Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

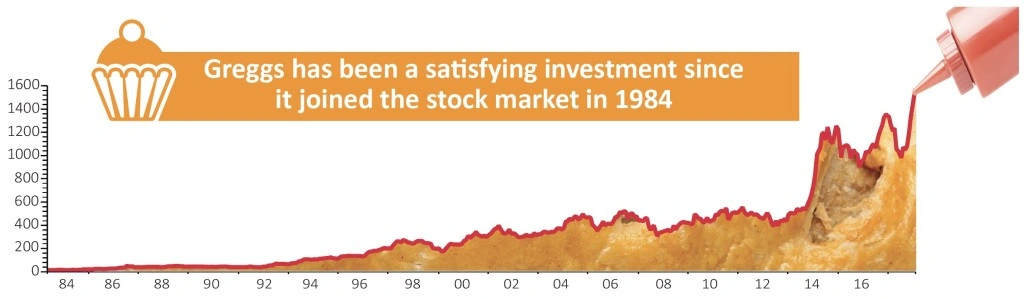

magazineGreggs is no longer good value as shares hit record high

Shares in food retailer Greggs (GRG) have hit an all-time high of £16.06, helped by a bullish trading update in January and investors keen to own a business on a roll.

Management flagged ‘good sales momentum and operational execution’ at the start of 2019. Greggs offers appeal on both the growth and income front and we expect trading has remained strong. The launch of the vegan-friendly sausage roll may have even provided a modest publicity boost for the broader business.

Sadly we believe all the good news is now in the price and the shares no longer offer compelling value. Several analysts from investment banks Berenberg and UBS also share our view.

The shares currently trade on 22 times forecast earnings for 2019 which looks too rich for a traditional bricks and mortar retailer.

Greggs will have to produce a few positive surprises in its full year results on 7 March if it is to sustain the upward share price momentum.

Berenberg argues the current strong trading is fairly reflected in the valuation, ‘especially given that free cash flow is likely to remain relatively limited this year’. Besides growing its store estate, Greggs is undergoing a significant supply chain investment programme.

Risk-averse investors should also bear in mind that same-store sales comparatives will become tougher in the second half of 2019. Last year saw the first quarter impacted by poor weather before a reacceleration in like-for-like growth in the second half.

And while Greggs is successfully shifting its exposure away from shopping locations towards work and travel, it still has material exposure to the embattled high street and faces intense competition in a crowded UK food-on-the-go market.

We rate Greggs as a fine business and one which still has considerable growth potential. For example, it is interesting to note that coffee sales are doing very well with Greggs ‘leading competitors on value-for-money perception’, says UBS.

Unfortunately we don’t think the shares are value-for-money at the current price, so anyone seeking to invest should wait until the valuation drops back before having a bite.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.