Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

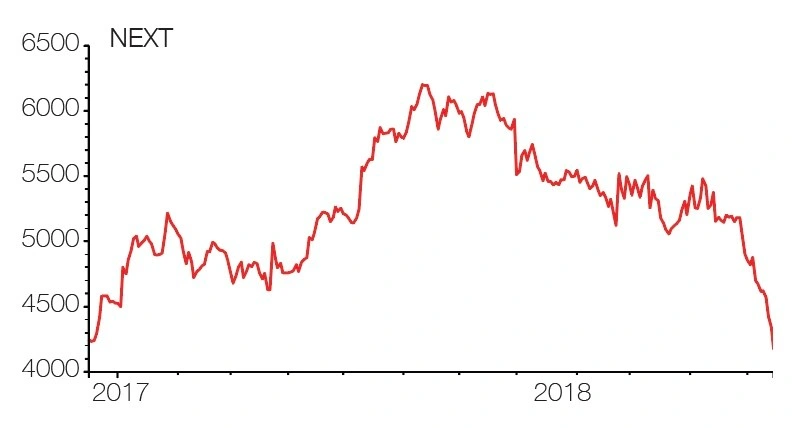

magazineShare pick for 2019: Next

We recognise retail is completely out of favour with investors and so are UK-domestic stocks. However, it feels the right time to take a contrarian view and look for opportunities in both these categories.

We’ve picked Next in the belief that management can navigate the tricky backdrop and that we may also see a bounce in UK-focused businesses, assuming there is an agreed Brexit plan which brings more certainty to the market.

Led by respected shopkeeper Simon Wolfson, Next’s thriving online operation is widely overlooked. Besides a pristine balance sheet, Next is highly cash generative and should be able to withstand flagging footfall while maintaining profitability.

Next is so much more than a bricks and mortar fashion retailer. Online market share gains, boosted by a growing online overseas operation and the third-party brands business, LABEL, should continue to outweigh the drag from lower shop sales.

Despite falling like-for-like sales, the vast majority of Next’s stores remain very profitable. It also has many stores on short leases. When they come up for renewal, it can shut the worst ones and those being renewed are being done on much lower rents.

It is making more use of in-store stock to fulfil online orders rather than solely depending on warehouse inventory. And there will be a trial using stores as a collection point for third party, non-competing businesses.

While third quarter store sales fell 8%, online sales grew by 12.7% and Next maintained sales and profit guidance for the financial year to 31 January 2019.

With spending migrating to the web, Next is heading in the right direction with more than half of sales now coming from its online and finance businesses.

Invesco fund manager Mark Barnett also argues that having a large physical store estate is no bad thing. He says: ‘Next is combining the best of offline with online. A large number of orders are click and collect ones via stores, so Next needs a high street presence. These stores may not look the same in the future as they do today.’

Broker Liberum forecasts adjusted pre-tax profit will hit £727.3m for the year to January 2019 and then rise to £743.3m in 2020 and £773.4m in 2021.

The shares trade on a mere 9.2 times forecast earnings for the financial year to 31 January 2020. Next is one of the best-run companies on the stock market and that equity rating is an absolute bargain for a business of its calibre. You’re also being paid an attractive stream of dividends, currently yielding a prospective 4.1%.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Aequitas

Big News

Editor's View

Feature

Great Ideas

- Share pick for 2019: Hollywood Bowl

- Share pick for 2019: Rolls-Royce

- Share pick for 2019: GB Group

- Share pick for 2019: Euromoney

- Share pick for 2019: Next

- Share pick for 2019: Renishaw

- Share pick for 2019: Fevertree Drinks

- Share pick for 2019: Keystone Law

- Share pick for 2019: On The Beach

- Share pick for 2019: Coats