Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineDividend relief lifts Vodafone

First-half year results from Vodafone (VOD), which helped the share price to strong gains on 13 November, tell us one thing loud and clear. This is a story where little else matters outside the dividend.

A typical sea of adjustments and footnotes, new chief executive Nick Read’s ambition is to clean up and simplify the company and how it presents its performance but Vodafone is evidently still a work in progress.

It may be one of the world’s largest mobile network companies but to be a shareholder through 2018 has been a thoroughly miserable experience. In January the share price changed hands at 238p, so at the price they traded at before the interims – 144.36p – it had lost 40% of its value in 2018.

By contrast, the FTSE 100 was down just 7% over the same period making Vodafone’s shabby performance abundantly clear.

Even at the current 155p, it’s still an ugly year-to-date performance and arguably even more staggering given that this is a FTSE 100 mega-cap valued at more than £41bn even at today’s depressed levels.

MODEST ENCOURAGEMENT

Vodafone was able to hand investors some cheer by nudging up full year guidance, even if that relies on a new swathe of cost cuts and efficiencies rather than any real improvement to how the business is trading.

Yet the only thing that really matters to investors in Vodafone is that it can keep spewing out hefty dividends. Fears of a cut to that payout have weighed heavily on the minds of investors with many presuming, so far incorrectly, that with a new man at the top a re-basing of expectations was coming.

That it hasn’t so far is a sop for the optimists. But given the current debt pile of €31bn and costly new 5G spectrum licences to be funded, we wonder for how long.

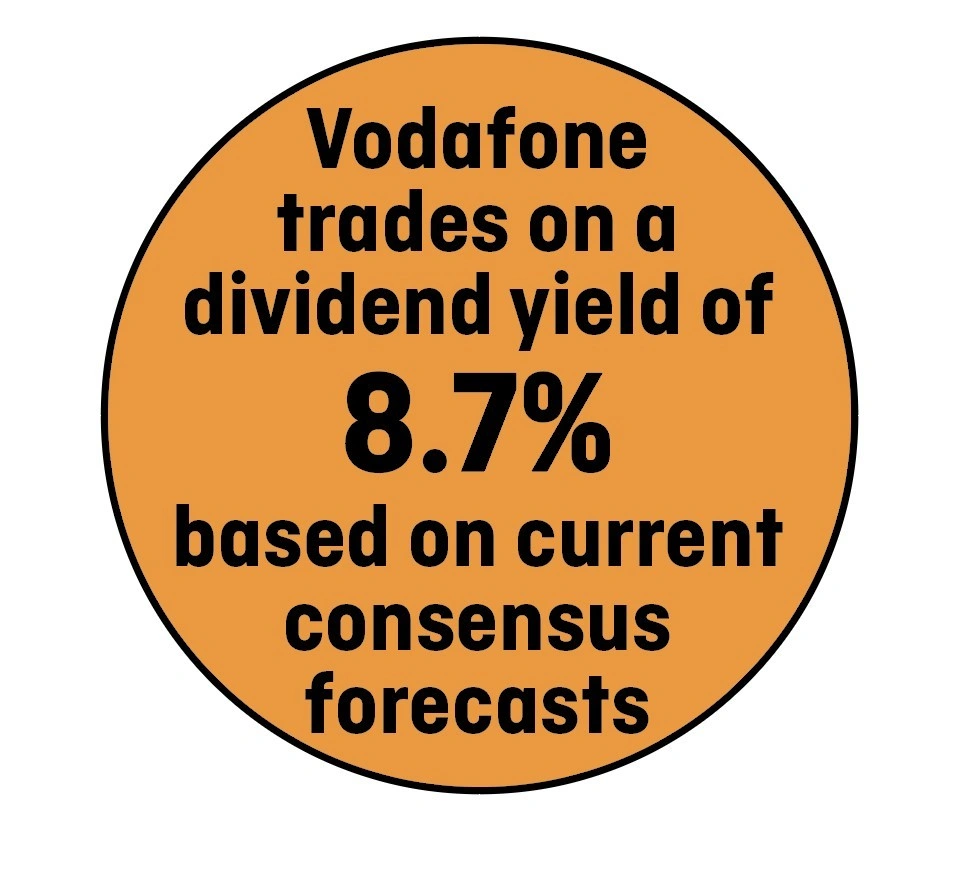

A forward yield of nearly 9% suggests the market remains sceptical on the sustainability of the dividend. (SF)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.