Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineIndustry price hikes mean now is the time to buy Smurfit Kappa

FTSE 100 packaging group Smurfit Kappa (SKG) has numerous factors working in its favour which could lead to brokers upgrading their earnings forecasts in the coming weeks.

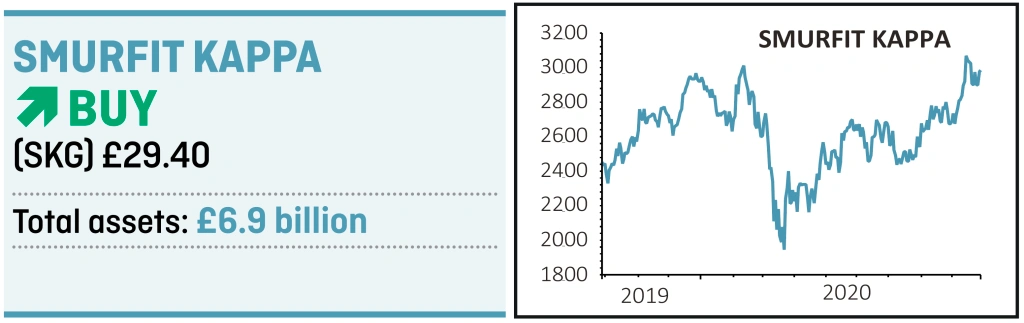

The shares have yet to reflect the improving fundamentals and trade on an undemanding 13 times next year’s earnings while also offering an attractive 3.5% dividend yield, covered three times by earnings. Now is the time to buy.

THREE LEGS TO THE STORY

The picture started to look more positive in August, when two of Smurfit’s competitors, SCA and UPM, announced capacity cuts equivalent to around 9% of the European installed base.

Meanwhile Lee & Man, China’s second largest containerboard producer, announced it had abandoned plans to add a new 300,000-tonne recycled containerboard machine at one of its plants in China, switching the planned capacity to tissue instead.

This month several leading US packaging companies including International Paper and Packaging Corporation of America announced the first increase in containerboard prices since 2018 with other players expected to follow suit.

The increase is in response to very strong box shipment data which grew 4% over the last three months leading to declining inventories. Along with other European players Smurfit announced plans to increase recycled containerboard prices by €50 per tonne from 1 October.

According to stockbroker Davy, Europe is a net importer of approximately 1 million tonnes of kraftliner, most of which comes from the US, so rising import prices will justify lifting prices in the continent.

BENEFITS TO SMURFIT

If implemented, the better pricing environment could amplify the earnings benefit due to Smurfit’s past self-help measures which have reduced costs and increased efficiencies.

A good indicator of the improving state of the business was the 29 July decision to pay a dividend of 80 cents a share after deferring the decision in April.

