Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

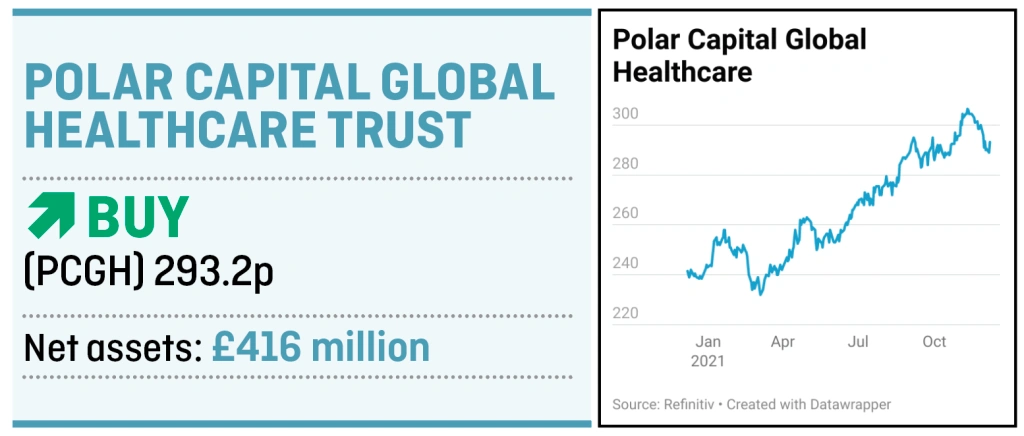

magazineBuy cut-price Polar Capital Global Healthcare for defensive growth

While it may be slightly out of favour with investors at present, healthcare is a good addition to any portfolio. It tends to be relatively insensitive to what’s happening in the wider economy and demographic drivers, particularly in the West, are likely to underpin demand in the years to come as we emerge from the Covid-19 pandemic.

Investment Trust Polar Capital Global Healthcare (PCGH) trades at a 7.2% discount to NAV whereas International Biotechnology (IBT) and Worldwide Healthcare (WWH) trade at modest premiums.

This likely reflects the historic underperformance of the Polar Capital vehicle, which struggles against its peers on a 10-year view; however, the last 12 months have seen a marked uptick in performance.

This has been helped by large cap stocks, where the portfolio is focused, outperforming small caps and biotech plays with stretched valuations – a reversal of the trend heading into the pandemic.

The trust’s innovations portfolio, which can account for as much as a fifth of its total holdings, has also been restructured so it is no longer as exposed to high-risk UK micro caps which had proved to be a drag on performance.

Managers James Douglas and Gareth Powell are focused on several themes which they believe can underpin durable medium-term growth. These include companies offering products and services which allow for the more efficient delivery of care without compromising on its quality, outsourcing of non-core activities and preventative medicine through vaccines and diagnostics.

The most notable feature of the portfolio is the modest representation for pharmaceutical stocks – a 20.8% allocation as of 29 October 2021, compared with 36.7% for the MSCI All Country World Healthcare benchmark. The trust instead has a higher allocation than the benchmark to healthcare equipment, facilities, supplies and distributor businesses.

The trust was launched in 2010 with the intention of being wound up in January 2018. This date was extended to March 2025 at which time the directors are required to propose liquidation or lay out new plans.

The mandate was changed in June 2017 to focus more on capital growth, where previously there was an emphasis on income; the yield is now a mere 0.7%. Ongoing charges come in at 1.09% which is comparable with other trusts in the healthcare space.

‘After a challenging period following the 2017 restructuring, the trust has become

overlooked – with the market failing to notice the strong turnaround in performance,’ said analysts at Stifel in September. ‘The team appears to have rectified performance, and it is now the cheapest healthcare trust by some margin.’

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Danni Hewson

Editor's View

Feature

Great Ideas

Investment Trusts

News

- BT could go down a different path for its sports arm

- China crackdown on US listings to benefit Hong Kong Stock Exchange

- Stock markets stage full recovery after Omicron fears

- Thungela plots bumper dividend despite coal price retreat

- Stocks relevant to efforts to licence vaping for medical use

- New listing rules aim to bring more innovative companies to London