Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

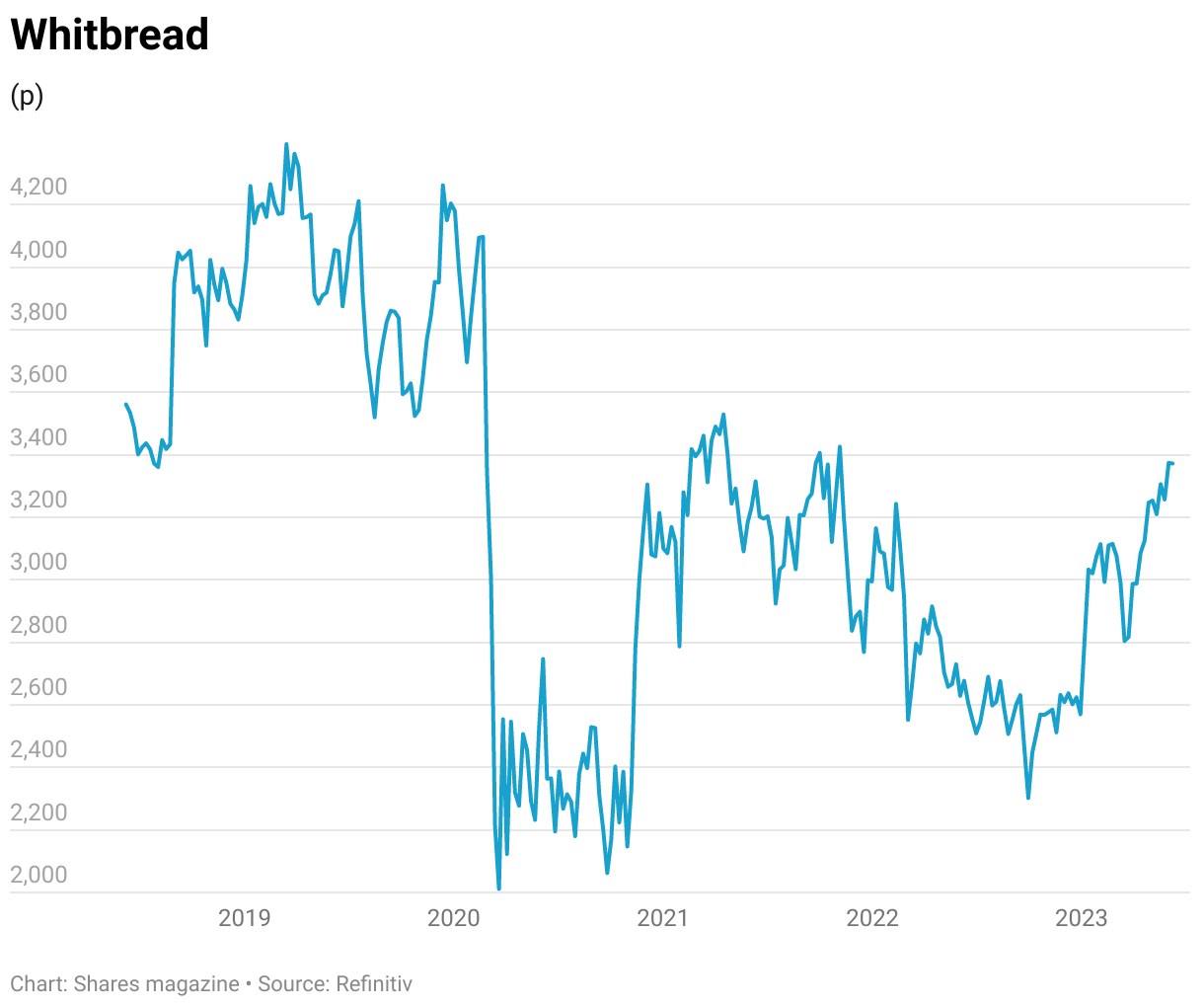

magazineThe time looks right to book into hotel operator Whitbread again

While shares in Holiday Inn operator Intercontinental Hotels (IHG) are flying high, those in budget hotel operator Whitbread (WTB) have been languishing, but we can see three reasons why that trend could reverse.

Revenues, earnings and dividends are already well above their pre-pandemic levels, and hotel stays are on the increase again – not just for pleasure but for business customers too.

The firm is looking to sell off some low-yielding assets in order to grow its hotel estate. Furthermore, the mooted price tag for rival Travelodge suggests considerable upside potential for the valuation of Whitbread’s Premier Inn chain.

A recent study by US investment bank Morgan Stanley found travel budgets at global firms with an aggregate annual spend of $5 billion were ‘surprisingly robust’ with spending expected to rise by high single digits both this year and next year against industry forecasts of low single-digit growth in RevPAR (revenue per available room).

While virtual meetings may be here to stay, suppliers still want to meet their customers and vice versa, but they are happy to trade down from upper-tier hotels to cut costs, meaning midscale/economy brands like Premier Inn should outperform the wider market.

Meanwhile, press reports suggest Whitbread has put the ‘for sale’ sign up over part of its UK pub and restaurant arm, which includes well-known brands like Beefeater and Brewers Fayre.

In its results for the year to March, Whitbread flagged the ‘increasing divergence of performance’ between the hotel business and the food and beverage business after UK accommodation revenues posted a 37% increase over pre-pandemic levels while food and beverage sales were 4% lower due to fewer customers.

Whitbread’s food sites are usually freehold properties located next door to Premier Inn hotels, offering guests the option of including breakfast, lunch and evening meals with their stay.

Separating, or at least reducing the weighting of the hospitality operations in the group accounts, could lead to a rerating of the shares.

Lastly, US hedge fund Goldentree is looking to cash in on the resurgence in UK travel by putting its Travelodge hotel chain up for sale for a reported £1.2 billion plus around £400 million in debt.

Shore Capital analyst Greg Johnson argues Premier Inn is bigger, generates more revenue per room, is more profitable and has better asset backing, meaning the UK estate could be worth £8 billion, while valuing the German operations at an investment cost of £1 billion means Whitbread’s shares could be worth up to £43 in total against just over £33 currently.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Exchange-Traded Funds

Great Ideas

News

- What El Niño means for commodity markets and how to play strong crop prices

- Gym Group faces macroeconomic headwinds and consumer behaviour shift

- UK banks’ profit margins under threat as pressure grows to boost rates on savings accounts

- Biotech companies in demand as pharmaceutical companies spend billions on takeovers