Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

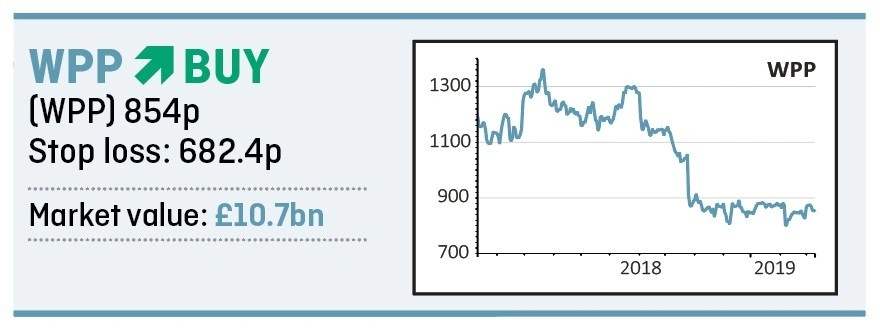

magazineNow is the time to buy WPP again

Having previously been negative on the investment case for advertising giant WPP (WPP) we now feel the story has reached a turning point and it is time to buy again.

We could be wrong and this is certainly not a stock to buy if you are risk-averse. However, the company is in the early stages of a turnaround plan under chief executive Mark Read. Any signs of progress could see the shares re-rate from the current low rating of 8.5 times forecast earnings. WPP’s 10-year average forward PE is 12-times.

The pledge to maintain dividends at a base line of 60p means investors should be paid for their patience as they wait for WPP shares to recover – that level of payout implies a 7% yield.

Read was appointed in September 2018 as a permanent successor to founder Martin Sorrell, following the latter’s acrimonious departure six months earlier.

We think if there were any hidden nasties in the business then he would have found them by now. The threat of a dividend cut also looks somewhat reduced and the company has issued some fairly conservative guidance – most notably with a third quarter update in October.

Targets for Read’s turnaround of the group include £275m

of annualised cost savings, a margin of 15% and industry growth in line with peers by the end of 2021.

As Liberum analyst Ian Whittaker observes: ‘WPP itself said it had set targets it knew it could meet and that will raise the hopes more can be done.’

WPP has lots of moving parts, having made a series of bite-sized acquisitions in the last decade. The plan is to now simplify the business and integrate the large number of agencies operating under the WPP umbrella.

The group will have four new reporting segments. The first is Communications which is currently 75% of the business and encompasses the traditional work of an advertising agency.

The other areas are Experience, Commerce and Technology – these are priorities for expansion as reflected in management comments that they ‘already’ account for a quarter of revenue.

The sale of a large stake in its market research business Kantar, expected to fetch as much as £3bn, is another strategic

priority for the group and should help reduce borrowings and could also provide scope for a one-off capital return to shareholders.

The main risk investors have to weigh is the company’s exposure to an uncertain global economic backdrop, but we think the combination of a discounted valuation, lowly expectations

and a programme of self-help is a compelling one.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Could Unilever turn the tables on Kraft Heinz?

- Doubts raised on OneSavings Bank and Charter Court merger

- Superdry, Kier, Domino’s and other news

- What Norway’s oil investment U-turn means for UK investors

- Raft of negative economic data fuels global growth concerns

- Airline sector gets tough on shareholders to keep flying post-Brexit