Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

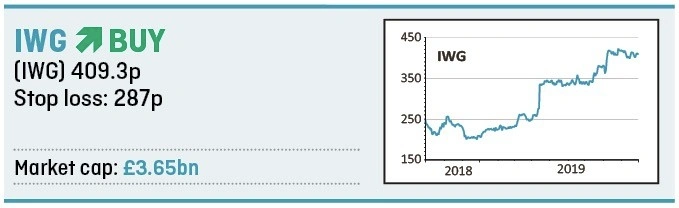

magazineIWG could be the next big market cash machine

Serviced office group IWG (IWG) is undergoing a significant transformation that could result in enhanced returns to shareholders in the coming years.

IWG is moving to an asset-light strategy where it becomes a master franchise owner, similar to the model used by Domino’s Pizza (DOM) and McDonald’s. IWG is selling its operating businesses to partners in exchange for cash and future licensing and services revenue.

Franchising ultimately provides a cost-effective way for IWG to take advantage of the structural growth of the flexible, co-working market.

A £320m deal was struck earlier this year in Japan where Tokyo-listed TKP will operate 130 flexible working centres using IWG’s brands Regus, Spaces and OpenOffice. The pair has since struck similar deal for IWG’s Taiwanese operations for £22.7m.

Chief executive Mark Dixon said at IWG’s half year results in August that discussions were being held with other prospective partners, with an update expected to be given to the market later this year.

Three private equity firms tried to buy IWG last year but talks ended on a disagreement about valuation. Fund manager Mark Slater who holds the stock in Slater Growth Fund (B7T0G90) says this bid interest made Dixon ‘more engaged’. He adds: ‘IWG’s chief executive realised the business could be run a lot better. Having a franchise model could see huge amounts of capital returned to shareholders.’

Some investors may be put off by IWG’s valuation. It is trading on 31.4 times forecast earnings for the next 12 months and five times book value.

Numis analyst Steve Woolf believes the current valuation does not fully reflect the potential for incremental growth, lower risk and higher cash generation as the franchise model becomes more established.

‘While the next catalyst could lie with the announcement of a new franchise buy-in, our sum-of-the-parts indicate fair value of 515p per share,’ he adds.

IWG has delivered 11% compound annual growth in dividends since 2010. ‘If IWG adopted a fully franchised model, we believe there would be significant scope for additional capital returns to investors,’ says Woolf.

‘If a sale price of around two times market value-to-sales was achieved, this would represent a cash inflow of c.£5.3bn, increasing to £6.6bn for a multiple of 2.5-times.

‘Including the proceeds from Japan, and adjusting for revised net debt and repayment of customer deposits, this would leave IWG with a net cash position of c.£4.5bn to £6.6bn. This equates to 490p to 640p per share, and provides significant scope for share buybacks during the franchising process.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.