Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineFreeAgent could be the next big disruptive firm

Now is the perfect time to buy accounting software supplier FreeAgent (FREE:AIM) as we believe a rotation is underway from short-term traders to more committed longer-term shareholders.

Many investors buy companies as soon as they join the stock market in the hope of making a quick 10%+ return. A lot of floats are priced below intrinsic value, so there is an opportunity to profit once they join the market as the price moves towards fair value (or beyond).

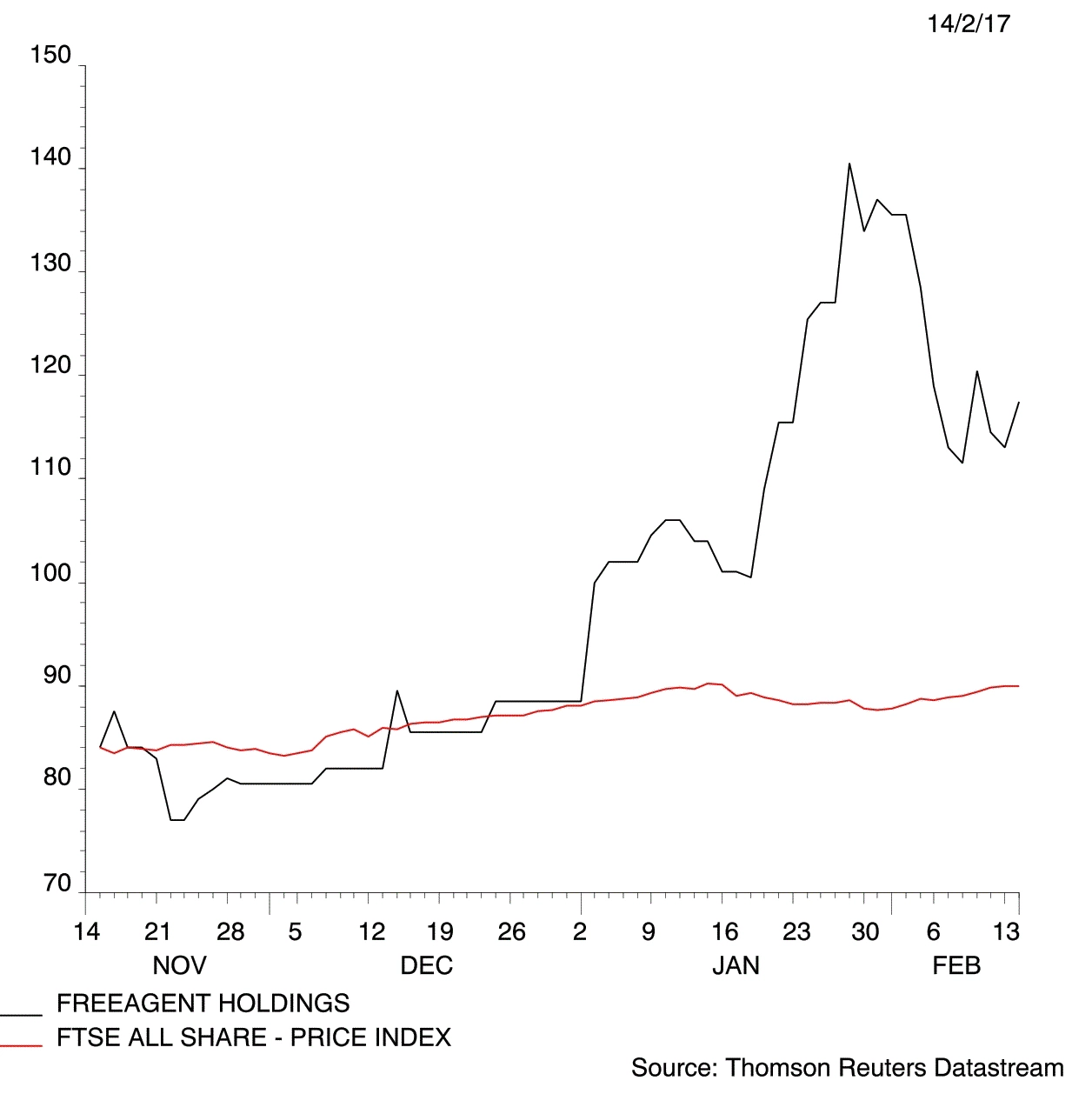

The rally and subsequent pullback in FreeAgent’s share price since its IPO (initial public offering) in November 2016 is a textbook performance. We believe the next phase for the share price is more a sustained, albeit slower upwards rally.

WHY WE LIKE THE STORY

FreeAgent has the potential to significantly disrupt the small business accounting market.

Most of the big accounting software firms largely serve businesses with at least 20 employees. FreeAgent is focused on sole traders or firms with only a handful of staff.

An estimated 90% of small businesses still use basic spreadsheets to add up their sales. The taxman wants all businesses to comply with digital accounting by 2020. That presents a large opportunity for FreeAgent to sell its accounting tool kit.

The £47m cap’s system provides ‘real-time’ tax liability tracking, invoicing and automated chasing, all seamlessly linked to a business’ bank account. Its platform is easy to use but advanced enough to charge premium fees.

In addition to direct sales, the company has successfully partnered with accountants who act as resellers. This helped customer numbers more than double to 27,137 in the six months to 30 September 2016 year on year, compared to 15% growth to 16,724 customers in the direct channel.

Average revenue per user was £17.63 on average in the period for direct sales and £10.86 from the reseller channel.

Royal Bank of Scotland (RBS) has signed up to offer FreeAgent’s software to its business bank account clients for free, paying the software firm an undisclosed licence fee.

Investors shouldn’t get carried away with this recent deal. Barclays (BARC) signed a similar partnership seven years ago which helped FreeAgent when still in its infancy. However Barclays’ importance as a source of revenue stream has ‘diminished’ in recent years, according to FreeAgent’s AIM admission document.

THE PATH TO PROFIT

FreeAgent’s average customer lifetime runs at 66 months (direct) to 96 (channel) versus customer acquisition costs (CSC) of 14 to 17 months.

Its software-as-a-service model means revenues are virtually 100% profit beyond the CSC, or between £800 and £950 per account over the contract lifetime.

Analysts forecast maiden profit in the financial year to March 2019.

FREEAGENT: (FREE:AIM) 116p

Stop loss: 80p

Market value: £47m

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.