Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

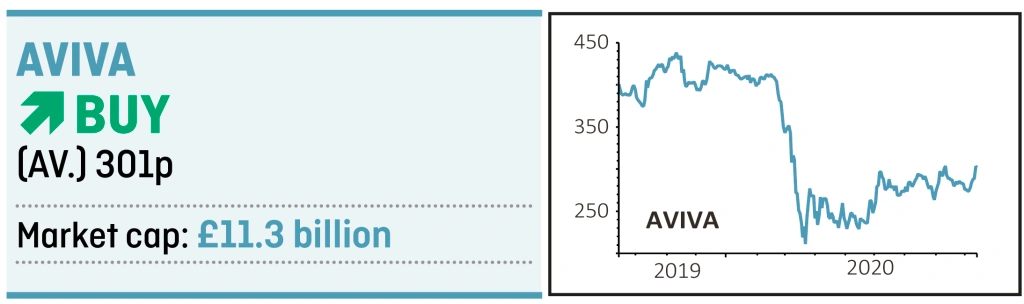

magazineAviva could deliver outsized gains under new leadership

Insurance giant Aviva (AV.) started 2020 on a high after reporting record earnings for the prior year and a promise from chief executive Maurice Tulloch to bear down on controllable costs.

He said: ‘There is much more to do simplifying our business, reducing costs and navigating competitive markets to make Aviva a stronger, simpler, better company.’

Just a few months later he was replaced by former AXA UK chief executive and ABI chair Amanda Blanc, who vowed not only to simplify the business but to go further, reviewing ‘all strategic opportunities, at pace, in order to unlock value for shareholders’.

That was code for disposals, which Tulloch – an Aviva ‘lifer’ – had shied away from, much to the disappointment of investors.

True to her word, last week Blanc set the ball rolling by agreeing to sell a majority stake in Aviva’s prized Singapore business to a local firm for £1.2 billion in cash and a further £400m in dividends and marketable debt securities.

‘In selling Singapore for £1.6bn, Aviva will realise value equivalent to 15% of the market capitalisation for a loss of just 5% of earnings and negligible cash generation,’ comments Jefferies analyst Philip Kett. ‘These proceeds will be retained to support central liquidity (ultimately used to reduce leverage when debt rolls off).’

The deal marked ‘a significant first step in our new strategy to bring greater focus to Aviva’s portfolio’ as well as bringing ‘excellent upfront value for shareholders’, according to Blanc.

It represents the first step in shifting Aviva’s focus to its core UK, Ireland and Canada operations. The non-core entities are interests in mainland Europe and parts of Asia.

Despite lower sales and a rise in Covid-related general insurance claims, the core Aviva business has weathered the pandemic, reporting a robust set of half-year results, and the group’s solid return on equity has allowed it to reinstate dividend payments.

Despite this, the shares trade on a 12-month prospective multiple of just 6.5 times earnings – one of the lowest ratings in the FTSE 100 index – and a prospective yield of 8.6%, towards the top end of the range for a FTSE stock.

In addition, we would argue that the funds business, Aviva Investors, deserves greater recognition due to the high returns it gets for customers and the value it adds to the business.

Last year 84% of the firm’s funds beat their benchmark, generating third-party net inflows of £2.3 billion compared with net outflows the year before.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.