Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazinePanoply seeds growth opportunity with biggest ever acquisition

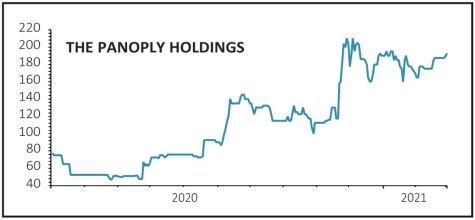

THE PANOPLY HOLDINGS (TPX:AIM) 189p

Gain to date: 110%

Original entry point: Buy at 90p, 6 August 2020

Digital transition business The Panoply Holdings (TPX:AIM) has made its biggest acquisition so far with the £26 million cash and shares purchase of Keep It Simple (KITS).

The managed services supplier to public sector organisations will do three things for Panoply. First, it adds digital transformation engineering expertise in the ‘go-live’ end of IT projects, allowing Panoply to bid for much bigger contracts, up to £20 million in time.

Second, it brings a £30 million backlog of annuity income with departments such as the rural Payments Agency (which pays government subsidies to UK farmers) and DEFRA, and one-third boost to earnings at a stroke, according to Panoply chief executive Neal Gandhi.

Lastly, using its highly rated paper to part fund the deal (£18.5 million) will widen the share register and improve the liquidity of the stock (i.e. how easy it is to buy and sell).

This looks like a great deal for the company and its investors as central and local government (and the private sector) continue their nascent digital push. Stifel raised its March 2022 earnings per share (EPS) forecast from 6p to 7.7p, implying a price to earnings multiple of 24.5.

SHARES SAYS: Still a buy.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

First-time Investor

Great Ideas

- Buy Dotdigital, among the UK’s few, true software growth businesses

- Panoply seeds growth opportunity with biggest ever acquisition

- Buy Lindsell Train UK Equity for strong short and long-term returns

- Supermarket Income REIT appeals as a steady investment purely for dividends

- Eurofins beats forecasts and raises guidance again