Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineGrowth, profit and M&A to drive CentralNic higher

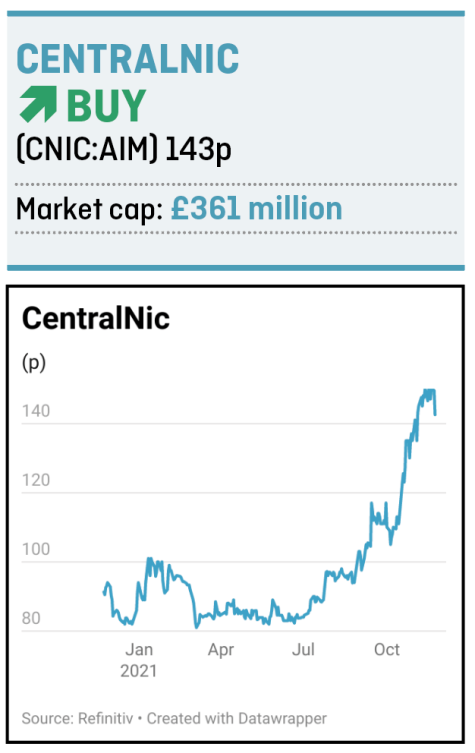

Small cap internet expert CentralNic (CNIC:AIM) has a gold standard buy and build strategy and enjoys strong levels of organic growth. It also has high levels of recurring revenues that frequently throw off more cash that adjusted earnings before interest, tax, depreciation and amortisation.

Despite these attractions, investors can still buy the stock on what one analyst has called a ‘pedestrian valuation’. The current year has seen net debt cut by $6.4 million despite spending $15 million on acquisitions and earnouts of past deals, leaving the business on an enterprise value of £302 million.

That equates to a 2021 EV/EBITDA multiple of around 11 versus analyst estimates for operational peers of more than 18 times. The price to earnings multiple for 2022 stands at 17.4.

CentralNic provides the tools businesses need to thrive online, offering website registry services, distribution, and strategic consultancy for various types of internet domain names from a single platform.

This is a game of scale, the bigger an operator is and the wider its reach, the more powerful its model and the better the profit growth. That helps explain 14 acquisitions since the company joined the London market in 2013, including KeyDrive in July 2018 for £33.6 million, Team Internet in December 2019 for £36.1 million and £28 million spent on Polish internet services businesses Zeropark and Voluum in September 2020. Funding is provided through a mix of equity raisings, bank debt and bonds.

So far in 2021, it has acquired German company Wando Internet Solutions, bolstering its online marketing arm by adding social marketing, display advertising and search engine marketing.

This is an important shift because online marketing is faster growing and offers higher profitability. In the nine months to 30 September 2021 CentralNic’s online marketing operations saw revenues up 129% to $94.1 million with organic growth of 47%, helping the overall business to post its largest organic growth ever of 29%.

Around $10 million has been invested in new staff and systems to drive operational efficiencies.

The internet services industry is dominated by US players such as GoDaddy and Verisign, but it is also hugely fragmented, which leaves an abundance of potential future acquisitions for CentralNic to hoover up.

Forecasts for 2022 of 10% growth imply earnings per share of $0.11. Estimates should be bolstered by opportunistic acquisitions as they emerge. Improving operational leverage will also help CentralNic towards its ambitions for a place at the top table of internet service companies.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

- DotDigital share slump means you can buy cheaper now

- Growth, profit and M&A to drive CentralNic higher

- Plenty of reasons to remain positive on Euromoney

- The smart way to play a rebound in the Chinese stock market

- All-weather trust Ruffer is selling new shares at a discount

- Investors overreact to Frontier Developments' downgrade