Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy central bank caution should worry investors

Just two months after it halted its quantitative easing (QE) bond-buying programme and made vague promises of interest rate increases for the second half of 2019 the European Central Bank is already downgrading its GDP forecasts for the Eurozone and delving once more into its bag of monetary policy tricks.

Interest rate increases are on hold until 2020 and the outgoing President Mario Draghi looks set to sanction another Targeted Long-Term Refinancing Operation (TLTRO) – in plain English, a third dollop of cheap cash directed at the banks to prompt them to lend and in turn offer cut-price credit to try and get the Eurozone economy back on track.

Rather than whoop for joy at the prospect of more central bank largesse, equity markets actually sagged, although bond prices rallied and yields fell as markets absorbed the possible implications of downgraded GDP growth forecasts and interest rates remaining lower for longer.

This (very rapid) policy U-turn by Draghi coincides with a similar switch by the US Federal Reserve and further studious inactivity from our own Bank of England. And coming so soon after central bankers had begun to tighten policy, albeit gently, it does raise two questions:

What are the ECB and US Federal Reserve so worried about, that they feel they cannot continue to try and normalise monetary policy? The Fed in particular is actually doing rather well on its twin mandates of inflation and employment and February’s 3.4% wage growth figure, the highest since April 2009, would normally have been enough to prompt interest rate increases.

And if the Fed and ECB stop tightening policy, is this a signal for stock markets and other risk assets to head off the races again?

That is what has happened so far this year as we have seen a huge ‘risk on’ rally with equities beating bonds hands down, cyclical sectors leading the way and high-yield or ‘junk’ bonds doing best in a fixed-income context.

But can such a surge continue if the underlying fundamentals of economics and corporate earnings are as weak as the need to stoptightening policy suggests?

FIRST CUT IS THE DEEPEST

Perhaps the ECB’s policy shift got such a cool reception last week because history actually shows that buying stocks on the first rate cut is not always a good idea. This sobering thought is worth bearing in mind, given that markets are now pricing in a 23% chance of an interest rate cut from the US Federal Reserve by December 2019, rather than the pair or trio of hikes that the central bank had been aiming for as recently as Christmas.

The ECB’s relatively limited history means we have a short data set when it comes to interest cycles and their impact on stock markets. But we have plenty of data in the UK and US.

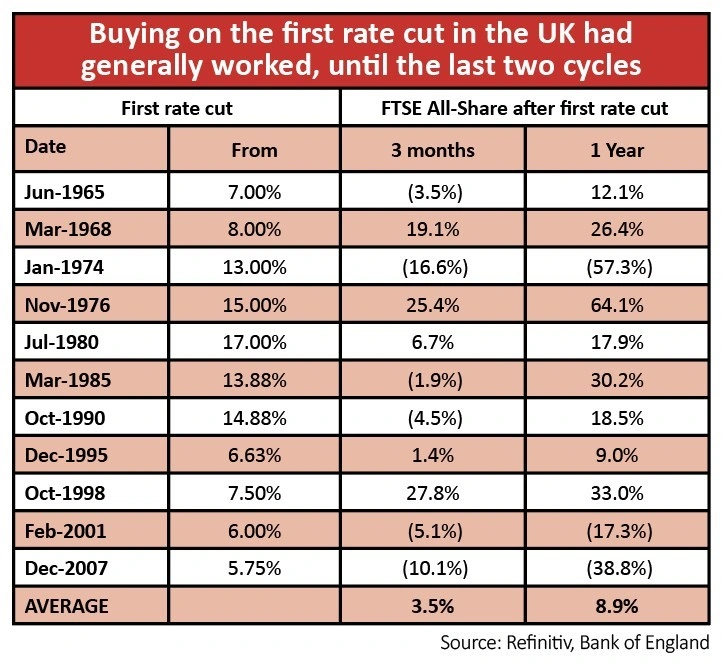

To start with the UK, the good news is that over the 11 rate-cut cycles since the inception of the FTSE All-Share in the early 1960s, the index has gained after the first decrease in borrowing costs on a three, six, 12 and 24-month view.

Yet the hit rate over the first three months is patchy (five gains, six losses) and the last two rate-cutting cycles started disastrously for buyers, with losses over a two-year period as recessions bit hard, earnings disappointed and equity valuations proved unsustainable.

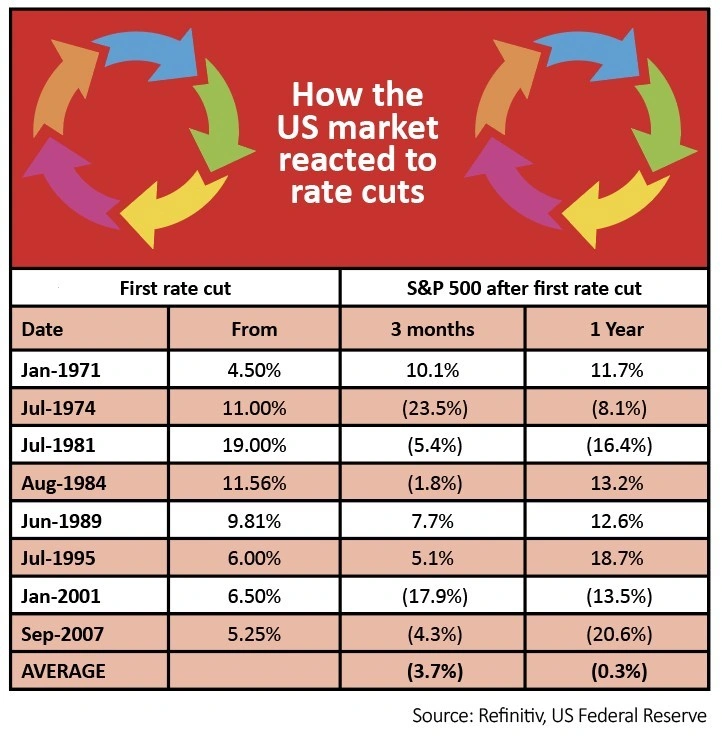

As for the US, the data since 1970 makes for grimmer reading. Buyers of US stocks after the first rate cut from the Fed have lost money on average over the past eight rate-cutting cycles on a three, six and 12-month view, with the last two being particularly painful, when ‘fighting the Fed’ was actually the right thing to do.

As for the US, the data since 1970 makes for grimmer reading. Buyers of US stocks after the first rate cut from the Fed have lost money on average over the past eight rate-cutting cycles on a three, six and 12-month view, with the last two being particularly painful, when ‘fighting the Fed’ was actually the right thing to do.

EMERGENCY MEASURE?

EMERGENCY MEASURE?

We may be jumping the gun here. The Fed is still shrinking its balance sheet, after all.

But Fed officials are already talking about zero interest rate policies and markets do seem to be asking themselves, in the case of Europe, why the third instalment of the ECB’s TLTRO should create sustainable growth when the prior two rounds did not?

And why, in the case of the US and UK, are the alleged temporary measures of a decade ago – namely QE and record-low interest rates – still required? After all, the architect of the policy in America, then Fed chair Ben S. Bernanke told Congress in 2009: ‘Clearly this is a temporary measure which is intended to provide support for the economy in this extraordinary period of crisis and when the economy is back on the road to recovery, we will no longer need to have these measures.’

Perhaps markets are now taking him at his word and thinking that the economy is still not in the best of health after all, despite 10 years of extraordinarily loose policy. And if that did not work, what remedies will central banks try next?

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit