weakness in the pound and therefore strength in overseas earners and exporters, and especially those stocks who fit these descriptions and have exposure to the US economy and do little business here at home.

By contrast, sectors with substantial exposure to the UK, such as retailers, construction and the utilities have lagged – with utilities particularly poor thanks to the threat, perceived or real, posed by the prospect of a Labour government under Jeremy Corbyn should the Tory government tear itself to bits.

The possibility of some sort of Brexit deal between the UK and EU means this trade of ‘pound down, exporters up’ has lost some of its lustre – but if the May deal is rejected and her government falls then it would be logical to expect sterling to slip and fund managers to investigate this strategy once more.

The mathematics of MP votes suggest this could well happen. But if the Brexit deal is approved, and ‘no deal’ avoided, perhaps sterling and those long-neglected domestic sectors could return to favour.

Given their underperformance and notable unpopularity that may be where the value lies in a UK market that itself looks cheap relative to its global peers, on just 11.6 times earnings and with a 4.8% dividend yield for 2019.

Why could this be interesting? As if often does, this column will let master investor Warren Buffett have the last word.

‘The most common cause of low prices is pessimism – sometimes pervasive, sometimes specific to a company or industry. We want to do business in such an environment, not because we like pessimism but because we like the prices that it produces. It’s optimism that is the enemy of the rational buyer,’ he said.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.