Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy do shares sometimes react so differently to positive news updates?

It’s fair to say that more often than not as human beings we overreact to information, which in turn can lead share prices to overreact in the short term.

Yet, as our recent article on momentum showed, if a stock is in a clear trend – positive or negative – it can experience a lot of short-term volatility but remain in that trend for some time, often longer than most investors anticipate.

If markets were genuinely efficient, share prices would incorporate all available news, good and bad, at all times. The only thing which should prompt a share price to go up or down would be new news of a company-specific nature, not news about the market in general.

GROUND RULES

However, the market has a tendency on the one hand to get over-excited about the future, continually bidding stocks up and on the other hand to take a bleak outlook and send share prices lower.

In other words, whenever a company releases news – good or bad – context matters greatly. Delivering good news when markets are in panic mode is unlikely to stop a company’s share price from falling.

Then there is the matter of degree. Good news can actually be bad news if it fails to meet the weight of investors’ expectations. Delivering a 25% increase in earnings would normally be enough to see a company’s share price jump, but if investors are primed for a 50% earnings increase it’s quite possible the shares will fall instead.

If you see shares fall on what at face value appears to be good news, it can be a sign that market expectations are too high. If that’s the case, investors may have got ahead of themselves and the shares could be vulnerable to further selling as expectations are reset.

