Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

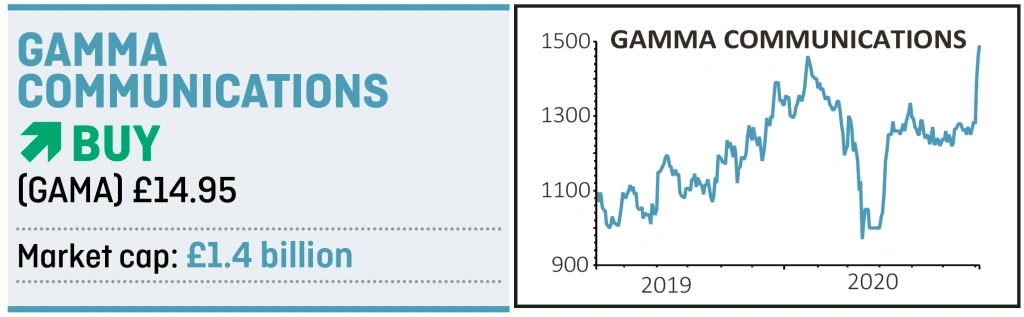

magazineGamma Communications is a superstar stock

With a growing track record for under-promising and over-delivering, Gamma Communications (GAMA:AIM) is a fairly unique play on integrated IT and communications using cloud technology.

Already a strong growth trend, the Covid-19 pandemic has hastened most organisations in their shift to embrace cloud flexibility and cost efficiency and we believe Gamma will increasingly emerge from under the investment radar.

Valued at £1.4 billion, it would go straight into the FTSE 250 index if it chose to depart AIM, and it may do so in time.

Out-competing both large and small rivals for years, Gamma is a technology-based supplier of communications solutions, or unified communications-as-a-service (UCaaS) as it is known in the industry.

The traditional telephony-based office is being transformed by new technology and mobile communications, and now businesses are embracing working from home more than ever.

Gamma has been taking advantage through a suite of in-house-designed products. Integrating services like Microsoft Teams has seen demand boom.

In 2019 the profitable, cash-generative and dividend-paying company reported a 15% rise in revenue; 10% was organic, a growth rate rare in the telecoms industry. About three quarters of the £329 million overall revenue came via its army of more than 1,000 channel partners. The rest comes from direct sales.

With a strong track record for developing communications solutions we would expect the company to continue expanding its suite, creating an increasingly compelling value and service-based proposition.

Traditionally UK-only, Gamma has expanded into Europe over the past 18 months through sensibly priced acquisitions, accessing markets in Spain, Holland and now Germany thanks to the purchase of an 80% stake in HFO earlier this month. Cloud computing penetration is much lower in Europe than the UK, and several years behind in technology adoption.

Analysts estimate that just 5% to 6% of organisations have shifted to the cloud so there is a huge opportunity for Gamma to cross-sell its best-in-class converged communications services to the enlarged customer base. That should see gross profit margins continue to escalate as they did last year, up five percentage points to 51%.

Covid-19 may have slowed the pace of installations, but this would be merely a temporary hiatus. More than 90% of revenue is recurring and billed monthly.

Compound annual revenue growth has run at about 20% a year since Gamma joined AIM in 2014, while its share price has soared by 700%.

The stock is not cheap, trading on around 29 times consensus 2021 earnings of 52p per share, but this is justified given the scope for future growth.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.