Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

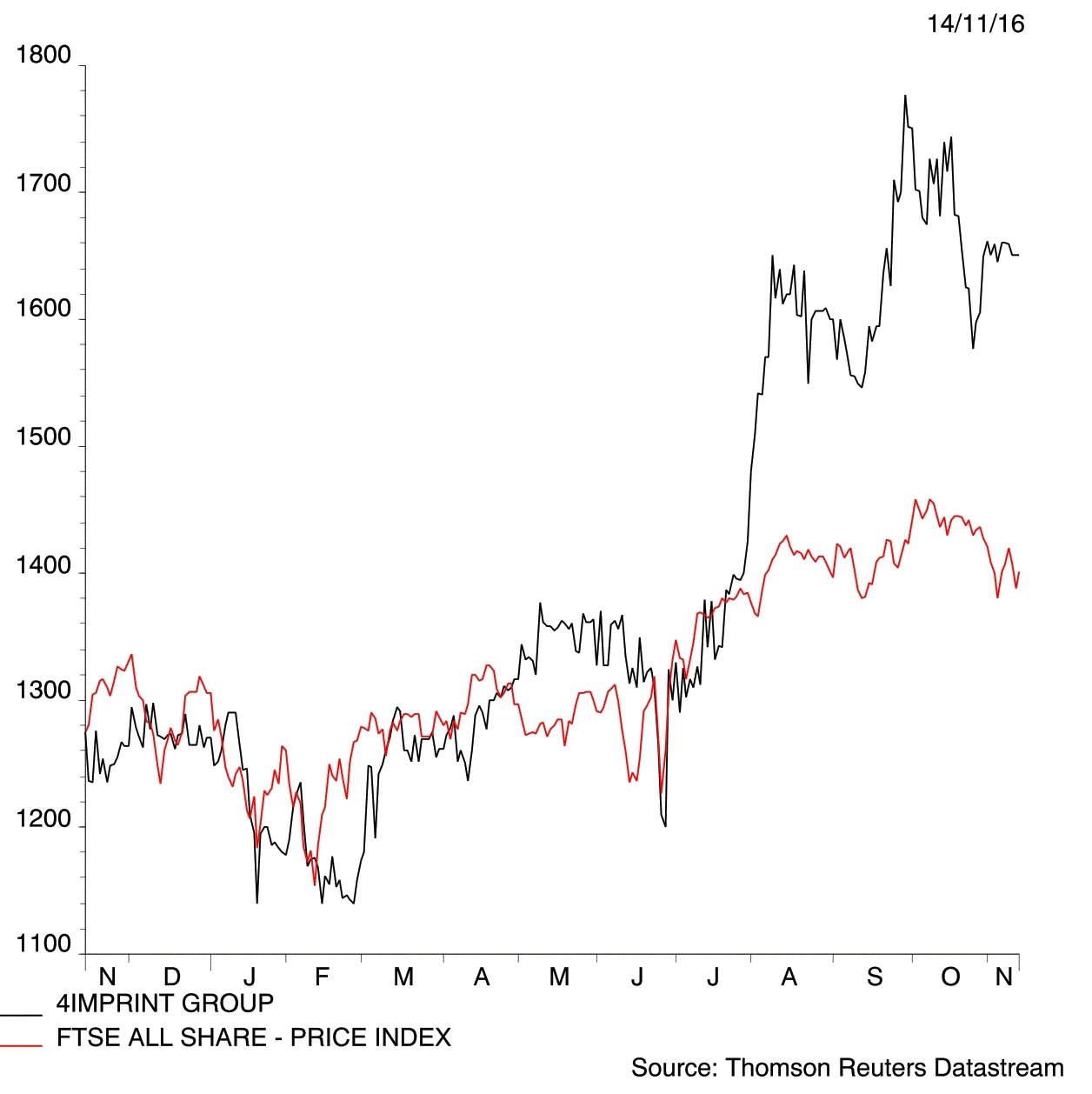

magazinePromoting 4imprint as a US play

Signs that a Donald Trump administration could stoke US economic growth is good for promotional products group 4imprint (FOUR). Buy at £16.63.

Despite being a market leader it has a modest share (around 2%) of a $24 billion addressable market in the US which accounts for 95%+ of its revenue. It has an excellent track record of under promising and over delivering.

The company is inherently cash generative with limited requirements for working capital or capital expenditure.

Now that action has been taken to address the company’s pension liabilities (76% of which are now insured), the company should be able to deliver more generous dividends to shareholders. It currently offers a prospective 2.9% yield.

The main risk for investors to weigh is a US downturn. In the 2007/8 financial crisis the shares collapsed despite a relatively robust financial performance. (TS)

Not cheap on a forward price to earnings ratio of 18.5 but a high-quality way of gaining US exposure.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.