Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhat investors should expect from the US in 2024

The US stock market represents almost two-thirds of total world stock market capitalisation, so it seems fair to assume that where America goes the world will follow, at least to some degree. Keeping an eye on the US political scene, US Federal Reserve policy and the American economy may therefore help investors judge what 2024 (and beyond) may hold for their portfolios.

By the same token, four sectors – technology, financials, healthcare and consumer discretionary – make up two thirds of the market value of the headline S&P 500 US equity index. Any investor who wants to cut down on the amount of research they wish to do can at least focus on those, in the knowledge they are looking at some of the most important companies and industries in the world, at least from the perspective of investment.

Centre stage

For better or worse, the US Federal Reserve will remain centre stage in 2024. Some will view this as a good thing, given the central bank’s political independence, willingness to explain its thought processes to market participants and how easy it is to follow its eight scheduled meetings a year (and then read the subsequently published minutes). Others will cringe, not least because the Fed has yet to correctly call a recession in its 111-year history, during which period the dollar has lost 97% of its purchasing power, a trend not helped by experiments such as quantitative easing and zero interest rate policies (ZIRP) since the Great Financial Crisis.

Markets’ faith in a cooling in inflation, a soft economic landing and a pivot to interest rate cuts from the Fed underpinned the late-2023 rally in stock (and bond) markets but this has left the US central bank in a position whereby it needs to deliver or share prices may falter.

At the time of writing, the CME Fedwatch suggests that markets are pricing in six, one-quarter point rate cuts by year end, although last week’s (3 Jan) minutes from the December meeting saw the probability of the first cut coming at the 20 March meeting cut to 66% from 73%. Perhaps the first doubts are creeping in, even if the Fed has done much more to stoke rate-cut expectations than either the Bank of England or the European Central Bank.

Big Four

The near-one third weighting of the S&P 500 toward technology leaves this column feeling a little uncomfortable, although it does help to explain why the index, at around 20 times earnings for 2024, trades above its long-term average of 18 times, according to research from S&P. Even more intriguing is that the Magnificent Seven of Alphabet (GOOG:NASDAQ), Amazon (AMZN:NASDAQ), Apple (AAPL:NASDAQ), Meta (META:NASDAQ), Microsoft (MSFT:NASDAQ), Nvidia (NVDA;NASDAQ) and Tesla (TLSA:NASDAQ) (not all of which are classified as tech stocks) represent 30% of the S&P 500. Such a reliance on so few names is not always a healthy thing and if anything goes wrong with them then other stocks and sectors will need to take up the slack – financials, healthcare and consumer discretionary in this case.

Two of those would presumably falter in the event of a nasty recession, even if lower interest rates could conceivably help the consumer-facing firms and the banks (which could also do with a steeper yield curve).

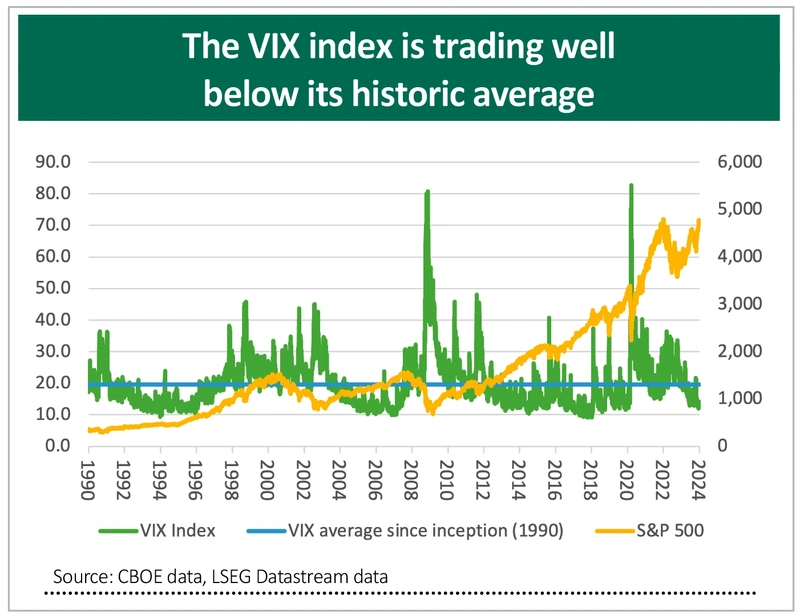

It bears repetition that markets are currently pricing in lower inflation, a soft landing (or even no landing at all) and rate cuts for 2024. Any developments that diverge from that – in the form of a hard landing or an inflationary, crack-up boom if central banks move too precipitately - might not mean the bull run in US equities ends, but they would surely portend greater share price volatility. The VIX – or fear – index is lurking at barely 13, well below its historic average of near 20, to suggest markets are at best complacent, at worst exuberant.