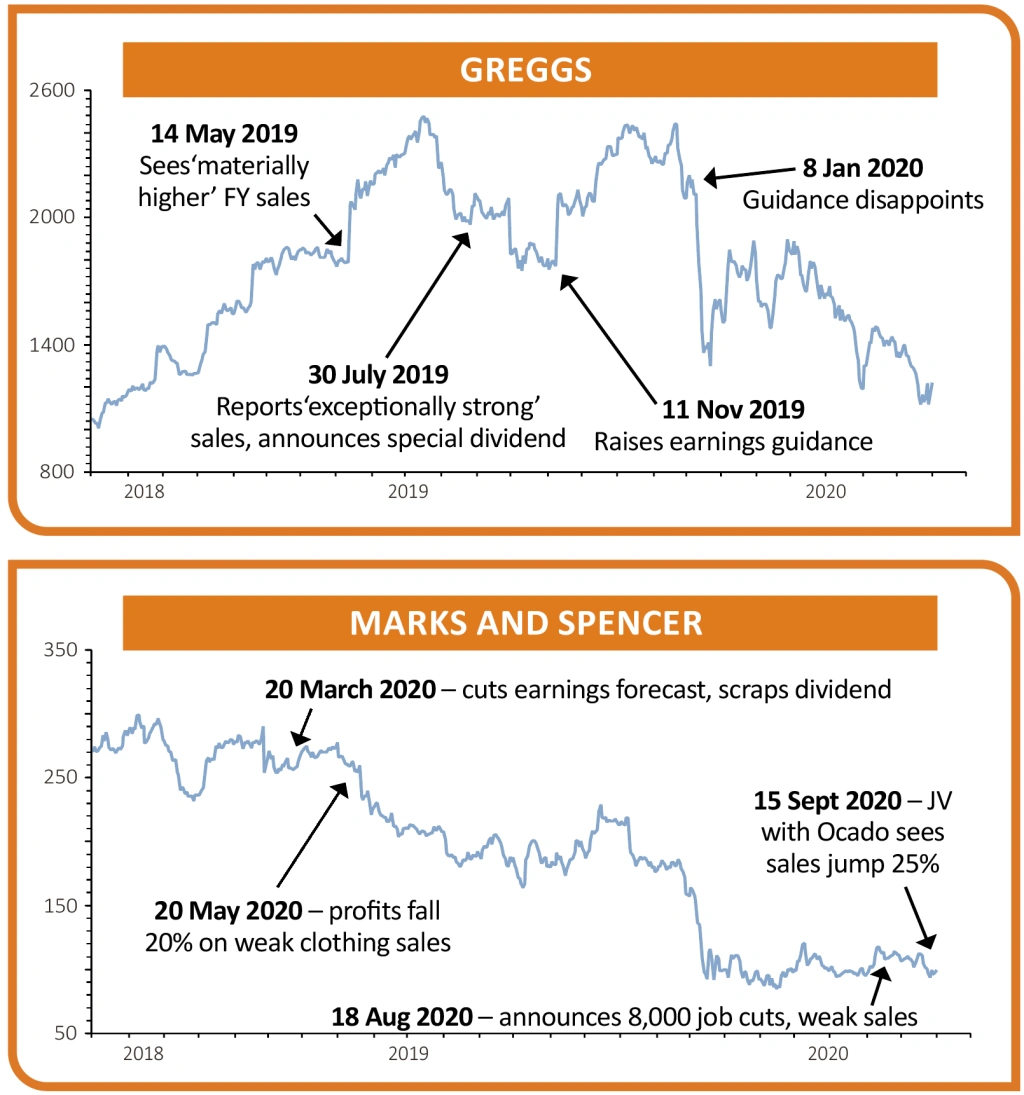

This is arguably what happened to food-to-go retailer Greggs (GRG) in January when it said full-year 2019 earnings would be ‘slightly higher’ than management had previously forecast, sending its shares down rather than up.

After a diet of constant positive earnings surprises, investors were expecting fireworks but instead the news was a damp squib. The arrival of the coronavirus has since led to a drastic rebasing of growth expectations.

MANAGING EXPECTATIONS

This is why companies spend so much time managing expectations, through trading updates, analyst and media briefings and presentations to investors. No finance director wants to see his company’s shares hammered due to poor communication, so there is a tendency for companies to set achievable earnings targets in order to be able to deliver a small ‘beat’ each quarter.

It should be said that, if results are going to be way above forecasts – or for that matter way below them – companies have a duty to pre-announce this news to the stock exchange so as not to withhold market-sensitive information.

The issue with managing expectations, however, especially if part of the directors’ pay is based on share price performance, is companies can find themselves having to improvise and discover new ways of beating consensus forecasts.

We aren’t talking fraud on the scale of firms like Wirecard, but investors should be on their guard for companies using unusual accounting techniques or making deals to give the appearance that their businesses are hitting their targets when in fact they aren’t.

REPEAT OFFENDERS

A third factor to take into account when a company reports is sentiment. If a firm has consistently disappointed investors and analysts have had to repeatedly lower their forecasts, the chances are that one piece of good news won’t be enough to change the market’s view.

Royal Mail’s (RMG) double-digit intraday rally on a positive revenue surprise (11 Sep) demonstrated that a bombed-out stock can bounce in the short-term.

It’s well known that we experience pain a lot more intensely than we experience pleasure, and it’s the same with investing. If we lose money in a stock, we are unlikely to look at it again with the same enthusiasm – once bitten, twice shy, as the saying goes.

Therefore it can take a lot of good news before an under-performing company truly turns the corner and investors begin to trust it again. A good example might be retailer Marks & Spencer (MKS), which had loyal fans up to 2015 when its shares traded close to 600p, but which has disappointed in terms of sales ever since and lagged the FTSE 100 to such an extent it was finally ejected from the index in June.

Recent news flow has actually been quite positive, especially in terms of sales of its food and household products on the new online retail platform jointly-owned with Ocado (OCDO), but the shares are still trading below 100p and we get the sense that after years of being let down many investors have given up hope of a revival.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Novacyt still looks really cheap despite share price rally

- Panoply busy signing new contracts and buying businesses

- Premier Foods poised for Hovis windfall

- Don’t miss out on this high-quality European growth company

- Take profits on gold miner Centamin

- Shares in AG Barr start to pick up after reassuring results

Investment Trusts

Money Matters

News

- How Trump’s Covid-19 diagnosis has impacted stock markets

- The options for Rolls-Royce shareholders as £2 billion rights issue looms

- What Asda’s sale means for supermarket rivals

- Cineworld faces liquidity crunch as cinemas close again

- Housebuilders rally on Boris Johnson’s bid to help first-time buyers