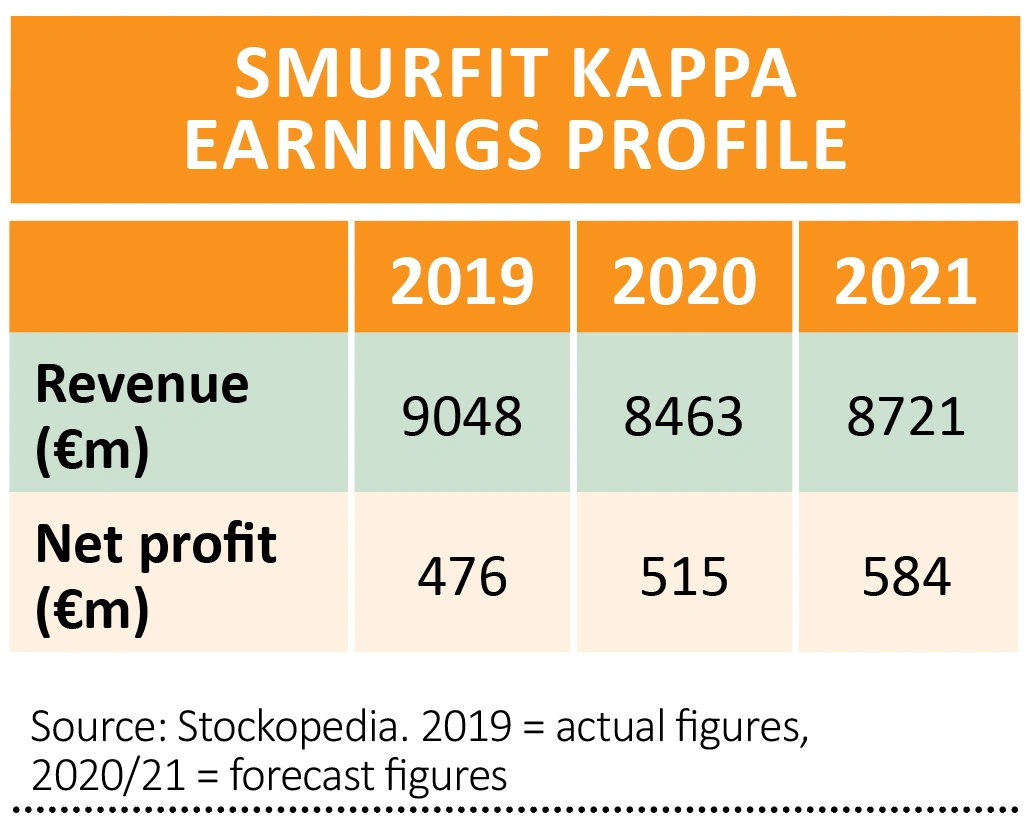

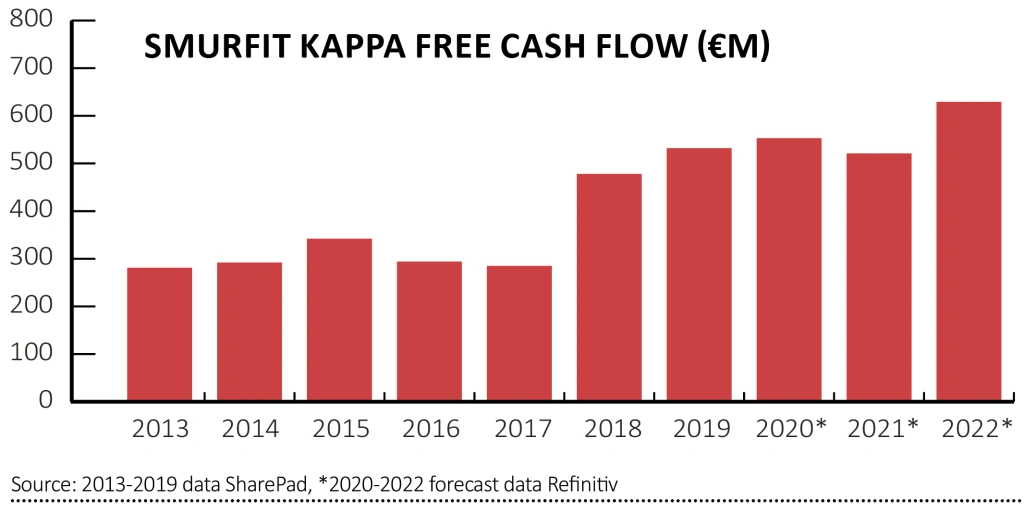

Despite first-half EBITDA (earnings before interest, tax, depreciation and amortisation) dipping 13% from last year to €735 million, the company generated free cash flow of €238 million in the first-half, which was up almost 50% on the same period last year.

One surprising characteristic given the capital-intensive nature of the packaging industry is that Smurfit has grown free cash flow at a compound annual growth rate of almost 10% since 2007.

STRUCTURAL GROWTH

Smurfit has capacity to manufacture 7.6 million tonnes of papers annually for the packaging industry. It designs, makes and supplies paper-based packaging to package, promote and protect its customers’ products.

It is a globally diversified business servicing over 64,000 customers from 350 production sites across 35 countries. The company has a clear strategy to selectively expand its market positions in Europe and the Americas while maintaining a disciplined approach to capital allocation with a strong focus on cash generation.

The firm’s scale, expertise and global footprint give it an edge to meet increasing customer demands, such as responding to Ebay UK’s request for 5 million boxes to be delivered in 10 days.

Corrugated paper shipments have grown consistently since 1990 averaging 5.5% a year and are expected to reach $317 billion in value by 2023 according the company.

Future growth will be driven by e-commerce, discount retailers and corrugated as a sustainable, renewable, bio-degradable solution.

ESG CREDENTIALS

Investors concerned about the carbon footprint of packaging companies will be pleased to discover that Smurfit has been publishing sustainability reports for over 13 years and holds a leading position in third party sustainability rankings.

Smurfit helps customers to create efficiencies and reduce their carbon footprint by using sustainable paper resources and eliminating single use plastics.

A good example is Bike Fun International which was able reduce the number of its different packaging types by 60%, allowing it to cut waste and double packing speeds to meet increasing demand.

Smurfit notes that 55% of consumers purchase a product because it has reusable or biodegradable packaging and management puts sustainability at the core of the business.

The company replaces the natural resources it uses by recycling over 6 million tonnes of fibre annually and managing 68,000 hectares of forests. The group is listed on the FTSE4Good index as well as the Stoxx Global ESG Leaders register.

Take advantage of the cheap valuation and get ahead of analyst upgrades.

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.