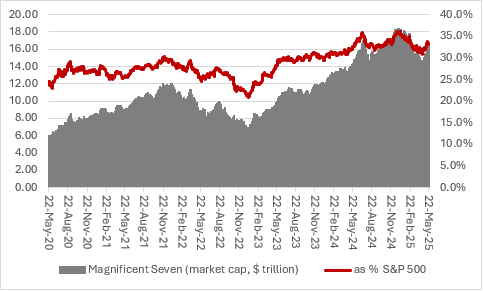

Global stock markets have rallied hard and one major source of support has been the so-called Magnificent Seven of Alphabet, Amazon, Apple, Meta, Microsoft, Tesla and NVIDIA, whose collective stock market capitalisation of $16.6 trillion is 10% below the peak reached on Christmas Eve last year and more than a quarter above the low reached on 8 April.

The stage is therefore set for Wednesday 28 May’s first-quarter results from NVIDIA, which is currently the second-largest company by stock market capitalisation in the world, behind only Microsoft.

Source: LSEG Refinitiv data

This is the next test of whether the Magnificent Seven can push on to new highs, but investors continue to ponder the implications of January’s launch of the R1 Large Language Model by China’s DeepSeek.

How are AI companies faring?

Trump’s tariffs and trade policies are blotting out many other issues right now, but this one is yet to go away. The product challenged the consensus view that Artificial Intelligence required more – more chipsets, more computing and server power and more energy – and AI-related stocks have yet to fully recover their poise.

Super Micro Computer has dished out a profit warning, and even written down the value of some inventory, while CoreWeave disappointed with guidance for its next quarter when it released its maiden quarterly results earlier this month.

NVIDIA’s quarterly result expectations

NVIDIA did offer fairly cautious guidance for the first quarter, which runs from February to April, but it has had the happy knack of beating estimates for the quarter, even if some are tempted to accuse chief executive Jensen Huang of intentionally sandbagging the numbers, so he can deliver the expected, even required, upside surprise.

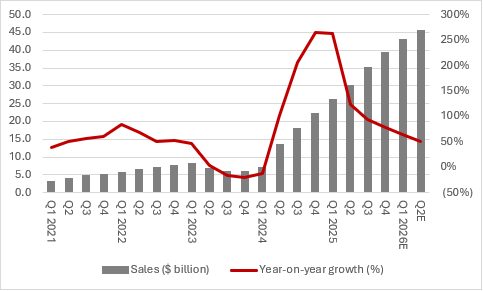

Either way, the first-quarter number will be benchmarked against the guidance given by Mr Huang alongside the full-year results back in February. Just as important will be any guidance for the second quarter, which runs from May through to July.

For the first quarter, NVIDIA has sales to $43 billion, some 70% above the $22.1 billion achieved in the same period a year ago. The analysts’ consensus for the second quarter is $45.4 billion.

Source: Company accounts, Marketscreener, management guidance for Q1 2025E, analysts’ consensus estimates. Financial year to January.

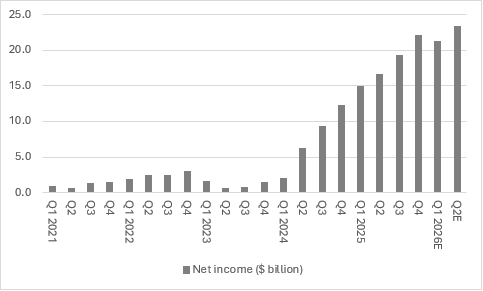

This year’s guidance for gross margin, the percent of money a company keeps from its sales, is a range of 70.6% to 71.0%. That is down from 78% a year ago and implies that the cost of sales will more than double year-on-year (hence the accusations that Mr Huang may be sandbagging the numbers).

Add in operating expenses of $5.2 billion, other financial income of $400 million and tax rate of around 17% and you get to the headline earnings per share, or EPS, figure of $0.88 per share for the first quarter. That compares to $0.61 a year ago and implies a net profit of around $21.4 billion. This would be below the outcome in the fourth quarter, which some, again, may see as conservative. These numbers exclude the projected $5.5 billion in tariff-and-trade related write-downs.

Source: Company accounts, Marketscreener, management guidance for Q1 2025E, analysts’ consensus estimates. Financial year to January.

How will NVIDIA approach tariffs and demand concerns?

More strategically, analysts will doubtless look for comments from Mr Huang on tariffs, America’s restrictions on Chinese buying of leading-edge silicon chips and the ramp-up of the Blackwell data centre chipset, where there have been reports of teething troubles.

There are two other numbers worth watching, though, especially in light of Super Micro’s profit warning. Remember that analysts used to say that Super Micro was a good proxy for demand for NVIDIA and AI-related chipsets, a comment we have heard less frequently of late, especially following the resignation of the company’s auditor, delays in the releases of quarterly regulatory filings and write-downs against the value of inventory on its balance sheet – presumably older-generation chipsets.

If a company’s big customers have too much inventory, then the danger is, at some stage, demand from that customer starts to slow, a trend which can show up in the supplier’s balance sheet, via both inventories and trade receivables.

NVIDIA had to work through an inventory bulge in 2022 that did take its toll on profit momentum, but it has done a good job since. Inventory may be rising but given the strong sales growth that is hardly a surprise and inventory days are back to pretty normal levels, by historic standards, at around 87 days.

However, some will note the way trade receivables are rising – this related to revenues possibly booked by NVIDIA but where payment has not yet been received. NVIDIA’s own website offers detail on the customer funding it provides.

Investors with long memories will remember how Cisco and some internet equipment giants provided so-called vendor financing in the late 1990s and how that helped to boost demand near-term but exacerbate the slowdown that followed as an investment boom turned to bust.

That said, NVIDIA’s sales growth is currently so rapid that days receivable are not substantially above historic norms, though they are higher, at 198 days against a five-year average of 157. There could be trouble ahead if customers start to slow their purchases for any unexpected reason, unlikely as the share price seems to think that may be.

Written by:

Russ Mould

Investment Director

Russ Mould is AJ Bell's Investment Director. He has a Master's degree in Modern History from the University of Oxford and more than 30 years' experience of the capital markets.

Ways to help you invest your money

Put your money to work with our range of investment accounts. Choose from ISAs, pensions, and more.

Let us give you a hand choosing investments. From managed funds to favourite picks, we’re here to help.

Our investment experts share their knowledge on how to keep your money working hard.