Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

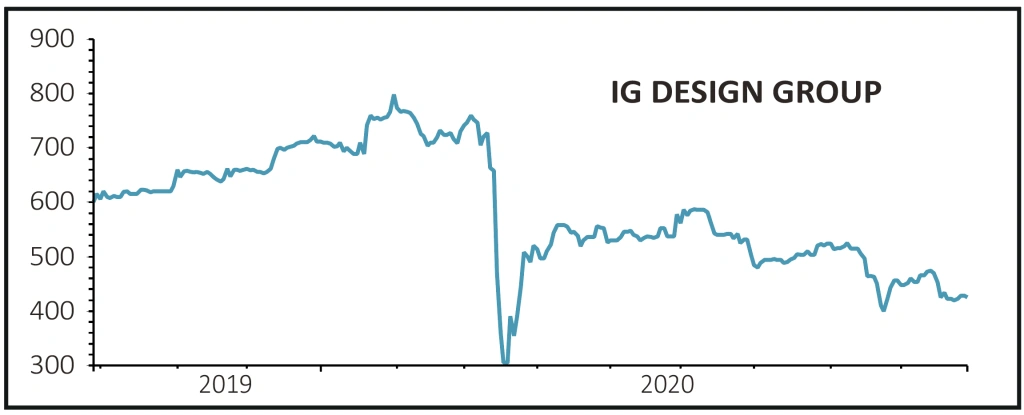

magazineIG Design is down but not out

IG Design (IGR:AIM) 420.2p

Loss to date: -39.7%

Original entry point: Buy at 697p, 19 December 2019

Coronavirus has not been kind to our bullish stance on greetings card firm IG Design (IGR:AIM).

While initial concerns centred on its supply chain – with some of the group’s manufacturing base in China – the pandemic’s spread led to increasing concern about demand for the group’s products which span everything from gift packaging, greetings cards, stationery and design-led giftware.

A trading update on 21 September at least confirmed the company would hit expectations for the 12 months to 31 March 2021.

Revenue is expected to be up year-on-year – albeit thanks to its £89.7 million acquisition of CSS, a deal which doubled the size of its footprint in the US.

The company also said it had started to deliver on its $500 million pipeline of orders and is building on this pipeline with new orders. Investors can expect more details in a planned update for mid-October.

SHARES SAYS: We hope the October trading statement can help improve sentiment towards the stock. Stick with the shares for now.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.