Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineShare pick for 2019: Euromoney

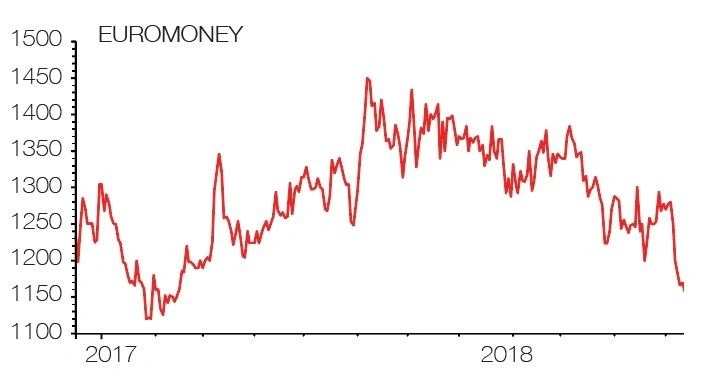

We think the transformation of Euromoney (ERM) from an old-fashioned media business to a higher quality data services outfit will hit home with the market in 2019 and help drive the share price higher.

The company is rapidly growing its pricing and data side, diversifying away from a weaker asset management business made up of Institutional Investor magazine and offshoots as well as the BCA investment research arm.

The pricing, data and intelligence division does smarter things like providing prices for opaque markets using traditional journalism. This might mean finding out what parties are paying for different commodities, for example, and then monetising this highly valuable market intelligence.

With much of the income from this part of the business linked to subscriptions, Euromoney enjoys a good level of earnings visibility.

Even after the company splashed out $87.3m on the acquisition of two US businesses – BoardEx and TheDeal – the company should still be in a net cash position thanks to a series of previous disposals of non-core assets. This includes the Indaba mining industry event.

Prior to the two recent acquisitions, Numis forecast net cash of £135m by the end of 2019, a total which also reflects inherently strong cash generation from operations.

This situation provides headroom for further M&A activity to accelerate its shift to a higher quality business profile and a buffer in case times get significantly tougher.

The shares still trade at a material discount to global financial data peers despite the headway chief executive Andrew Rashbass has made since joining in 2015.

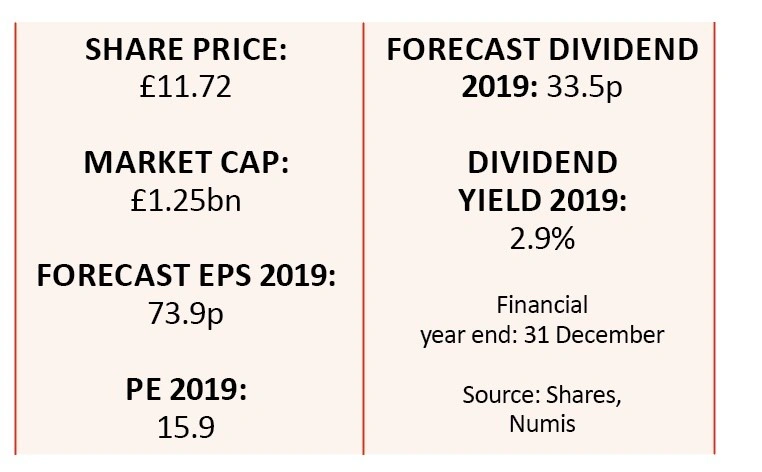

Euromoney trades on a forward PE of less than 16-times compared to a peer group average of 25.6-times, according to research house Edison.

Boardex and TheDeal are expected to be immediately earnings enhancing. Both are data-driven outfits with subscription-based models and therefore a good fit with the current strategy. BoardEx provides executive profiling and relationship mapping, while TheDeal is a database of M&A information.

There are some risks for investors to weigh. The asset management arm, which still accounted for nearly 40% of revenue in the past financial year, is struggling thanks to industry cost-cutting, which was exacerbated by the disruptive Mifid II regulations on financial sector transparency.

We accept Brexit could result in further pain. Additionally Daily Mail & General Trust (DMGT) continues to hold a 49% stake in the business and if it were to look to offload its holding this could depress the share price.

However, we still believe the shares are incredibly attractive given the tighter business focus and relatively cheap valuation.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

Editor's View

Feature

Great Ideas

- Share pick for 2019: Hollywood Bowl

- Share pick for 2019: Rolls-Royce

- Share pick for 2019: GB Group

- Share pick for 2019: Euromoney

- Share pick for 2019: Next

- Share pick for 2019: Renishaw

- Share pick for 2019: Fevertree Drinks

- Share pick for 2019: Keystone Law

- Share pick for 2019: On The Beach

- Share pick for 2019: Coats