Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat your weekly shop can tell you about Unilever and Reckitt

When you go to the supermarket or go online to shop for household essentials, just how much do brands matter to you?

Will you pay more for a brand you know and have an attachment to, or are you prepared to pay less for a cheaper non-branded alternative? And if you’re happy to pay up, perhaps you’ll be looking for a more niche, artisan product.

These everyday questions of domestic life are central to the dilemma facing two of the UK’s largest listed companies – consumer goods giants Reckitt Benckiser (RB.) and Unilever (ULVR).

Historically both companies were popular with investors due to their reliable dividends, the robust margins protected by a strong portfolio of brands, and steady growth. Of late that growth has started to evaporate leading to strategy shake-ups and management change at both firms.

We took a detailed look at Unilever in a recent issue after it warned on sales growth in December 2019. Now Morgan Stanley analysts have been running the rule over Reckitt Benckiser ahead of its full year results on 27 February when a relatively new-look management team, including ex-Pepsi man Laxman Narasimhan at CEO, will outline their plans for the business.

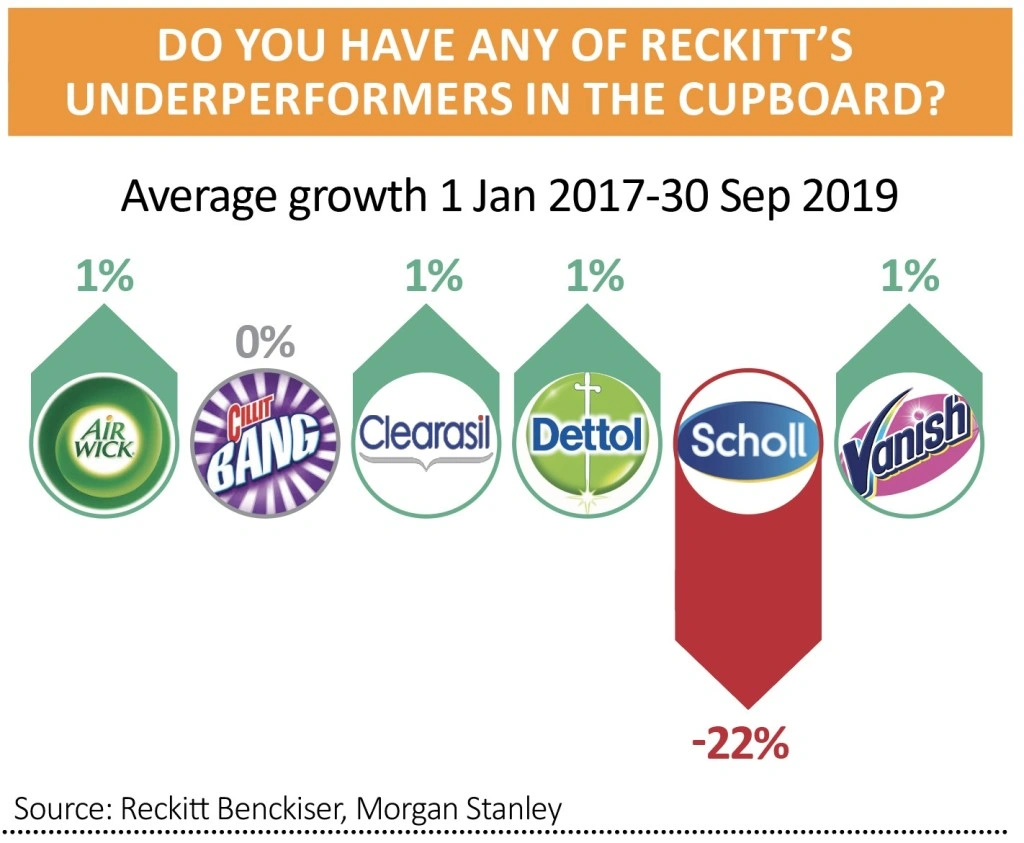

The investment bank observes that in 13 of the last 14 quarters the company has fallen short of expectations. Its analysis further suggests that just two out of its top 23 brands (which combined account for 83% of sales) delivered high single digit growth in the period between 2017 and 2019.

These standout names are toilet cleaner Harpic (likely familiar to UK shoppers) and surface cleaner Veja (likely not as it is sold in Brazil).

Improving the growth prospects of the underperformers in the portfolio, which include the Cillit Bang range and antibacterial brand Dettol, appears as if it would involve sacrificing profitability.

Morgan Stanley says: ‘If we assume for illustration that the investment level in the underperforming brands is raised to 20% to drive growth back to in-line or above market growth, this could drive an additional 150 to 200 basis points to group top-line growth. Our framework suggests that this could cost 80 to 240 basis points at the group margin level.’

With both Unilever and Reckitt, you need to think whether investing in the underperformers in their portfolios can make a difference or if we just aren’t as loyal to those brands specifically or more significantly to big brands in general any more.

Given their substantial weighting in the FTSE 100 and the big contribution they make to the overall dividends on offer from UK stocks, these considerations are relevant to most investors. It’s something to consider next time you do the weekly shop.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.