Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineStock markets tumble as the trade war reheats

The nascent recovery in global stocks in 2019 has suffered a significant setback. The culprit is renewed escalation in trade tensions between China and the US – an issue the markets were previously hoping would soon be resolved.

Those hopes have been dashed by an increasingly belligerent tone from the Trump administration, with an increase in tariffs on Chinese goods met by retaliation from Beijing.

Hints from Trump on 13 May of a deal in ‘three or four weeks’ helped stem some of the market panic. Yet earlier the same day the S&P 500 index of US companies endured its worst session since 3 January with more than 90% of its constituents in negative territory.

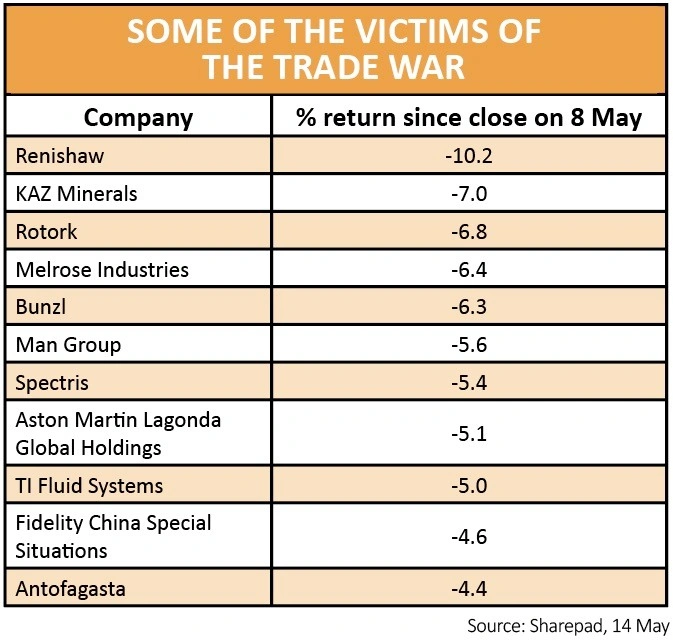

Since the issue exploded into life on 8 May, several stocks in the FTSE 350 have also taken a hit. Unsurprisingly the list is dominated by industrial stocks which would be disproportionately affected by a reduction in global trade.

Mining stocks also feature, given China’s status as a major consumer of commodities, with obvious implications for demand if the country experiences a slowdown.

China-specific investment trust Fidelity China Special Situations (FCSS) has also come under pressure.

These are the areas of the market to watch as the tit-for-tat exchanges between Beijing and Washington continue.

To an extent the FTSE 100 has been insulated from some of the pain by weakness in sterling as the wait for clarity on the UK’s exit from the European Union goes on.

Weaker sterling increases the relative value of the overseas earnings which dominate the index.

Something to monitor in the UK, beyond the long-running Brexit saga, is the jobs market and how that may result in higher interest rates.

The latest figures (14 May) showed a lower-than-expected unemployment rate and wage growth which continued to outpace inflation, even if it slipped back a little.

Thomas Pugh, UK economist at consultant Capital Economics, says: ‘The implication of solid wage growth combined with low productivity growth is that firms’ costs are rising. So far it appears that firms are absorbing higher labour costs by squeezing their margins, but this cannot go on indefinitely.

‘Eventually firms will have to pass on rising costs to consumers in the form of higher prices,’ he adds. ‘This will push up inflation and force the Bank of England to raise rates to 1.5% by the end of 2021, compared to market expectations of just 1%.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.