Archived article

Please note that tax, investment, pension and ISA rules can change and the information and any views contained in this article may now be inaccurate.

magazine

magazineWhy GlaxoSmithKline’s HIV division could nearly double in value by 2020

Pharma giant GlaxoSmithKline’s (GSK) drug Juluca should help to drive value in its HIV-focused ViiV business after being approved by the US Food & Drug Administration (FDA).

HIV is a virus that damages cells in the immune system, making it more difficult for people to fight off infections and disease.

Market is ‘undervaluing’ hiv business

Juluca is the first treatment for HIV-1 that contains just two drugs, dolutegravir and rilpivirine, instead of three to help reduce toxicity in patients.

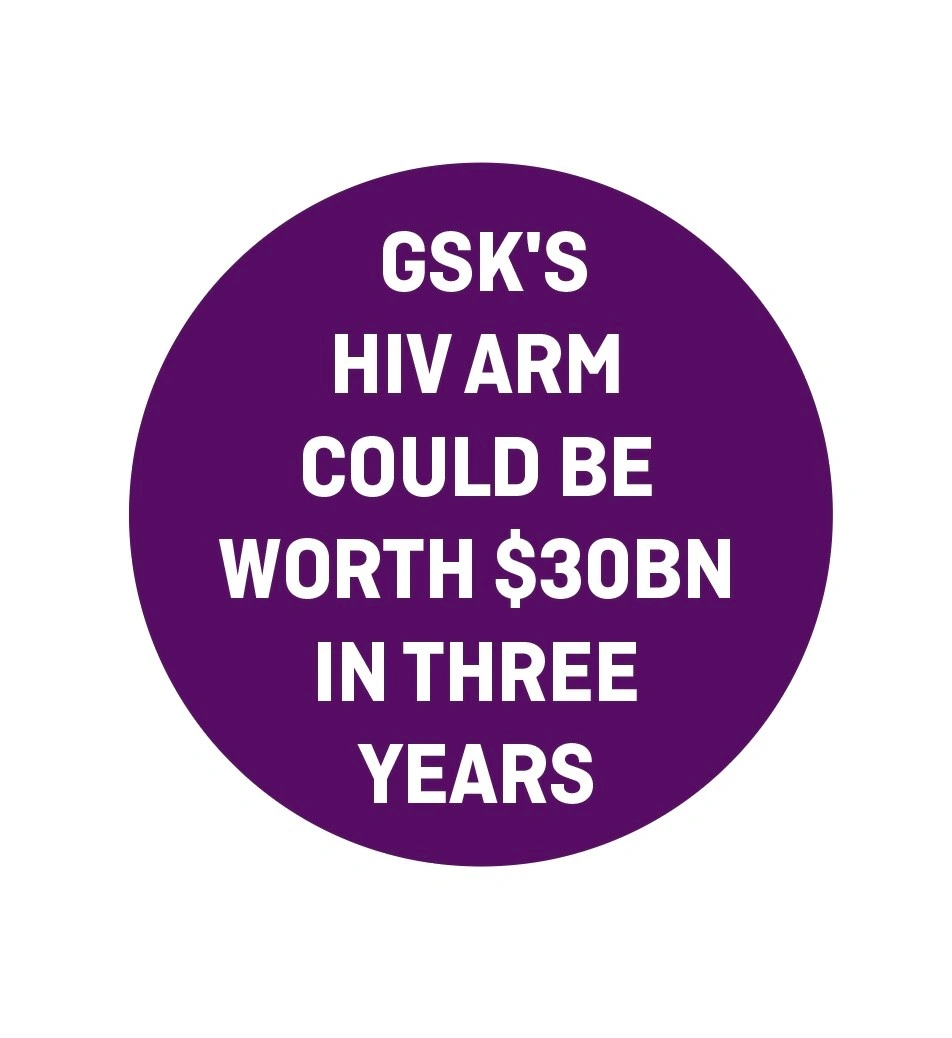

HSBC analyst Steve McGarry values the ViiV division at $16bn today and forecasts sales of approximately $8.1bn in 2023. He believes the market is undervaluing the business. Based on the analyst’s 2020 forecasts, the ViiV business could be worth closer to $30bn. Glaxo’s total market cap in dollars is currently around $86bn.

McGarry says operating margins will ‘comfortably exceed 50%’ once several large clinical studies are completed.

This is despite potential competition from US-listed Gilead’s HIV drug bictegravir, commercialisation of which could be delayed if GlaxoSmithKline takes legal action. McGarry believes this is a possibility due to the ‘striking similarity of both drugs and how they act’.

Dividend concerns on potential M&A

GlaxoSmithKline’s share price has fallen by 16.9% to £12.98 so far this year.

One of the biggest concerns weighing on the stock is a potential dividend cut following speculation the drugs giant might buy US-listed Pfizer’s consumer division.

Beaufort Securities analyst Ben Maitland says 2018 could be an expensive year for the firm if it goes ahead with the Pfizer deal and also buys Novartis’s minority stake in Glaxo’s consumer joint venture.

He estimates the total cost could be $24bn, which might result in a dividend cut, as the ratio between net debt and earnings would be a demanding 3.5 times if these transactions were funded entirely by debt.

Another threat is a potential generic version of GlaxoSmithKline’s multi-billion asthma treatment Advair Diskus, which could drag on Glaxo’s earnings growth in the longer term if rivals gain regulatory approval. Its competitors in this area Hikma (HIK) and US-listed Mylan have failed so far.

These headwinds look like they might already be reflected in the price as GlaxoSmithKline offers a generous dividend yield of 6.1% and trades on an undemanding forecast 11.9 times earnings per share in the year to 31 December 2018. (LMJ)

Important information:

These articles are provided by Shares magazine which is published by AJ Bell Media, a part of AJ Bell. Shares is not written by AJ Bell.

Shares is provided for your general information and use and is not a personal recommendation to invest. It is not intended to be relied upon by you in making or not making any investment decisions. The investments referred to in these articles will not be suitable for all investors. If in doubt please seek appropriate independent financial advice.

Investors acting on the information in these articles do so at their own risk and AJ Bell Media and its staff do not accept liability for losses suffered by investors as a result of their investment decisions.

Issue contents

Big News

- Centrica’s yield could be a phantom menace

- UK banks pass latest stress tests

- New European-focused fund offers tastier way to play e-commerce logistics boom

- Tri-Pillar promises ‘completely different’ infrastructure proposition

- UK engineers in demand with customers and investors

- ConvaTec and Merlin to be ejected from FTSE 100