Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

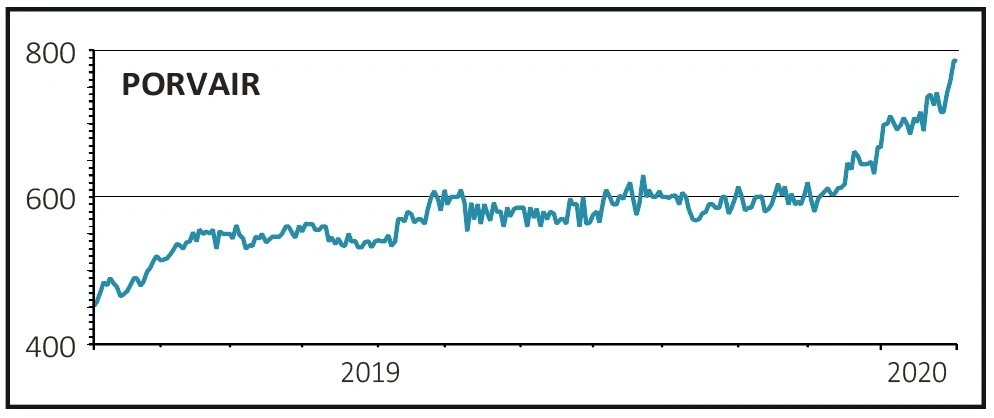

magazineBank the 20% profit on Porvair shares

Porvair (PRV:AIM) 760p

Gain to date: 20.6%

Original entry point: Buy at 630p, 26 September 2019

Specialist, high end filters manufacturer Porvair (PRV:AIM) reported record revenues on 3 February of £144.9m, up 13% for year ended 30 November 2019, while adjusted pre-tax profit was 9% higher to £14.8m, both slightly higher than consensus estimates compiled by Refinitiv.

The strategy is to focus on specialist, bespoke design of products whose replacement is mandated by regulation or quality accreditation and which ideally have a long life cycle.

Around 80% of revenues are recurring, driven by heavily regulated markets, which give the business some defensive qualities in a tough

macro environment.

That said some divisions aren’t immune to the cross-currents of world trade tensions, as evidenced by the 6% revenue contraction in the Metal Melt Quality division which designs and manufactures porous ceramic filters for the filtration of molten metals.

Shares highlighted the premium rating of 23.9 times forecast earnings at the outset, arguing that it was justified by good earnings visibility, defensive characteristics and attractive growth prospects.

Today the rating has crept up to around 30 times 2020 forecast earnings. Broker Shore Capital says this is in line with Japanese peer Yamashin Filter and a circa 20% discount to US peer Pall.

SHARES SAYS: While this is a fantastic business, the higher rating adds extra risk which is harder to justify. We’re minded to take profits while the going is good.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Education

Exchange-Traded Funds

Feature

Great Ideas

Great Ideas Update

Money Matters

News

- China trusts under pressure from coronavirus fears

- Sales growth challenges weigh on Diageo and Unilever shares

- The key challenges facing new BP boss

- Surging stock prices mask concerns about a US economic slowdown

- The companies in the race to find a coronavirus cure

- Burford Capital shares gain despite earnings warnings