Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineVodafone’s persistent high dividend yield is telling us something bad

Can Vodafone continue to pay generous dividends? That’s the big question continuously asked by investors.

Its shares at 141.48p are currently yielding 9.1%, significantly higher than the 4.9% average for the FTSE 100 index.

Vodafone’s full year results to be published on 14 May are expected to show that dividends for the 12 month period add up to €0.1507. That payout works out at about 12.9p per share.

Many market watchers believe this level of dividend remains unsustainable and that a cut to its future income commitments is inevitable.

Vodafone is widely held by investors specifically as an income stock so any reduction in cash payments from the shares would go down terribly.

Capital expenditure, free cash flow and the credit rating of its £32.1bn of net debt hold the keys to answering the dividend sustainability question.

It needs to reduce such huge borrowings, as well as fight off growing competition and potentially invest a lot of money in new radio wave spectrum for fifth generation (5G) mobile networks that will allow users to send more data faster over the mobile internet.

New chief executive Nick Read recently met a group of institutional investors in a bid to calm such concerns, taking the opportunity to reiterate the group’s commitment to its current dividend pledge.

At that meeting Read is believed to have spelled out Vodafone’s largely unchanged strategy and explained the group’s capital expenditure and free cash flow ambitions.

These partly revolve around layering new 5G infrastructure over existing 4G networks, and extracting significant cost savings from its acquisition of assets from Liberty Global across Germany and Central Europe.

Vodafone’s balance sheet was recently bolstered by the issue of convertible bonds that raised €4bn from investors. It plans to maintain a share buyback programme in the future to cap potential dilution of equity investors.

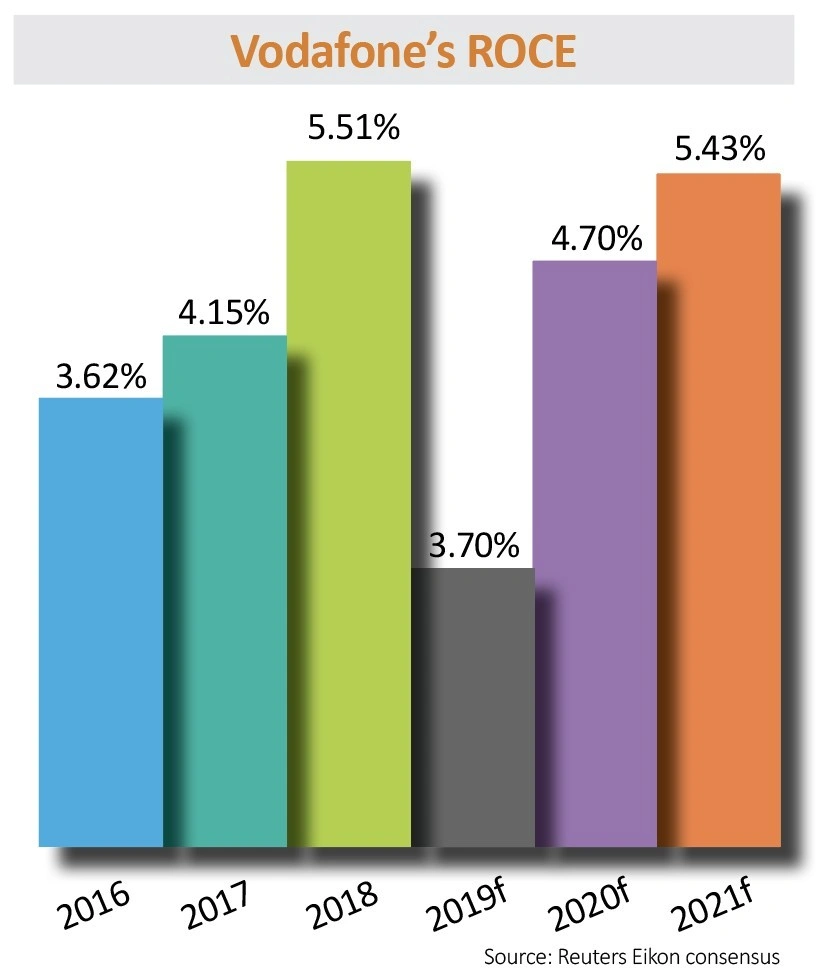

It has made return-on-capital-employed (ROCE) a key focus going forward as it tries to keep investors on side. This is a ratio which measures how effectively a company uses capital.

Vodafone’s ROCE is forecast by analysts to show a steep decline this year before improving from 2020.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.