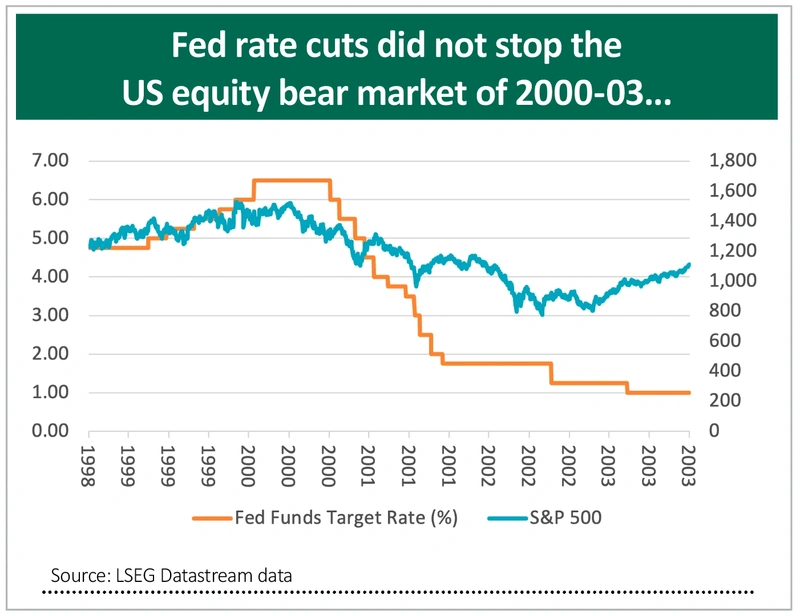

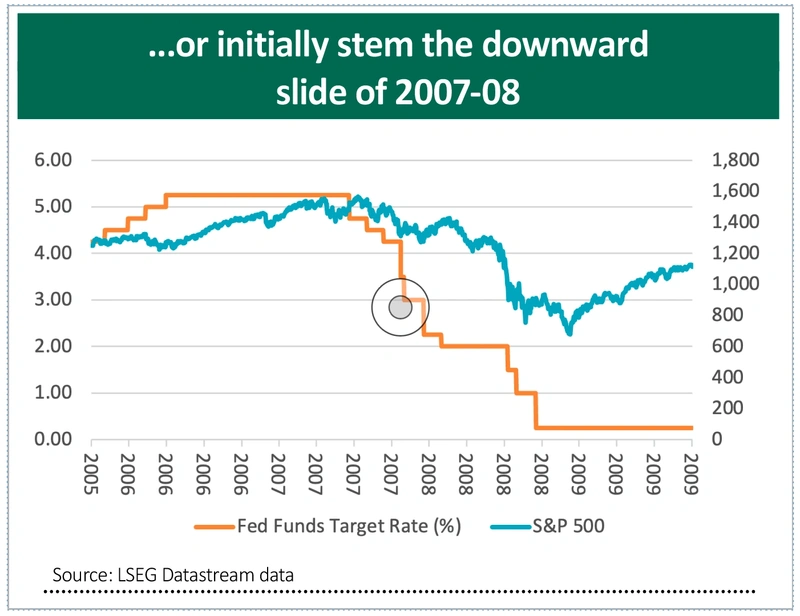

This, again, takes us back to interest rates and the Fed. A crack-up boom and rates may not come down as fast and as far as hoped. A sharper-than-expected slowdown may mean the rate cuts arrive but for the ‘wrong’ reason and investors with long memories will know that Fed intervention did nothing to stop the bear markets of 2000-03 or 2007-09, at least initially. That was because earnings estimates were falling a lot faster than rates, as the US economy hit the buffers.

The dream middle path of cooler inflation, a soft landing and rate cuts may well transpire and in that case then all may be well and good. But if the Fed cuts interest rates because America’s government debts and the interest burden are too high or the economy (and earnings) are hitting the buffers, then markets may need to be careful about what they are wishing for.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Editor's View

Feature

Great Ideas

News

- Next raises guidance after strong Christmas sales

- US March rate cut bets pared back after stronger than expected December jobs report

- What it might take to revive the UK IPO market as M&A frenzy continues

- What completion of game-changing YouGov GfK deal means for the business

- JD Sports Fashion shares take a bath as consumers feel the cost-of-living squeeze